Most financial advisors stay far away from estate planning. They assume it’s purely the attorney’s domain. They worry about stepping into legal practice. They’re uncomfortable with the conversations. So they do nothing, and their clients remain vulnerable.

This hesitation is a missed opportunity. You don’t need to become an estate planning expert to add enormous value. You need to understand your quarterback role: identifying when planning is needed, assembling the right professionals, ensuring they work together, and most critically, verifying that the plan actually gets implemented.

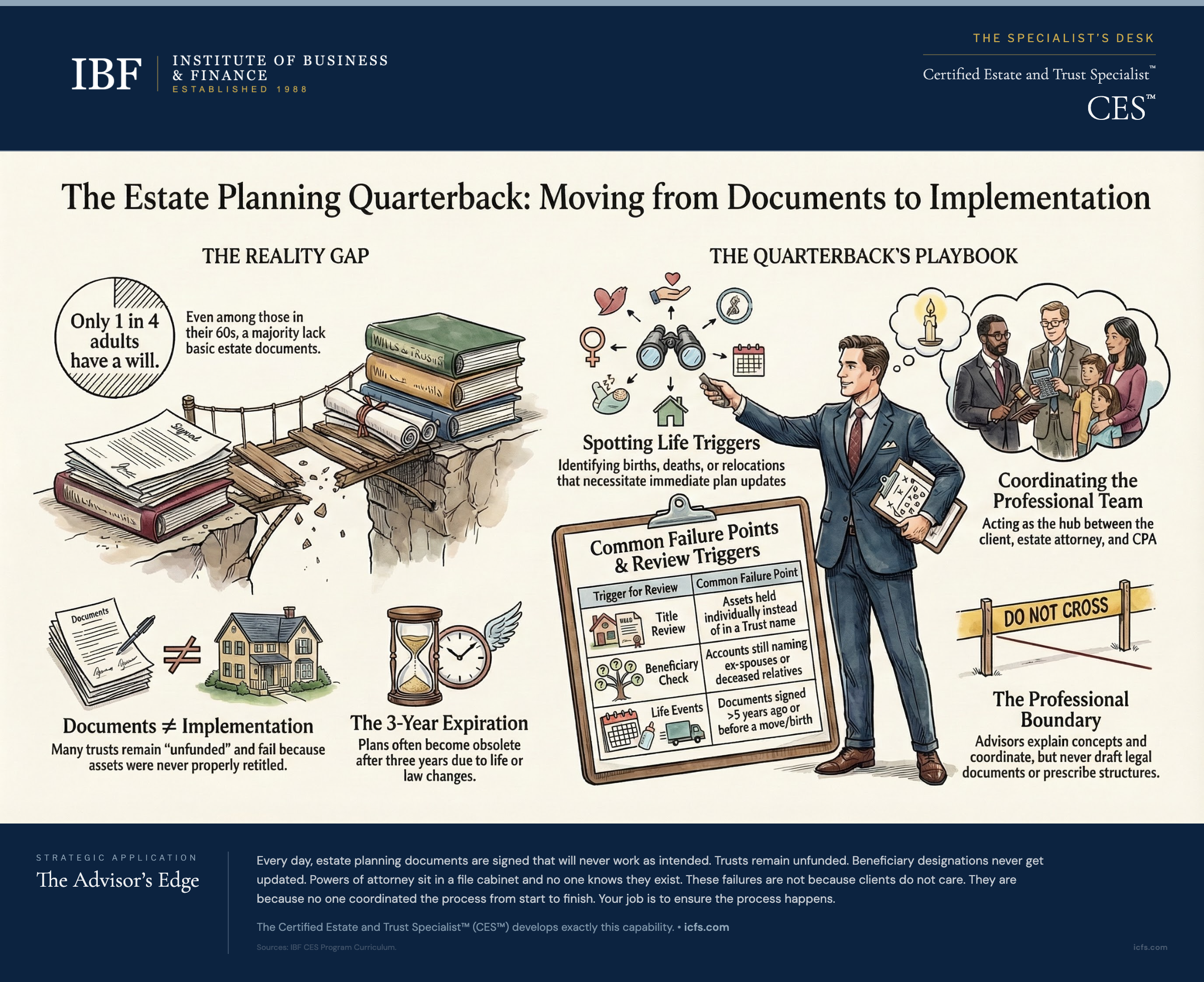

The gap between documents drafted and documents implemented is enormous. Clients sign revocable living trusts that never get funded. They update beneficiary designations on some accounts but miss others. They have wills that no one can find when they’re needed. An attorney’s job ends when the client signs. Your job is just beginning.

The Completion Gap

Look at the statistics on estate planning completion and ask yourself a tough question: How many of your clients fall into these gaps?

Only about 1 in 4 American adults have a will. Among adults in their 50s and early 60s, a majority still lack one (Caring.com 2024; Trust & Will 2025). This isn’t because people don’t care about what happens to their assets. It’s because estate planning feels abstract, uncomfortable, and low-priority until something forces it to the front of the mind. Most clients won’t initiate these conversations. They’re waiting for you to bring it up.

But there’s a second gap that matters more. Among clients who do have estate planning documents, many have false security. Your client has a will from 2009. Their trust was signed five years ago but never funded. Their beneficiary designations haven’t been reviewed in a decade, so they’re probably wrong. Their power of attorney names someone who moved to another state and probably won’t serve. The documents exist. The plan doesn’t work.

This second gap is where you operate. It’s not legal work. It’s project management. It’s asking the questions attorneys don’t see, the ones that come from knowing your client’s full financial picture. It’s ensuring that the beautiful documents signed in the attorney’s office actually move into implementation in the real world. And it’s the highest-value estate planning work you can do.

The Six Quarterback Functions

Your quarterback role has six distinct components. Understanding each one gives you a framework for when and how to step in.

Identifying Need

You spot triggers that clients don’t. A new grandchild. A significant inheritance on the horizon. A relocation to a different state. A business sale. A health event. A marriage or divorce. A client who just accumulated $500,000 in life insurance proceeds and hasn’t thought about what happens if that client dies with the proceeds still floating around.

These triggers tell you that estate planning is needed or that existing plans need updating. The attorney won’t see them. The attorney only sees what clients tell them at a single point in time. You see the full arc of a client’s life because you’re working with them over years.

Start building a trigger list. Keep it simple. When you spot one of these signals in a client meeting, add it to a calendar reminder to revisit estate planning. Don’t assume your client already has a plan. Ask directly: “Have you reviewed your estate documents in the last three years?” or “If something happened to you tomorrow, do you know if your will still reflects your wishes?” The answers will surprise you.

Initiating Conversation

Most clients won’t ask about estate planning. They’re uncomfortable with mortality. They don’t know what they should have. They assume if it’s important, they’ll remember to do it (they won’t). So you need to bring it up, and you need to do it directly.

Here’s how this conversation often works in practice. You’re meeting with a couple in their early 60s. They have significant assets, two adult children, and grandchildren. You review their investment strategy. Then, before they leave, you say something like: “Before you go, I want to ask about your estate plan. When did you last review your will?” They’ll either say “we have one from years ago” or “we’ve been meaning to do that.” Either way, you’ve opened the door.

Your follow-up is crucial. Don’t hand them a checklist and wish them luck. Instead, ask specific questions that surface gaps. “When was it drafted?” “Have you had any major life changes since then?” “Do you know if your will still names who you want to manage your estate?” “Have you reviewed your beneficiary designations on your retirement accounts?” “If you became unable to manage your finances tomorrow, who would handle your accounts?”

These questions serve two purposes. First, they often reveal that existing documents are outdated or incomplete. Second, they demonstrate that you take this seriously, which gives clients permission to admit they need help.

Assembling the Team

You’re not drafting documents. But you need to know which professionals draft them well. Maintain a roster of three to five estate planning attorneys you trust. Not all attorneys are created equal. You want someone who focuses on estates, not a general practice lawyer who occasionally drafts wills. For complex situations, you want an attorney with deeper credentials like an LL.M. in taxation or board certification in estate planning.

You should also have relationships with CPAs who understand estate tax implications, life insurance specialists if your client base includes business owners, and maybe a trust company for clients who need institutional trustees.

When a client needs to connect with an attorney, you don’t send them into the world alone. You either introduce them directly or at least recommend someone specific. You tell them: “I work regularly with Jane Smith at Smith Estate Planning. She specializes in situations like yours. I’ll give her a call and have her expect your call.” This makes the attorney transition smoother and shows your client that you’re actively involved.

Coordinating Across Professionals

This is where your quarterback value becomes visible. Consider a real example: Your client is planning to set up a revocable living trust. The attorney is excellent at estate documents. But the attorney doesn’t know that your client’s brother (who was going to be successor trustee) struggles with substance abuse and financial management. The attorney also doesn’t know that the client’s tax situation involves significant pass-through business income and complex retirement account withdrawals. The attorney doesn’t know that the client’s intended executor is now retired and living five hours away and probably shouldn’t manage a complex estate administration.

Without your input, the attorney drafts a technically sound document that may not fit reality. You step in. You have conversations with the client about these issues. You make sure the attorney knows about them before finalizing documents. You might facilitate a three-way conversation between the attorney and your client about trustee options if the original plan doesn’t work. You ensure the CPA understands what the new trust structure means for income tax planning.

This coordination rarely happens unless someone forces it. Attorneys don’t reach out to advisors. Advisors who don’t take initiative leave their clients with documents that look good on paper but don’t serve reality.

Tracking Implementation

This is where the quarterback role delivers the most tangible value, and where most plans break down.

Start with the asset audit. Every asset transfers at death through exactly one of three mechanisms: will and probate (for assets titled solely in the individual’s name), beneficiary designation (for retirement accounts, life insurance, and annuities), or operation of law (for jointly titled property and trust assets). Most clients assume their will controls everything. It does not. For many clients, the will controls a fraction of their wealth.

Consider Eleanor, age 75, a widow with three adult children and $1.5 million in assets. She wants everything divided equally. Her asset audit reveals: Her $600,000 home is correctly titled in her revocable trust and will pass equally through the trust terms. Her $400,000 brokerage account is titled jointly with her eldest daughter, added “for convenience” years ago, passing entirely to the eldest daughter by operation of law. Her $350,000 IRA correctly names all three children as equal beneficiaries. Her $50,000 bank account has a payable-on-death designation to her youngest daughter “to pay final expenses.” Her $100,000 life insurance policy still names her deceased husband as beneficiary.

The actual distribution under current titling: the eldest daughter receives $717,000, the middle child receives $317,000, and the youngest receives $367,000. The life insurance proceeds revert to Eleanor’s estate (assuming no contingent beneficiary is named), where they are subject to probate and creditor claims rather than passing directly to her children. Eleanor’s equal-distribution intention produces dramatically unequal results. A five-column exercise (asset, title, transfer mechanism, beneficiary or co-owner, value) catches this before it becomes permanent.

Next, audit beneficiary designations. These override everything, including the will, including the trust. When they are correct, they provide fast, private, probate-free transfers. When they are wrong, they produce outcomes that cannot be undone after death. The most common errors: designations that still name an ex-spouse from a marriage that ended decades ago. Designations that name a deceased person, forcing the account through a claims process. Designations that name only one child when the client has three. Designations that name “my estate” as beneficiary of a retirement account, pulling it into probate and subjecting it to the 5-year distribution rule when the owner dies before the Required Beginning Date. (Since the SECURE Act of 2020, most individual beneficiaries face a separate 10-year distribution rule, making proper beneficiary designation even more critical.) Your audit should cover every account with a beneficiary designation: IRAs, 401(k)s, life insurance, annuities, payable-on-death bank accounts, and transfer-on-death brokerage accounts. For each one, verify that the primary beneficiary is current, that a contingent beneficiary is named, and that the designation coordinates with the rest of the estate plan.

Finally, verify trust funding. A revocable living trust avoids probate, provides privacy, and enables controlled distributions. But only for assets actually titled in the trust’s name. An unfunded trust is an empty container. Your checklist after trust creation: verify that real estate deeds have been recorded, brokerage accounts retitled, bank accounts retitled or given POD designations to the trust, and that the client understands that any new accounts opened in the future must also be titled in the trust’s name. Then verify again at the next review meeting. In six months, ask: “Can you pull up one of your investment account statements and let me see how it’s titled?” If it still shows individual name only, you know there’s work to do.

Maintaining the Plan

Estate planning isn’t an event. It’s a process. Plans age poorly. A will drafted 15 years ago might name an executor who has since died. It might reference assets the client no longer owns. It might fail to address grandchildren born after the documents were signed. It might use tax planning strategies that no longer apply.

Clients need periodic reviews. A common standard is every three to five years, or after any major life change: marriage, divorce, birth, death, significant asset change, relocation, or business change.

You can be the person who triggers these reviews. Calendar it. Every three years on each client’s review date, you ask about estate planning. You don’t require them to redo everything. Often a small amendment is enough. But you ensure they’re not coasting on a 20-year-old plan.

Where the Advisor’s Role Ends

Here’s what you don’t do. You don’t draft wills, trusts, or powers of attorney. That’s unauthorized practice of law. You don’t recommend specific trust structures or estate planning tax techniques. You don’t advise clients about whether they should use a revocable trust versus an irrevocable life insurance trust. You don’t tell them they should do a Roth conversion as part of their estate plan or that they should consider a charitable remainder trust.

The line is this: You explain how concepts work. You don’t prescribe which structure to choose.

If a client asks whether they should set up a living trust, your answer is NOT “Yes, everyone should have a living trust.” Your answer is: “A revocable living trust helps with probate avoidance and incapacity management. Whether it makes sense for your situation depends on several factors an attorney needs to evaluate. Let me get you in front of an estate planning specialist who can look at your whole picture and give you advice on whether a trust is right for you.”

You can explain beneficiary designation rules. You cannot tell a client which beneficiary option to choose for their IRA.

You can point out that a client’s documents haven’t been reviewed in a decade and likely need updating. You cannot tell them what the updated documents should include.

You can identify that a situation might require a special needs trust. You cannot draft one or recommend specific terms.

Crossing this line creates legal liability. It also weakens your position as quarterback. Your value is knowing when to involve specialists, not trying to be a specialist in multiple domains at once.

Client Conversation

Let me walk through three real client conversations where the quarterback role plays out differently.

The Client Who Thinks a Will Is Enough

Your client, Linda, is 58 and has significant assets spread across multiple accounts. She mentions casually that she had a will drafted years ago and feels good about her planning. You ask when it was drafted. “Oh, maybe 2015?” she says. Then you ask: “What about incapacity planning? Do you have financial and health care powers of attorney?” She looks confused. “What’s that for?” This is your moment.

You explain: “A will only controls what happens after you die. But what if you can’t make decisions before that? If you had a stroke tomorrow, who would pay your bills? Who would manage your investments? Who would talk to your doctors? Without a power of attorney, your family would have to go to court to get a guardianship. That’s expensive and slow and public.”

Linda nods. She hadn’t thought about this. You say: “You should review with an attorney not just your will, but your whole estate plan including incapacity documents. I can refer you to someone good. But before you go, let me ask a few questions so I can brief the attorney on your situation.” You pull out a simple sheet and ask about her family structure, her major assets, whether anyone depends on her financially, what her biggest concerns are. Then you send her to the attorney with some context.

The Client Whose Trust Isn’t Funded

Your client, Robert, signed a revocable living trust two years ago. He felt accomplished. He was done. You’re meeting for his annual review and you ask: “How are your investment accounts titled now?” He says they’re still in his name. “Have you had a chance to retitle them into the trust?” He hasn’t. He had meant to, but it felt complicated and he forgot.

This is the implementation gap. You say: “That trust isn’t doing what you intended until we get your accounts titled into it. Once they’re titled in the trust name, they avoid probate. If you stay in your account name, they’ll go through probate even though you have the trust.” Robert looks concerned. “What do I need to do?”

You pull out a copy of his trust and review who the trustee is, confirm Robert is comfortable with that structure, then say: “Let me call your brokerage and ask what they need to change the title. I’ll walk you through it, or we can do it together.” You then follow through. You don’t send him away hoping he’ll do it. You help him across the finish line.

The Client Whose Beneficiary Designations Are Wrong

Your client, Susan, is divorced. She remarried five years ago. She’s been meaning to update her estate plan but hasn’t gotten around to it. You’re reviewing her financial accounts during a planning meeting and you ask about beneficiary designations. You pull up her retirement accounts and her life insurance.

The retirement account still names her ex-husband from her first marriage as the primary beneficiary. The life insurance names her daughter from her first marriage to receive 60% and doesn’t mention her current husband at all. Susan is horrified. “That’s not what I want at all!”

You say: “We need to fix this immediately. Your ex-husband is legally entitled to that retirement account when you die, even though that’s not your intention. Your current husband gets nothing.” You pull out the forms and Susan fills them out while you’re sitting there. You say: “I’ll call the custodians to confirm these went through. But let me also recommend you get in front of an estate planning attorney to make sure your will and other documents line up with these beneficiary designations.”

In each of these conversations, you’re not practicing law. You’re asking questions, identifying gaps, and making sure something actually happens. That’s the quarterback role.

Key Takeaways

- Identify estate planning needs proactively, not reactively. Spot triggers like life events, asset changes, and time passing. Ask directly about existing documents. Don’t assume clients have addressed it.

- Know when a client has an outdated plan. A document signed years ago without review is almost certainly incomplete or wrong. Changes in family, assets, location, and law create gaps. Review creates accountability.

- Assemble a team before you need it. Build relationships with estate planning attorneys, CPAs, and other specialists. Know who you’d refer to for different situations. Don’t send clients to practitioners you haven’t vetted.

- Coordinate across professionals. Make sure the attorney understands your client’s financial situation. Make sure the CPA understands the estate structure’s tax implications. You’re the hub connecting spokes. This coordination rarely happens without your initiative.

- Track implementation relentlessly. The gap between documents signed and documents implemented is enormous. Follow up on trust funding. Verify beneficiary designation updates. Confirm powers of attorney are signed. Don’t assume it happened just because the attorney said they would handle it.

- Know your boundaries. Explain how estate planning concepts work. Don’t recommend which specific structures, tools, or techniques apply to a specific client. Refer those decisions to qualified attorneys. Your value is in coordination and implementation, not in legal recommendations.

The Advisor’s Edge

Every day, estate planning documents are signed that will never work as intended. Trusts remain unfunded. Beneficiary designations never get updated. Powers of attorney sit in a file cabinet and no one knows they exist. Incapacity arrives and families face guardianship proceedings that are slow, public, and costly. These often cost several thousand dollars and can rise steeply in complex or contested situations. These failures aren’t because clients don’t care. They’re because no one coordinated the process from start to finish.

This is available expertise that every practicing advisor can develop. Estate planning fundamentals are teachable. The concepts of transfer, incapacity, probate, and beneficiary coordination are straightforward once explained. The documents and structures are specialized, yes, but your job isn’t to specialize in them. Your job is to ensure the process happens.

The Certified Estate and Trust Specialist™ (CES™) designation develops exactly this capability. The curriculum covers the full estate planning landscape: property ownership, transfer mechanisms, the roles of different documents, how to identify what’s missing from existing plans, how to coordinate with attorneys and CPAs, and most importantly, how to track implementation so the plan actually works.

As you deepen this expertise, you’ll find that estate planning conversations become less uncomfortable and more natural. You’ll know what to ask. You’ll know which professionals to involve. You’ll have frameworks for verifying whether existing plans are actually functional or just appear to be. Clients will stop seeing you as the investment manager and start seeing you as the coordinator who makes their entire financial picture work together. If you’re ready to develop these skills, explore the CES program and build this capability in your practice.

Sources and Notes: This article draws from the Certified Estate and Trust Specialist curriculum developed by the Institute of Business & Finance and reflects practitioner principles established across 16 chapters covering property ownership, transfer mechanisms, document coordination, and implementation tracking. This article is refreshed biennially.