Required Minimum Distributions: Calculate, Plan, and Avoid the Penalty

At age 72, your client thinks she has finally reached the promised land. No more contributions. No more early withdrawal penalties. Just decades of tax-deferred growth ahead.

Then comes the letter from her IRA custodian. By April 1 next year, she must withdraw a specific amount. It is not optional. It is not a recommendation. It is a Required Minimum Distribution. Miss it by a dollar, and the IRS imposes a 25% penalty on the shortfall.

This chapter covers what RMDs are, how to calculate them, and how to manage them strategically. The rules are complex, but the core principle is simple: Congress created tax-deferred accounts to help you save for retirement, not to create permanent tax shelters. RMDs ensure that retirement assets eventually get taxed.

When RMDs Begin

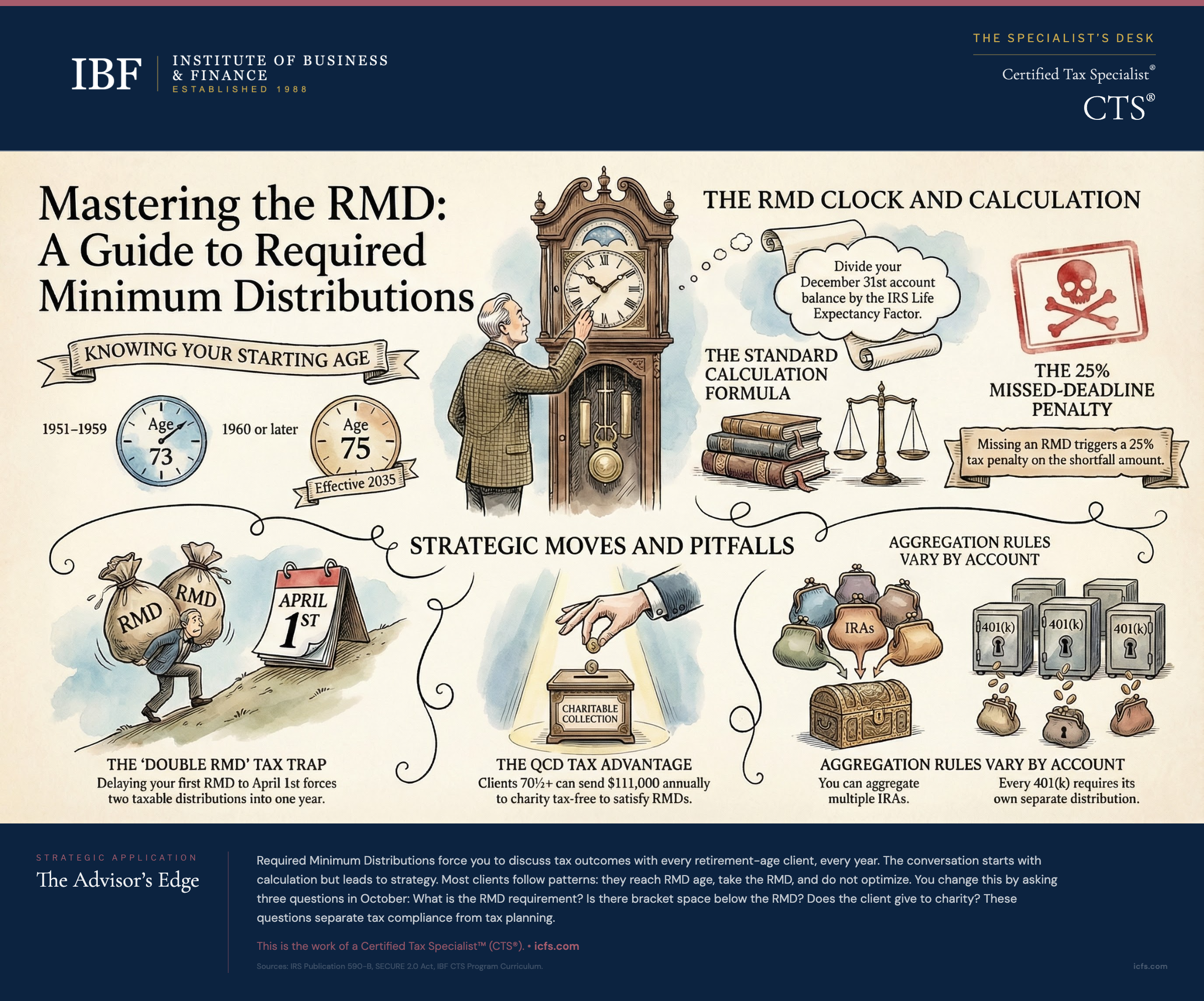

The year your client turns their applicable RMD age, they enter the Required Beginning Date phase. Under SECURE 2.0, the RMD age depends on birth year.

If your client was born before July 1, 1949, RMDs began at age 70 1/2 under pre-SECURE Act rules. For those born July 1, 1949 through December 31, 1950, RMDs began at age 72. For those born 1951 through 1959, RMDs begin at age 73. For those born 1960 or later, RMDs begin at age 75. This rule does not take effect for any client until 2035, when the first cohort of 1960-born individuals reaches age 75.

The Required Beginning Date (RBD) is the deadline for taking the first RMD: April 1 of the year following the year they reach their applicable RMD age. If a client turns 73 in 2026, their RBD is April 1, 2027. This is when the first RMD must be taken, not when it becomes mandatory to begin.

This distinction matters because delaying the first RMD creates a uniquely expensive tax problem.

The RMD Calculation

The calculation follows a simple formula: Account Balance divided by Life Expectancy Factor.

The account balance is the December 31 balance from the prior year. For 2026 RMDs, use the December 31, 2025 balance.

The life expectancy factor comes from an IRS table. Most account owners use the Uniform Lifetime Table, which assumes a beneficiary exactly 10 years younger than the account owner, regardless of who is actually named. If you turn 74 in 2026 and your IRA balance on December 31, 2025 was $850,000, the Uniform Lifetime Table factor at age 74 is 25.5. Your RMD is $850,000 divided by 25.5, or $33,333.

You can always withdraw more. The RMD is a floor, not a ceiling.

When the Joint Life Table Applies

The Uniform Lifetime Table is the default. But there is one scenario where a different calculation applies. If your sole beneficiary is your spouse and your spouse is more than 10 years younger than you, the Joint Life and Last Survivor Table produces a smaller RMD.

Consider this example. Thomas is 75 with a traditional IRA worth $1,200,000. His wife Linda is 62, making her 13 years younger. Linda is his sole beneficiary.

Using the Uniform Lifetime Table at age 75, the factor is 24.6. The RMD is $48,780.

Using the Joint Life Table for ages 75 and 62, the factor is 26.8. The RMD is $44,776.

The Joint Life Table produces a smaller RMD because it accounts for the longer joint life expectancy. Thomas keeps roughly $4,000 more in tax-deferred growth each year. This only works if the beneficiary designation remains unchanged. Changing beneficiaries to adult children or trusts immediately eliminates access to the Joint Life Table.

Which Accounts Require RMDs

RMDs apply to traditional IRAs, SEP IRAs, SIMPLE IRAs, 401(k)s, 403(b)s, and 457(b)s. RMDs do not apply to Roth IRAs during the owner’s lifetime. Effective for tax years beginning after December 31, 2023, SECURE 2.0 eliminated the RMD requirement for Roth 401(k)s. Note: participants who turned 73 in 2023 still had to take a 2023 RMD by April 1, 2024.

After an account owner dies, inherited accounts follow different rules.

The First Year RMD Decision

Your client reaches their RMD age. They face an unusual choice. They can delay their first RMD until April 1 of the year following the year they reach RMD age. This is the only time a delay is permitted. This seems attractive. One more year of tax-deferred growth.

But delaying creates a hidden cost. If you delay the first RMD, you must still take your second RMD by December 31 of that same year. This creates a “double RMD” year where two years of distributions land in a single calendar year.

Patricia turns 73 in March 2026. Her RBD is April 1, 2027. She faces two options.

Option A: Take her 2026 RMD in 2026. Then take her 2027 RMD in 2027. Two distributions across two years.

Option B: Take no RMD in 2026. Then in 2027, take the 2026 RMD by April 1 and the 2027 RMD by December 31. Two distributions in the same calendar year.

If Patricia’s IRA balance produces a $19,000 RMD each year, Option B creates $38,000 of taxable income in 2027. This might push her into a higher tax bracket, trigger additional Social Security taxation, or affect Medicare premiums. Option A spreads $19,000 across two calendar years.

For most clients, taking the first RMD in the first year produces better tax results. The delay option rarely makes sense unless a client has unusually high income in the first RMD year and expects significantly lower income the following year.

RMD Aggregation Rules

Clients with multiple retirement accounts face aggregation questions. The rules differ sharply by account type.

If you have multiple traditional IRAs, you calculate the RMD for each separately, then withdraw the total from any one or more IRAs. You have complete flexibility in how you satisfy the requirement.

Susan has three traditional IRAs with balances of $200,000, $150,000, and $100,000. Her RMDs are $7,843, $5,882, and $3,922 respectively. Total RMD is $17,647. She can withdraw the entire $17,647 from her largest IRA alone, or split it across accounts. Her choice.

But 401(k) plans do not work this way. Each 401(k) must satisfy its own RMD. You cannot take the RMD from one 401(k) to satisfy another.

Jonathan has a 401(k) from his current employer with $400,000 and a 401(k) from a former employer with $200,000. He must calculate and withdraw RMDs from each plan separately. He cannot take one large distribution from one plan to cover both.

This difference creates a strategic implication. Consolidating old 401(k)s into a single IRA simplifies RMD management because IRAs allow aggregation. But before consolidating, check the still-working exception. If you are still employed and do not own more than 5% of the company (under IRC section 416, including family attribution rules), you can delay RMDs from your current employer’s plan until retirement, even if you are past RMD age. Rolling this money to an IRA would lose this advantage.

Strategies for Taking RMDs

The RMD is a minimum requirement, not a target. Several strategies optimize how you satisfy it.

Take distributions throughout the year instead of one lump sum. Monthly or quarterly withdrawals smooth cash flow and avoid year-end scrambles.

Withdraw from the poorest performers in your portfolio. If your IRA holds multiple investments, withdraw from positions you would sell anyway. Rebalance while satisfying RMDs.

Take RMDs early in the year. Withdrawing in January gives more time for reinvestment if you do not need the income. Early withdrawal also protects against year-end complications like account errors or illness.

Or use a Qualified Charitable Distribution.

Qualified Charitable Distributions (QCDs)

If your client is age 70 1/2 or older and charitably inclined, a QCD is the most tax-efficient RMD strategy available.

A Qualified Charitable Distribution allows IRA owners age 70 1/2 or older to transfer directly from their IRA to a qualified 501(c)(3) charity. The distribution satisfies the RMD requirement but is excluded from taxable income. The annual limit, originally $100,000, is indexed for inflation. For 2026, the limit is $111,000.

Why does this matter? Consider Eleanor, age 75, who takes a $30,000 RMD and wants to donate $10,000 to charity.

Without QCD, she faces two scenarios. If she itemizes, she deducts $10,000. Her taxable income is $20,000. If she takes the standard deduction, she receives no deduction at all. Her taxable income is $30,000.

With QCD, she directs $10,000 from her IRA to the charity. This $10,000 satisfies part of her RMD but is excluded from her taxable income. Her remaining RMD is $20,000. Her taxable income is $20,000.

The QCD produces the same result as itemizing a charitable deduction, but with a critical advantage: it works even for clients who take the standard deduction. Most retirees do not itemize. For them, regular charitable donations produce zero tax benefit. QCDs always work.

QCDs also lower AGI, which reduces Social Security taxation and may lower Medicare premium surcharges (IRMAA). The indirect benefits often exceed the direct income tax savings.

Requirements for QCDs are simple. The client must be age 70 1/2 or older (not 73, the RMD age). The transfer must be direct from the IRA to a qualified charity. It cannot go to donor-advised funds, private foundations, or supporting organizations. The client cannot receive goods or services in exchange.

Spousal and Non-Spouse Beneficiary Rules

When a retirement account owner dies, the rules change for beneficiaries. For purposes of this article, we focus on the primary account owner’s RMD. But advisors should understand what happens when clients inherit accounts, as this affects planning for estate purposes.

Surviving spouses have the most flexibility. They can roll an inherited IRA into their own IRA, keeping the account as their own and subject to their own RMD schedule. They can also elect to remain as beneficiary of the inherited account. Or they can take a lump sum distribution. Most younger surviving spouses benefit from the rollover option.

For non-spouse beneficiaries, SECURE Act rules are less generous. Most non-spouse beneficiaries must withdraw the entire inherited account within 10 years. The exceptions are narrow: surviving spouses, minor children of the owner (until they reach majority), disabled or chronically ill individuals, and beneficiaries not more than 10 years younger than the owner.

If the original account owner died after their Required Beginning Date, beneficiaries must take annual distributions within the 10-year window. If the owner died before their RBD, annual distributions are not required. The beneficiary simply must empty the account by the 10-year deadline.

The RMD Penalty

Missing an RMD triggers a penalty. SECURE 2.0 reduced the penalty from 50% to 25% of the shortfall. If the shortfall is corrected within two years, the penalty drops further to 10%.

If Richard’s 2026 RMD was $25,000 and he withdrew only $15,000, his shortfall is $10,000. The penalty at 25% is $2,500. If he corrects the shortfall within the correction window, the penalty is $1,000.

To correct, Richard must withdraw the $10,000 shortfall and file Form 5329 with a reasonable cause explanation. The IRS has often waived penalties when taxpayers self-report missed RMDs and promptly correct them, but penalty waiver is not guaranteed.

Common causes of missed RMDs include forgetting the first RMD (new retirees often miss this), multiple accounts with separate RMDs (especially multiple 401(k)s), inherited IRAs with rules that confuse beneficiaries, and custodian errors.

Limitations and Complications

RMD planning breaks down when tax situations are not predictable. Large one-time income events (asset sales, business exits, Roth conversions) in the year of an RMD can create unexpected tax brackets. In these years, taking less than the RMD may seem attractive, but this is not possible. The RMD is mandatory.

Second, the still-working exception applies only to current employer plans. If you are still working but have IRAs from previous employers, RMDs apply to those IRAs regardless of your employment status.

Third, RMDs interact with other tax rules in ways that require coordination. Social Security becomes partially taxable as provisional income rises. Medicare premiums increase at high income levels. State income taxes may apply. These interactions mean RMD planning cannot be done in isolation.

Client Conversation Example

Your 73-year-old client arrives with a question. His custodian is pestering him about an RMD withdrawal. He has not thought about taking money from his IRA yet. His Social Security is modest. He does not need the money. Can he skip it?

The answer is no. RMDs are mandatory. But the conversation that follows matters.

You discover that he gives $8,000 annually to his church. He takes the standard deduction. He has not itemized in years. This is the perfect QCD situation.

You explain that a QCD allows him to direct $8,000 from his IRA directly to the church. This $8,000 satisfies part of his RMD but is excluded from his income. His total RMD might be $35,000, but $8,000 of it goes to charity. His taxable income is $27,000 instead of $35,000. His tax bill drops by roughly $1,760 (at 22% rate).

He had no idea that his charitable giving could reduce his taxes when he takes the standard deduction.

A second client is not so fortunate. She has two 401(k)s from two separate employers and an IRA rolled from an older plan. She has three separate RMD calculations. She almost missed the 401(k) RMD last year because she did not realize she had to take it from that specific plan. She cannot aggregate.

You set up a system to remind her in October of each RMD calculation and deadline. You recommend consolidating the old 401(k) into her IRA (after verifying the still-working exception does not apply). This simplifies future management.

A third client faces the classic first-year dilemma. He turns 73 in December. His RBD is April 1 of the following year. He asks whether he should take his first RMD in December of his birth year or wait until April.

You calculate both scenarios. Taking it in December spreads $28,000 across two calendar years. Delaying until April creates a $56,000 double RMD year that pushes him into a higher tax bracket and triggers additional Social Security taxation. The cost of the double RMD year is roughly $4,200 in extra taxes.

He elects to take the first RMD in the year he turns 73. The analysis makes the decision obvious.

Key Takeaways

- RMD age is 73 for those born 1951–1959, or 75 for those born 1960 or later. The Required Beginning Date is April 1 of the year following the year you reach your RMD age. Missing any RMD carries a 25% penalty on the shortfall (10% if corrected within two years).

- Calculate using the Uniform Lifetime Table in most cases. Account Balance divided by the age factor produces the RMD. The Joint Life Table applies only when the sole beneficiary is a spouse more than 10 years younger. Verify beneficiary designations annually because changing beneficiaries eliminates the Joint Life Table advantage.

- Delay the first RMD only in unusual circumstances. Delaying the first RMD until April 1 creates a double RMD year. For most clients, taking the first RMD in the first year produces better tax outcomes. Model both scenarios before deciding.

- Understand aggregation rules by account type. Traditional IRAs aggregate: calculate each separately, withdraw from any combination. 401(k)s do not aggregate: each plan requires its own distribution. This distinction affects consolidation decisions and the still-working exception.

- QCDs are the default strategy for charitably inclined clients age 70 1/2 or older. Directing up to $111,000 annually from an IRA to a qualified charity satisfies the RMD while excluding the amount from income. This works even for clients taking the standard deduction. The indirect benefits (lower Social Security taxation, lower Medicare premiums) often exceed the direct tax savings.

- Inherited account rules are restrictive for non-spouse beneficiaries. Most non-spouse beneficiaries must empty inherited accounts within 10 years. If the original owner died after their RBD, annual distributions are required within the 10-year window. Only Eligible Designated Beneficiaries can stretch over life expectancy.

- RMD planning must coordinate with other income sources. Large distributions affect Social Security taxation, Medicare premiums, and state income taxes. Run an annual review in October to identify bracket space, QCD opportunities, and Social Security optimization before year-end.

The Advisor’s Edge

Required Minimum Distributions force you to discuss tax outcomes with every retirement-age client, every year. The conversation starts with calculation but leads to strategy.

Most clients follow patterns. They reach RMD age. They take the RMD. They do not optimize. You change this by asking three questions in October:

(1) What is the RMD requirement? (Calculate it.)

(2) Is there bracket space below the RMD? (Tax efficiency question.)

(3) Does the client give to charity? (QCD question.)

These questions separate tax compliance from tax planning. The difference is measurable and repeatable.

The analytical skills here are specific. You are reading IRS tables. You are calculating life expectancy factors. You are modeling tax brackets year by year. You are coordinating multiple income sources. This is the work of a Certified Tax Specialist™ (CTS®). This is the knowledge your designation signals to clients and other professionals.

For a closer look at how Roth conversions interact with RMD planning, see Roth Conversion Decision Framework: When to Convert and How Much.

Sources and Notes: Content draws on CTS Module 1, Chapter 5 (Retirement Distribution Rules) and Module 2, Chapter 10 (RMD Planning Strategies). QCD limit for 2026 per IRS Notice 2025-67. SECURE 2.0 RMD age provisions per P.L. 117-328, Sections 107 and 302. Uniform Lifetime Table and Joint Life Table factors from IRS Publication 590-B (2025 edition). Penalty reduction from 50% to 25% per SECURE 2.0 Section 302. This article is refreshed annually or as tax law changes.