The 1035 Exchange Decision: More Than a Tax Strategy

Your 58-year-old client calls with frustration. Her variable annuity is eating her alive with fees. A colleague mentions she could move the money to a lower-cost FIA without triggering taxes. She asks: should she do it?

The answer is not obvious, and it starts with understanding what Section 1035 actually does.

Section 1035 of the Internal Revenue Code permits tax-free exchanges between certain insurance products. For annuity owners, it means you can trade an old annuity contract for a new one without recognizing the gain in the old contract. The gain that built up over years of accumulation simply carries forward to the new contract. No immediate tax, no capital gains, no ordinary income due on the exchange itself.

This tax treatment is valuable. It removes a major barrier to repositioning. But it also creates a false comfort zone. The absence of tax does not mean the absence of cost.

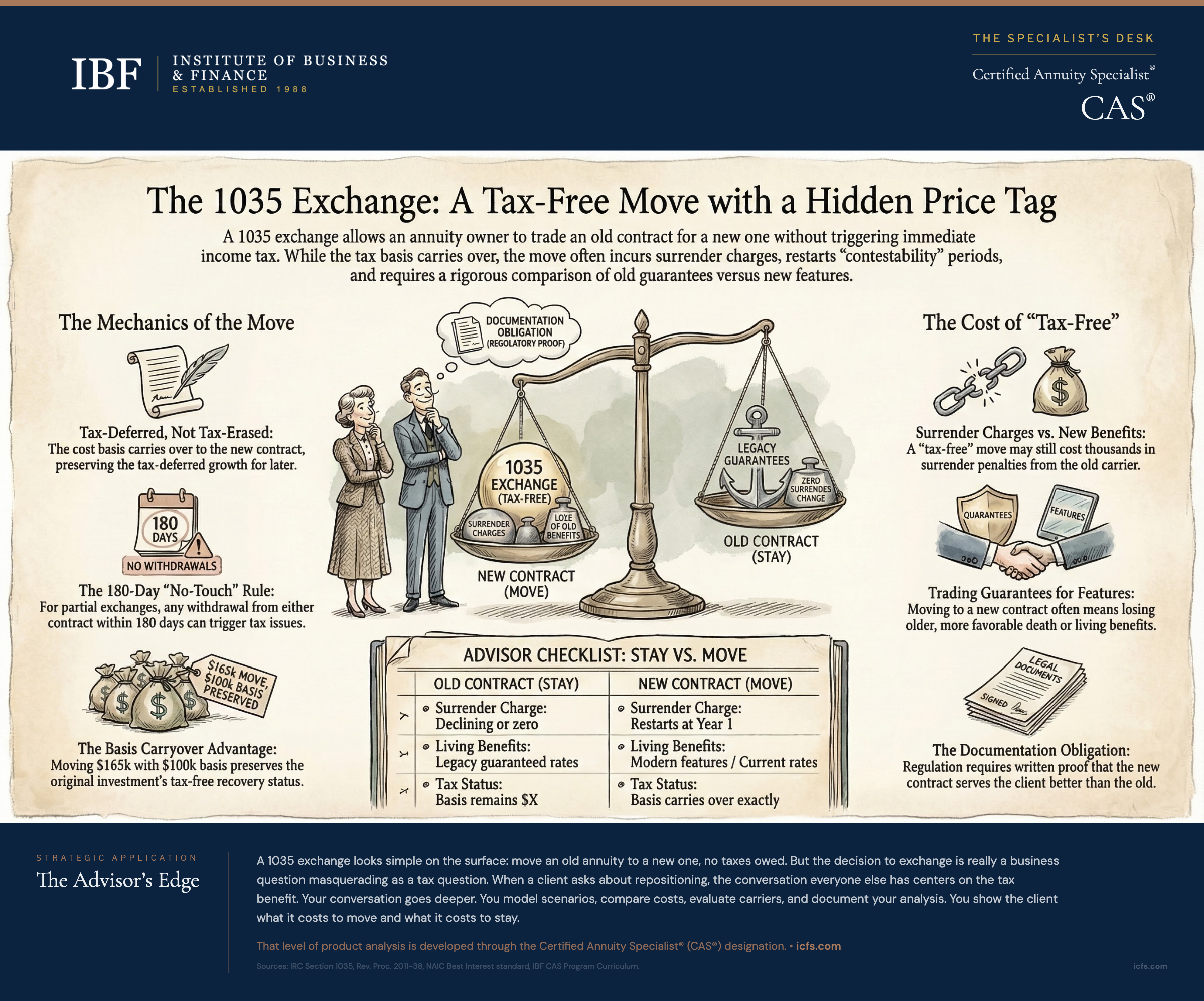

What 1035 Exchange Actually Does

The mechanics are simple. The cash value from the old contract moves to a new contract with a new carrier or a different product from the same carrier. The owner and annuitant remain the same. Most importantly, the cost basis from the old contract carries over. If you paid $100,000 for an annuity that is now worth $140,000, you had $40,000 of gain. When you 1035 exchange to a new contract, the gain does not disappear. It simply transfers to the new contract, where it will be recognized later when you take distributions.

This is the critical point: tax-free does not mean tax-erased. It means tax-deferred. The exchange itself triggers no tax, but the gain remains embedded in your contract until you withdraw it.

Consider the mechanics with a concrete example. Sarah purchased an annuity ten years ago with a $100,000 premium. The current value is $165,000, giving her $65,000 of accumulated gain. Her contract has a 7-year surrender period she entered only two years ago. The surrender charge is 5%, which would cost her $8,250 to exit now.

Sarah wants to move to a new product with better features. Under Section 1035, she exchanges the $165,000 value to a new contract. She recognizes no gain on the exchange itself. The new contract has $165,000 value and $100,000 basis. The $65,000 gain is embedded in the new contract, just as it was in the old one.

The Hidden Cost: Surrender Charges

This is where many 1035 exchange conversations derail. The exchange itself is tax-free, but getting out of the old contract is not free. Sarah’s old contract still has a surrender period running. Moving to a new contract requires surrendering the old one, which triggers surrender charges.

In Sarah’s case, she pays $8,250 to exit ($165,000 value times 5% surrender charge). That $8,250 comes directly from her contract value. The new contract receives $156,750 instead of the full $165,000. She has lost money, not to taxes, but to surrender penalties.

The decision calculus shifts immediately. Is the new contract better enough to justify an $8,250 penalty? That requires modeling the new contract’s features and expected performance against the old one.

Sometimes the answer is yes. If the new contract carries fees or crediting limitations that will cost more than $8,250 over the remaining years, the exchange makes sense. If the old contract is simply mediocre and the new one is marginally better, the exchange does not make sense.

Advisors often fall into a trap here: focusing on the tax benefit ("you won’t owe any taxes") while minimizing the surrender charge ("it’s just 5%"). For Sarah, "just 5%" is $8,250. That is real cost that has to be justified.

The Advantage: Basis Carryover and Tax Treatment

The flip side of the hidden cost is the genuine advantage. When you exchange, your basis carries over intact. Sarah’s $100,000 basis comes forward to the new contract. When she eventually withdraws from the new contract, she will recover that $100,000 tax-free, and the remaining $65,000 (plus any new gains) will be taxable.

Compare that to a taxable sale and reinvestment. If Sarah had surrendered the old contract and taken the $156,750 after surrender charges, she would have recognized $65,000 of gain at the time of withdrawal. She would have owed tax on that gain immediately. She could then invest the after-tax proceeds in a new annuity, but the new contract would have lower basis because she already paid tax on the gain.

The 1035 exchange preserves the tax deferral embedded in the old contract. This preserves compounding. The basis comes forward, and the new contract can grow from that higher starting value.

The New Contestability Period

This is a detail that catches clients off guard. When you exchange into a new contract, you restart the surrender period and contractual evaluation window with the new carrier. Most deferred annuity contracts do not involve health underwriting, so health-based contestability is not the primary concern for most exchanges.

For older clients or those with existing health issues, the relevant concerns are different. You lose the contract features of the old contract: death benefit guarantees, living benefit riders at favorable terms, or guaranteed minimum rates that are no longer available from the new carrier. If Sarah is 68 years old and exchanges into a new contract, the new carrier offers a fresh start with its own contractual terms, but those terms may not replicate the guarantees she had in her previous contract.

This is rarely a reason to avoid an exchange, but it is worth pricing the difference and disclosing to the client.

Partial 1035 Exchanges and the 180-Day Rule

Not every exchange has to be all-or-nothing. The IRS permits partial 1035 exchanges, where you move only a portion of an old contract to a new one, leaving the rest in the original contract. Rev. Proc. 2011-38 (effective October 24, 2011) explicitly confirms that partial exchanges apply regardless of whether the two contracts are from the same or different companies.

This can be valuable if you like some features of the old contract but want to upgrade part of it. Move the growth into a better product, and leave the income annuitant portion with the current carrier.

The catch: the 180-day rule under Rev. Proc. 2011-38. If you take a partial 1035 exchange, neither the old nor the new contract can have withdrawals within 180 days of the exchange. The safe harbor is binary: no withdrawal from either contract within 180 days equals tax-free exchange. There is no exception list or carve-outs, except for amounts received as an annuity for a period of 10 years or more, or during one or more lives (income-for-life or SPIA annuitization).

When the 180-day rule is violated, under Rev. Proc. 2011-38, a withdrawal within 180 days does not automatically make the entire exchange taxable. The IRS applies general tax principles to determine the tax treatment based on all facts and circumstances. The transaction may be treated as boot in a tax-free exchange or as a taxable distribution.

This is a critical rule that clients must understand. Mark their calendar 180 days out. Do not let them make a withdrawal thinking they can work around it. Improper withdrawals will be subject to tax treatment under IRS examination.

Exchange Into an Existing Contract

You can exchange into a brand-new contract with a new carrier, or you can exchange into an existing contract you already own from the same carrier. This second option can be useful for eliminating duplicate contracts or consolidating into a single account to reduce fees.

Some carriers have specific forms allowing this. If the carrier permits it, the same basis carryover rules apply. Verify with the carrier before attempting this approach.

The Bigger Decision: Replacement Analysis

The tax mechanics are clear. The harder question is whether the exchange makes business sense.

Start with the fundamental analysis any advisor should perform before recommending any annuity replacement: compare the surrender charges and penalties of the old contract to the benefits of the new one.

What are the surrender charges remaining on the old contract? What will they decline to if you wait one more year? Is the new contract so superior that it justifies accelerating the exit?

What features exist in the old contract that you will be giving up? Some older contracts have living benefit riders, death benefit enhancements, or guaranteed minimum rates that are no longer available. If you exit the old contract, those features disappear. The new contract may offer something similar, but it may not be identical. Price the difference.

What is your timeline? If the client is 72 years old and plans to start withdrawals in two years, waiting out a surrender period may not make sense. If the client is 48 years old and has 30 years of accumulation ahead, a few years of patience might be worth avoiding surrender charges.

What is your confidence in the new carrier? You are asking the client to commit to a new company for potentially a decade or more. Is the new carrier’s financial strength better or equivalent? Is the new carrier’s history with contract owners reliable? A lower fee structure is attractive only if the carrier will be around to honor it.

The Advisor’s Obligation: Documented Comparison

Regulators have flagged annuity replacement as a problem area. When clients move from one annuity to another, they often do not understand they are restarting surrender periods, losing benefits, or incurring immediate costs. This creates compliance risk and relationship damage.

Before recommending a replacement, document your analysis. Create a side-by-side comparison showing:

The surrender charges in the existing contract and when they decline. The crediting mechanisms or income rates available in the old contract versus the new one. The rider costs and features in each. The financial strength ratings of the old and new carriers. The timeline for when the client might need access to funds.

Then document your conclusion. Why does the new contract serve this client better, even after accounting for surrender charges and any lost features? If you recommend keeping the existing contract, document that you evaluated replacement and determined it was not in the client’s best interest.

This documentation is not optional under the NAIC Best Interest standard. The Care Obligation requires a reasonable basis for your recommendation. The Documentation Obligation requires you to record that analysis in writing. Documentation is how you satisfy both.

When 1035 Exchanges Make Sense

The clearest cases for exchanges are when the old contract has completed its surrender period. If surrender charges have expired, the only costs are the structural ones: new contestability period, change of carriers. These are manageable.

Also clear: when the old contract has genuine problems. A carrier experiencing financial difficulty, a contract with crediting rates that have dropped so far that they no longer compete, a product with riders that no longer fit the client’s needs. These warrant exchanges despite remaining surrender charges.

The grayer cases: when the new contract is marginally better and significant surrender charges remain. These require client conversation and documented analysis showing why the marginal improvement justifies the immediate cost.

Client Conversation Framework

When a client asks about moving to a new annuity, structure the conversation this way.

First, understand why they want to move. Is it fees? Crediting performance? A feature they need that the old contract lacks? Or just a general feeling that they could do better? The reason matters because it points to whether the new contract actually solves the problem.

Second, examine the old contract’s fine print. How long is the remaining surrender period? What will surrender charges cost? What features exist that they might lose? What does their basis look like compared to the current value?

Third, model the new contract. Run scenarios showing what they would earn in the new contract under different market conditions. Compare total costs in the new contract to the total cost of staying in the old one, including both the surrender charges and the ongoing crediting differences.

Fourth, present the analysis neutrally. Not "you should move" or "you should stay," but "here is what it costs to move, here is what it costs to stay, and here is how the products compare." Let the client make the decision with full information.

Finally, document your analysis and the client’s decision. If they choose to move, the documentation protects you. If they choose to stay, the documentation shows you evaluated replacement and determined it was not advisable for their situation.

Key Takeaways

- Section 1035 allows tax-free exchanges between annuities, with basis carrying over intact. The gain remains embedded in the new contract but defers taxation until distribution.

- Surrender charges in the old contract create real costs that must be compared against the benefits of the new contract. Tax-free does not mean cost-free.

- A new contract restarts the surrender period and contractual evaluation window. For older clients, the concern is losing existing contract guarantees and benefits, not health-based contestability.

- Partial exchanges are permitted under Rev. Proc. 2011-38 but subject to a 180-day withdrawal restriction on both old and new contracts. Violations are treated under general tax principles based on facts and circumstances, not automatic full gain recognition.

- Before recommending replacement, perform documented side-by-side analysis comparing surrender charges, crediting mechanisms, rider features, and carrier strength. This analysis is required under the NAIC Best Interest standard.

- The clearest cases for exchanges are when surrender periods have expired or when the old contract has genuine problems (carrier concerns, inadequate crediting, missing features).

The Advisor’s Edge

A 1035 exchange looks simple on the surface: move an old annuity to a new one, no taxes owed. The mechanics are in every product guide and every carrier’s training materials. Any advisor can explain how basis carries over.

What transforms a tax question into a planning conversation is the ability to model scenarios: calculating whether surrender charges are justified by the new contract’s advantages, identifying contract features that cannot be replaced, pricing the difference between old and new carrier guarantees, and documenting the analysis to meet the NAIC Best Interest standard. That work requires structured analytical training, not just product familiarity.

The Certified Annuity Specialist® (CAS®) designation develops that level of product evaluation and replacement analysis expertise across 18 chapters covering every major annuity category.

For a closer look at how living benefit riders work (one of the key features to evaluate in any replacement analysis), see Variable Annuity Living Benefits: GMWB, GLWB, GMIB, and GMAB Explained.