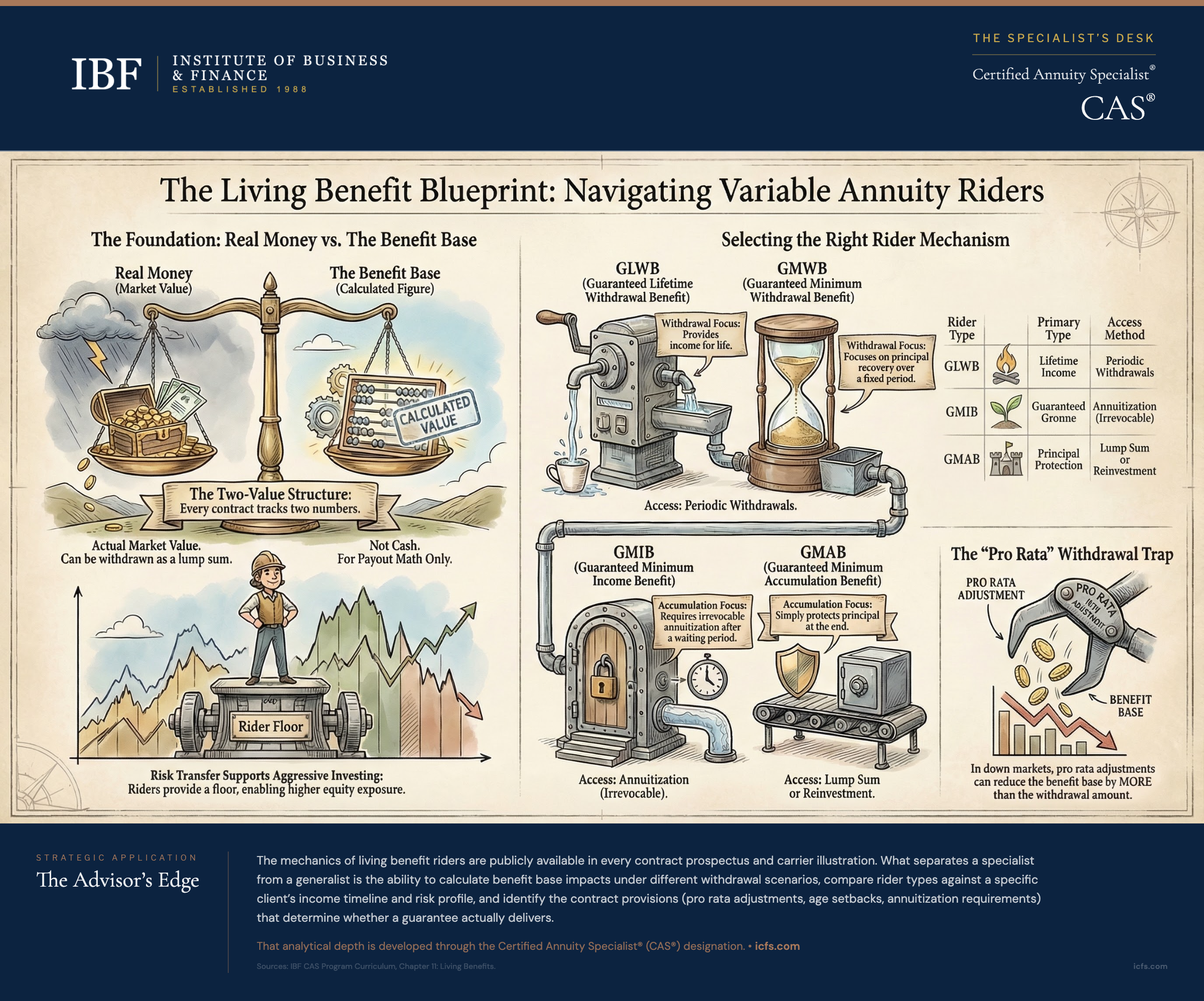

Every variable annuity with a living benefit rider carries two numbers your client needs to understand, and one of them is not real money.

The contract value is the actual market worth of the underlying subaccount investments, minus any applicable surrender charges. This is what the owner receives upon full liquidation. The benefit base is a separate, calculated figure used solely to determine guarantee payouts. It often has no connection to what the contract is actually worth. In a strong market, the contract value may exceed the benefit base by a wide margin. After a downturn, the benefit base may be double the contract value. The benefit base is a calculation, not a balance. No one can withdraw it as a lump sum.

This two-value structure is the foundation of every living benefit conversation. Advisors who skip over it create confusion that surfaces months or years later, usually when a client reviews their statement and cannot reconcile the two figures. Getting this distinction right from the start prevents the most common client complaint about living benefit contracts.

The Four Rider Types

The earliest living benefit riders (GMIB and GMAB) emerged in the mid-to-late 1990s. GMWB followed in 2002, with GLWB developing shortly after. All four expanded rapidly through the mid-2000s before the 2008 market crisis reshaped the competitive landscape. The name describes exactly what they do: provide guarantees to the contract owner while the owner is alive, as opposed to death benefit riders that pay beneficiaries after the owner dies.

There are four types. Each addresses a different client concern, uses a different activation timeline, and imposes different distribution requirements. Picking the wrong one for a given client is worse than not having a rider at all, because the client pays for a guarantee that does not match how they actually need income.

GMWB: Principal Recovery

The Guaranteed Minimum Withdrawal Benefit is the simplest of the four. It guarantees the owner can withdraw a fixed percentage annually, typically 5-10%, until 100% of the original investment is recovered. The guarantee is not lifetime income. It is principal recovery over a defined period.

Consider Jane, who invests $50,000 in a variable annuity with a 7% GMWB rider. She selects an aggressive portfolio and starts withdrawals immediately. Even if her investments decline 22% annually, she receives $3,500 each year for at least 14.3 years (100% divided by 7% = 14.3 years).

If her portfolio instead earns 4% annually while she withdraws 7%, the positive returns partially offset each withdrawal. Her payments extend from 14.3 years to approximately 21-22 years before the contract value depletes.

The GMWB establishes a floor, not a ceiling. Positive investment performance extends the payout period. The guarantee kicks in only when markets fail to support the withdrawal rate.

Two features separate better GMWB contracts from weaker ones. Step-up provisions lock in market gains to the benefit base on anniversary dates, permanently increasing the principal the guarantee protects. And contracts differ on excess withdrawal treatment: taking more than the guaranteed percentage in any period may reset the benefit base to the current contract value, which in a declining market can destroy the guarantee entirely.

GLWB: Lifetime Income

The Guaranteed Lifetime Withdrawal Benefit extends the GMWB concept from principal recovery to lifetime income. Annual payments continue as long as the annuitant lives, even if the contract value drops to zero.

The distinction from GMWB matters more than most advisors recognize. A GMWB promises return of principal over a fixed period. A GLWB promises income for life, regardless of how long the owner lives or how markets perform. That longevity protection is the core value.

GLWB withdrawal rates typically increase with age. A 60-year-old might receive 5% annually, while a 70-year-old might receive 6%. This reflects actuarial reality: older annuitants have shorter remaining life expectancies, so the insurer can afford a higher annual percentage. The increasing rate also creates an incentive to delay activation, which benefits both the owner (higher payments) and the insurer (fewer total payment years).

Ken invests $100,000 in a variable annuity with a GLWB offering 5% lifetime withdrawals. He receives at least $5,000 annually for life. If he lives to 110, the payments continue at $5,000 per year even though the contract value ran out years ago. If his investments perform well, step-up features may ratchet the benefit base higher, permanently increasing his income.

Joint coverage options extend payments until the second covered person dies, typically at slightly reduced rates. For married couples whose primary retirement concern is outliving their money, joint GLWB coverage transfers that specific risk to the insurer.

GMIB: Guaranteed Accumulation Plus Annuitization

The Guaranteed Minimum Income Benefit takes a fundamentally different approach. It guarantees a minimum accumulation rate, commonly in the mid-single digits, applied to the benefit base over a required holding period of 7-10 years. After that waiting period, the owner can annuitize at the guaranteed amount.

The keyword is annuitization. Unlike GMWB and GLWB, which allow periodic withdrawals from the contract, the GMIB typically requires the owner to irrevocably convert the account into a lifetime income stream. That is a permanent decision with no reversal.

Angie invests $100,000 in a variable annuity with a 6% GMIB at a cost of approximately 1% per year. After 10 years, her investment choices produced a contract value of only $125,000. The guaranteed 6% compounding grew the benefit base to approximately $180,000.

Angie now has three options. She can ignore the GMIB, take her $125,000, and invest elsewhere with full flexibility. She can activate the GMIB, accept the $180,000 benefit base, and annuitize. Or she can wait, letting the 6% guarantee continue compounding while hoping the contract value improves.

The decision hinges on a feature many advisors overlook: the age setback. Many GMIB contracts calculate annuitization payouts as if the annuitant is younger than their actual age, often by several years. A 70-year-old activating a GMIB with a 5-year setback receives payments calculated for a 65-year-old’s life expectancy. The annual payment drops accordingly. Before recommending a GMIB, request hypothetical illustrations showing annuitization payouts with and without the age setback. The benefit base number means nothing in isolation. What matters is the actual dollar amount the client will receive each year.

GMAB: Principal Protection

The Guaranteed Minimum Accumulation Benefit guarantees that after a holding period (typically 10 years), the contract value will equal at least 100% of premiums paid, regardless of investment performance. No annuitization required. No distribution schedule imposed.

Ken invests $200,000 in a GMAB contract with principal protection after 10 years. Despite selecting aggressive subaccounts, his contract loses $110,000 by the tenth anniversary, leaving only $90,000 in contract value. The GMAB guarantee restores his value to $200,000. He can take the money in a lump sum, roll it into another product via 1035 exchange, or leave it invested.

The GMAB is the most flexible of the four riders, and also the most limited. It does not provide income. It does not offer longevity protection. It simply guarantees that principal is intact after a defined holding period. If cumulative returns are positive after the holding period, the owner ignores the GMAB and keeps their market gains. The guarantee only matters if markets have failed to return principal over 10 years, which is rare but not impossible.

GMAB suits clients who want equity exposure with a defined safety net, have a time horizon matching the holding period, and value lump sum access over guaranteed income streams.

The Withdrawal Trap: Dollar-for-Dollar vs. Pro Rata

How early withdrawals affect the benefit base is one of the most consequential contract details in any living benefit, and one of the least discussed during the sales process.

Under dollar-for-dollar adjustments, each withdrawal dollar reduces the benefit base by one dollar. This is simple and intuitive. A $10,000 withdrawal from a contract with a $120,000 benefit base leaves a $110,000 benefit base.

Under pro rata adjustments, each withdrawal reduces the benefit base by the same percentage it represents of the contract value. In a declining market, this magnifies the damage.

Consider a contract with a $100,000 original investment, now worth $80,000 in contract value, with a $100,000 benefit base. The owner withdraws $6,000. That withdrawal represents 7.5% of the $80,000 contract value. Under pro rata rules, the benefit base drops by 7.5%: from $100,000 to $92,500. The client took out $6,000 but lost $7,500 from the benefit base. In a rising market, the same math works in the owner’s favor, but living benefit guarantees are most needed in exactly the declining markets where pro rata adjustments do the most harm.

Some contracts use a bi-level formula: dollar-for-dollar adjustments up to the guaranteed withdrawal limit, then pro rata adjustments on excess amounts. This protects the benefit base for normal withdrawals while penalizing excess withdrawals more severely.

Before any withdrawal from a living benefit contract, verify the adjustment method. Then calculate the actual benefit base impact. Telling a client “you can take money out anytime” without explaining the pro rata consequences is an incomplete conversation.

Why Living Benefits Support Aggressive Investing

This is counterintuitive, but the logic is sound. Living benefits transfer investment risk to the insurer. That risk transfer supports aggressive investing, not conservative investing.

If aggressive investments succeed, the owner captures the gains and the benefit base steps up. If aggressive investments fail, the living benefit guarantee provides the floor. The owner cannot lose below the guaranteed amount.

Investing conservatively with a living benefit means paying for a guarantee while simultaneously limiting the upside that makes the guarantee worth its cost. If a client would choose conservative investments anyway, the living benefit rider fee may not be justified. Conservative investments like bond funds may return amounts comparable to what the guarantee floor already provides.

This is why most living benefit contracts restrict subaccount options, often limiting equity exposure and requiring allocation to managed volatility portfolios. The insurer needs to manage hedging costs, which increase with portfolio volatility. Investment restrictions are the trade-off for the guarantee.

The Real Cost Question

Variable annuities with living benefits can carry total annual expenses exceeding 3%, including subaccount management fees, administrative and mortality expenses (M&E charges), and the living benefit rider cost itself.

But the annual expense ratio is not the full cost picture. The bigger cost consideration is how the account liquidates once the benefit activates. Distribution schedules, age setbacks, required annuitization, and withdrawal adjustment methods all affect the actual value the client receives. An advisor who focuses only on the rider’s basis point cost is missing the more consequential terms.

When evaluating a living benefit for a client, compare three scenarios. First, the variable annuity with the living benefit: higher annual costs, guaranteed floor, risk transfer. Second, the same variable annuity without the rider: lower costs, full market risk. Third, alternative products entirely: ETFs, mutual funds, fixed annuities, or immediate annuities, each with different risk, cost, and flexibility profiles.

The comparison should be specific to the client’s timeline, income needs, risk tolerance, and estate planning objectives. A 55-year-old accumulating for retirement faces a different calculation than a 68-year-old converting savings to income.

When Living Benefits Pay Off and When They Don’t

The purpose of a living benefit is not to maximize wealth. It is to minimize the chance of failure, meaning running out of money before running out of life.

Living benefits are most valuable for clients who face a 25-30 year or longer retirement horizon, where the probability of portfolio depletion under systematic withdrawals increases with time. They are valuable for clients with limited ability to reduce spending if markets decline, because the guaranteed floor provides income regardless of investment performance. And they are valuable for clients who will actually use the guarantee as intended, meaning clients who understand the withdrawal rules, the distribution schedule, and the activation requirements.

Living benefits are least valuable for clients with short time horizons, where the holding period may not be met before income is needed. They are a poor fit for clients who need full liquidity, because surrender charges and benefit base reduction penalties limit access. And they add cost without proportional value for clients with substantial other income sources, where the “failure probability” the rider protects against is already low.

Where This Analysis Stops

This article covers the mechanics: how each rider type works, how withdrawals affect benefit bases, and how to evaluate cost against value. It does not cover the tax treatment of living benefit distributions (which varies by qualified vs. non-qualified status), the regulatory suitability standards that apply to living benefit sales (including Reg BI implications), or the carrier-specific variations that exist across hundreds of active contracts. Those topics require separate treatment, and several are covered in depth in the CAS program curriculum.

It also does not address the insurer’s ability to honor guarantees over 20-30 year periods. Carrier financial strength ratings, hedging program quality, and concentration of living benefit exposure all affect whether the guarantee on paper translates to payments in practice. After the 2008 market decline, several carriers reduced guarantees, raised costs, or exited the living benefit market entirely.

The Client Conversation

The most common client misunderstanding about living benefits is treating the benefit base as a real balance. When a client sees a $150,000 benefit base on a contract worth $95,000, the instinct is to believe they “have” $150,000. Correcting this misunderstanding is not a one-time conversation. It needs reinforcement at every annual review, especially in down markets when the gap between the two values is widest.

Start with the analogy that works: the benefit base is like an insurance policy’s coverage limit. A homeowner with $400,000 in coverage does not have $400,000 in their pocket. They have a promise that if something goes wrong, the insurance company will make payments based on that figure. The benefit base works the same way. It is the number the insurance company uses to calculate what they owe the owner, not the amount the owner can walk away with.

From there, the conversation shifts to the specific guarantee: what triggers it, how payments are calculated, and what restrictions apply. This is where the four rider types diverge, and where knowing the details of the actual contract matters more than knowing the category name.

Key Takeaways

- Every living benefit contract carries two values: the contract value (real money) and the benefit base (guarantee calculation). Confusing these with your client guarantees problems at the first annual review.

- GMWB and GLWB allow periodic withdrawals without a required accumulation period, though many contracts impose age minimums or short deferral windows. GMIB and GMAB impose structured holding periods of 7-10 years. Match the rider type to the client’s income timeline, not just their risk tolerance.

- Pro rata withdrawal adjustments magnify benefit base losses in declining markets. Before any withdrawal, verify the adjustment method and calculate the actual impact. Dollar-for-dollar is more favorable in down markets.

- Living benefits logically support aggressive investing because the guarantee provides the floor. Conservative investing with a living benefit means paying for protection while limiting the upside that makes the protection worthwhile.

- The annual rider cost is not the full expense. Distribution schedules, age setbacks, required annuitization, and excess withdrawal penalties determine whether the guarantee actually delivers what the client expects.

The Advisor’s Edge

The mechanics of living benefit riders are publicly available in every contract prospectus and carrier illustration. Any advisor can read about GMWB, GLWB, GMIB, and GMAB in a product brochure.

What separates a specialist from a generalist is the ability to calculate benefit base impacts under different withdrawal scenarios, compare rider types against a specific client’s income timeline and risk profile, and identify the contract provisions (pro rata adjustments, age setbacks, annuitization requirements) that determine whether a guarantee actually delivers. That analysis requires structured training in annuity product design, not just familiarity with acronyms.

The Certified Annuity Specialist® (CAS®) program develops that analytical depth across 18 chapters covering every major annuity category, from fixed-rate structures through variable subaccounts, FIA crediting methods, and RILA buffer mechanics.

For a detailed breakdown of how FIA crediting methods work (the other major product category in today’s annuity market), see Fixed Indexed Annuity Crediting Methods Explained.

Sources and Notes: Living benefit mechanics and rider type descriptions drawn from IBF CAS program curriculum, Chapter 11: Living Benefits. Rider cost ranges, withdrawal rate schedules, and age setback features reflect general industry patterns; specific contract terms vary by carrier. This article is refreshed annually.