When Tax-Loss Harvesting Actually Creates Value

Most advisors understand the basic idea behind tax-loss harvesting: sell a position at a loss, use that loss to offset gains or income, and reinvest in something similar to maintain market exposure. Simple enough in theory. In practice, execution is where the value lives or dies.

The difference between a well-run harvesting program and a sloppy one is not philosophical. It is mechanical. It comes down to how often you look, how you handle the wash sale rule across multiple accounts, which lots you select, and whether you are building a repeatable process or just scrambling in December. This guide walks through the mechanics that separate advisors who generate real tax alpha from those who leave it on the table.

The Loss Budget: Thinking About Losses as Tax Assets

Before getting into mechanics, it helps to reframe the way you think about losses. Most investors and many advisors treat unrealized losses as a problem. They are not. They are a resource.

A harvested loss is a tax asset with a defined dollar value. At a 23.8% combined federal rate (20% long-term capital gains plus 3.8% net investment income tax), a $50,000 harvested loss is worth $11,900 in avoided taxes when used to offset long-term gains. Even at the 15% rate, that same loss saves $7,500. Losses that exceed current-year gains can offset up to $3,000 of ordinary income per year, with unlimited carryforward. That $3,000 limit has not been adjusted for inflation since 1978, which makes it worth far less in real terms than it once was, but the unlimited carryforward means large harvested losses can provide value for years.

Thinking in terms of a “loss budget” changes how you manage portfolios. Instead of viewing a market decline as purely negative, you evaluate which positions now carry harvestable losses, what the tax value of those losses would be, and whether harvesting now or waiting makes more tactical sense. The loss budget becomes part of the annual planning conversation alongside rebalancing and cash flow.

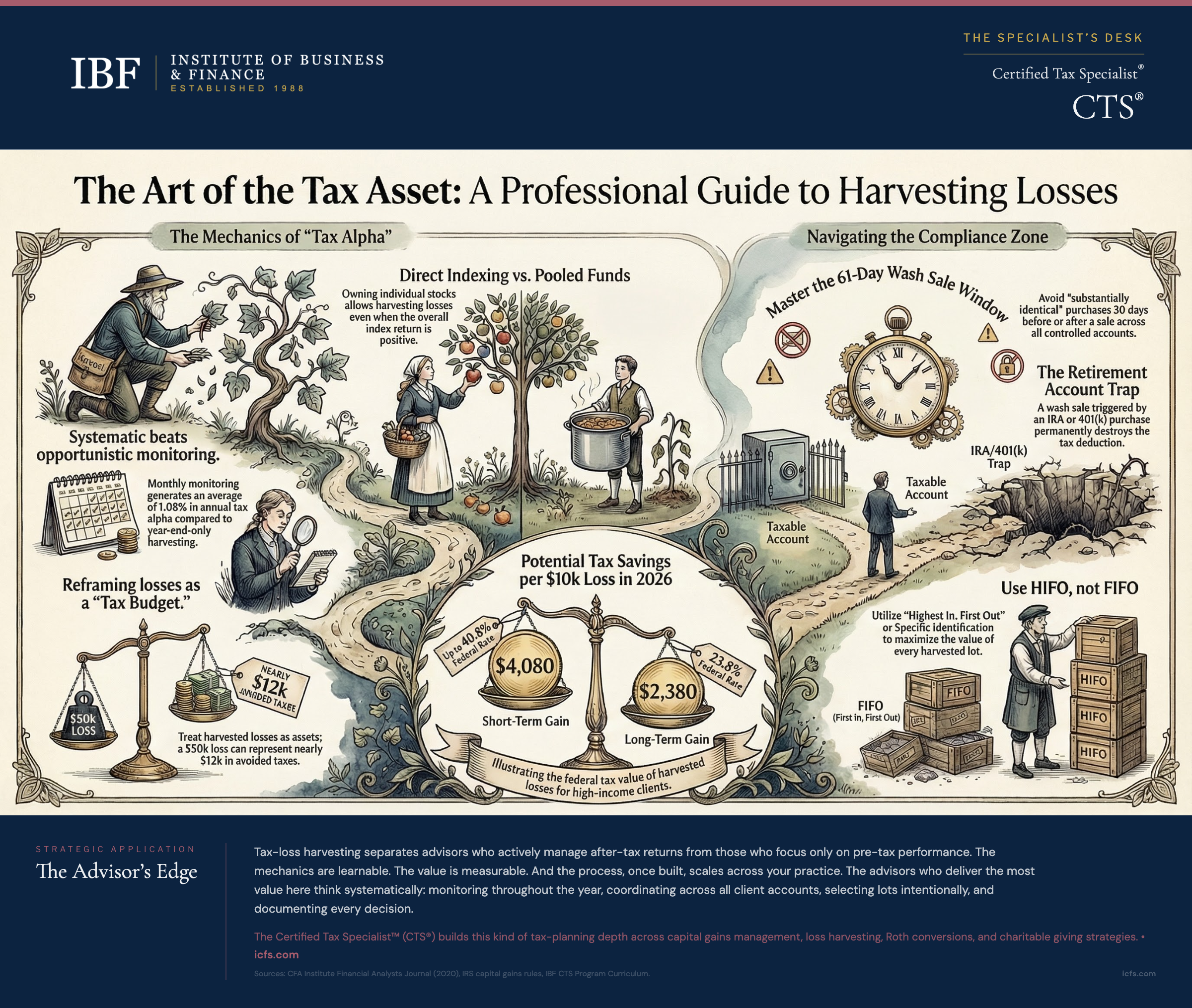

Systematic vs. Opportunistic: Why Frequency Matters

There are two approaches to tax-loss harvesting. The first is opportunistic: you look at the portfolio once or twice a year, usually in Q4, and harvest whatever losses happen to exist. The second is systematic: you monitor positions continuously (or at regular intervals throughout the year) and harvest losses whenever they cross a defined threshold.

Research consistently shows that systematic harvesting captures significantly more value. A study published in the CFA Institute’s Financial Analysts Journal (Chaudhuri, Burnham, and Lo, 2020) found that systematic monthly monitoring and harvesting generated an average of 1.08% in annual tax alpha relative to a non-harvesting baseline (0.82% after accounting for wash sale constraints; the study assumed 15% long-term and 35% short-term capital gains tax rates, which differ from 2026 rates). Research from Smartleaf estimates that year-round harvesting is 1.5 to 2 times more effective than year-end-only approaches. The reason is straightforward: losses are volatile. A position that is down 12% in March may be flat by October. If you only look in December, you miss the March opportunity entirely.

Systematic harvesting does not mean daily trading. A monthly or quarterly review cadence, combined with threshold triggers (for example, harvesting when an individual position shows a loss exceeding $5,000 or 5% of position value), captures most of the available benefit without excessive transaction costs. The key is having a defined process with consistent execution, not reacting to every red number on a screen.

For advisors running multiple client portfolios, the operational challenge is real. Systematic harvesting requires tracking cost basis at the lot level, monitoring wash sale windows across accounts, and coordinating with any automated rebalancing tools. The payoff justifies the effort, but only if the process is built to scale.

The Wash Sale Rule: Where Most Mistakes Happen

The wash sale rule is simple to state and surprisingly easy to violate. If you sell a security at a loss and purchase a “substantially identical” security within 30 days before or after the sale, the loss is disallowed. The 61-day window (30 days before, the sale date, 30 days after) is the compliance zone.

Three aspects of the wash sale rule trip up advisors more than any others.

Cross-account application. The wash sale rule applies across all accounts the taxpayer controls. If you harvest a loss on a stock in a client’s taxable brokerage account and their 401(k) buys the same stock through an automatic contribution within the 61-day window, the loss is disallowed. This is worse than a standard wash sale between taxable accounts, because when the replacement purchase happens inside an IRA or 401(k), the disallowed loss does not get added to the basis of the new shares. It is permanently lost. The deduction simply vanishes. IRS Revenue Ruling 2008-5 explicitly addresses IRAs and Roth IRAs; the same treatment is broadly applied to 401(k)s by practitioners as a conservative position, though the IRS has not issued a parallel ruling for employer-sponsored plans. The practical advice remains the same: avoid the situation entirely by checking retirement plan holdings before harvesting. Advisors who manage taxable accounts but do not coordinate with retirement plan allocations are exposed to this risk every pay period.

“Substantially identical” is not clearly defined. The IRS has never published a definitive test for what makes two securities substantially identical. Identical ticker symbols obviously qualify. Shares of the same mutual fund qualify. But what about two S&P 500 index funds from different providers? Two large-cap value ETFs tracking different but overlapping indices? The IRS has not ruled definitively on these scenarios. The standard practice among tax professionals is that switching between funds tracking different indices (for example, selling an S&P 500 fund and buying a total market fund, or selling a Russell 1000 Value ETF and buying an MSCI USA Value ETF) is acceptable, because the underlying indices differ in construction and composition. But this is professional judgment, not IRS safe harbor. There is no bright-line rule, and advisors should document their rationale for the replacement security selection.

Timing discipline. The 30-day-before component of the wash sale window catches advisors who purchase a position and then decide to harvest a loss on the original holding. If a client buys additional shares of a stock and you then sell older lots of the same stock at a loss within 30 days, the wash sale rule applies. This matters for clients making regular contributions or automatic investments. You need to know what went into the account in the prior 30 days before you sell anything at a loss.

Replacement Security Strategy

When you harvest a loss, you typically want to maintain similar market exposure during the 31-day waiting period. The replacement security needs to be different enough to avoid the substantially identical standard but similar enough to keep the portfolio’s risk profile intact.

Common replacement strategies include swapping between index providers tracking different benchmarks (S&P 500 to total stock market, Russell 1000 to MSCI USA), switching between individual stocks in the same sector, and using ETFs to replace mutual fund positions or vice versa. The goal is to preserve the asset allocation while creating enough differentiation to satisfy the wash sale standard.

After the 31-day window closes, you can swap back to the original position if preferred. Some advisors maintain a permanent replacement strategy instead, using the swap as an opportunity to move into a preferred vehicle without creating the need to eventually swap back.

The tracking requirement is important: you need to record the replacement security, the date of the swap, and the date the 31-day window closes for every harvesting transaction. Without this, you risk inadvertent wash sales when future rebalancing or contributions reintroduce the original security too soon.

Direct Indexing: Maximum Harvesting Capacity

Direct indexing takes tax-loss harvesting to its most granular level. Instead of holding an index fund (which is a single security with a single cost basis), the investor owns the individual stocks that make up the index. Each stock is a separate tax lot with its own basis, which means losses can be harvested at the individual security level even when the overall index is positive.

Consider a year when the S&P 500 returns 12%. Inside that 12% return, some stocks are up 30% and others are down 15%. An investor holding the index fund has no losses to harvest because the fund itself is up. An investor holding the individual stocks through a direct indexing strategy can harvest losses on the declining positions while maintaining index-like exposure through the remaining holdings and replacement securities.

The tax alpha from direct indexing is highest in the early years after funding. Research suggests that first-year tax alpha can reach 1.5% to 2% or more in volatile markets, but it decays over time as cost bases are reset through harvesting and positions appreciate. After roughly a decade, the ongoing tax alpha typically settles to 0.3% to 0.5% per year. This decay curve matters for setting client expectations. Direct indexing is not a permanent 2% annual benefit; it is a front-loaded benefit that tapers.

Direct indexing is not appropriate for every client. It requires enough assets to hold enough individual stocks to approximate an index (most platforms require $100,000 to $250,000 minimums), and it increases the complexity of account management, cost basis tracking, and tax reporting. For clients with large taxable portfolios and high marginal rates, the math works well. For clients with smaller accounts or lower tax brackets, the complexity may not justify the incremental benefit over a well-managed ETF tax-loss harvesting program.

According to Fidelity’s 2024 RIA Benchmarking Study, over a third of RIAs managing more than $1 billion in assets are already offering direct indexing, with more actively evaluating it. Actual current usage across all advisor segments is lower (Cerulli Associates found 18% of advisors overall used direct indexing in 2024), but adoption is concentrated among larger firms. The category has moved from niche to mainstream, which means advisors who do not understand the mechanics risk losing client conversations to competitors who do.

Lot Selection: Specific Identification and HIFO

Tax-loss harvesting generates value only if you are selling the right lots. The default method at most brokerages is FIFO (first in, first out), which sells the oldest shares first. FIFO is rarely optimal from a tax perspective.

Specific identification allows you to choose exactly which tax lots to sell. This is the gold standard for tax-managed portfolios because it gives you complete control over both the amount of gain or loss realized and the character (short-term vs. long-term) of that gain or loss.

HIFO (highest in, first out) is the most common systematic alternative. By selling the lots with the highest cost basis first, HIFO minimizes the gain (or maximizes the loss) on each sale. For harvesting purposes, HIFO automatically targets the lots most likely to carry losses.

The holding period dimension adds a second layer of complexity. Short-term losses are more valuable than long-term losses when used to offset short-term gains, because short-term gains are taxed at ordinary income rates (up to 37% federal for 2026). A $10,000 short-term loss offsetting a short-term gain saves up to $3,700 in federal tax, while the same loss offsetting a long-term gain saves at most $2,380 (at the 23.8% combined rate). When selecting lots, consider both basis and holding period to maximize the tax value of each harvest.

To use specific identification, the investor must instruct the broker which lots to sell at or before the time of sale, and the broker must confirm the instruction in writing. Most modern brokerage platforms support lot-level selection through their trading interfaces, but the advisor needs to ensure the account is set up for specific identification rather than defaulting to FIFO or average cost.

The Capital Gains Rate Landscape

Understanding the current rate structure puts the dollar value of harvesting into context. For 2026, long-term capital gains rates are 0%, 15%, or 20%, depending on taxable income. Single filers with taxable income up to $49,450 and married couples filing jointly up to $98,900 fall in the 0% bracket. The 20% rate kicks in at $545,500 for single filers and $613,700 for joint filers. Everyone in between pays 15%.

On top of the capital gains rate, high-income investors face the 3.8% net investment income tax (NIIT) on the lesser of net investment income or the amount by which modified AGI exceeds $200,000 (single) or $250,000 (married filing jointly). These NIIT thresholds have never been indexed for inflation, which means more taxpayers are subject to the surtax every year.

For a high-income client in the 20% bracket with NIIT exposure, the combined federal rate on long-term capital gains is 23.8%. Short-term gains face ordinary income rates up to 37%. At these rates, harvested losses carry significant dollar value, and the spread between short-term and long-term treatment makes holding period management a critical part of the harvesting decision.

Limitations: When Tax-Loss Harvesting Breaks Down

Tax-loss harvesting is valuable, but it is not free money. Several limitations are worth discussing with clients before building a harvesting program.

First, harvesting generally defers taxes rather than eliminating them. When you sell a position at a loss and reinvest in a replacement security, the replacement has a lower cost basis. The tax savings you capture today will be recaptured when you eventually sell the replacement at a larger gain. The value comes from the time value of money (paying taxes later is better than paying them now) and from the possibility that the gains will eventually be taxed at a lower rate, eliminated through charitable gifting, or stepped up at death. But for a client who plans to sell everything in a taxable account next year, the harvesting just shifts the tax from one year to the next.

Second, the $3,000 ordinary income offset limit constrains the annual value of losses that exceed capital gains. A client who harvests $100,000 in losses but has only $20,000 in gains can use $20,000 immediately and $3,000 against ordinary income, but the remaining $77,000 carries forward. The carryforward is unlimited, so the losses are not wasted, but the benefit is stretched over many years.

Third, tax-loss harvesting can create tension with investment discipline. If an advisor is constantly selling positions to harvest losses and buying replacements, the portfolio can drift from its target allocation. Transaction costs (even in a commission-free environment, there are bid-ask spreads and market impact costs) accumulate. And the behavioral temptation to let tax decisions drive investment decisions, rather than the other way around, is real. The tail should not wag the dog.

Fourth, state taxes add a layer of complexity. Some states conform to federal wash sale rules and capital gains treatment; others do not. State-level tax rates vary significantly and can shift the cost-benefit analysis of harvesting strategies. Advisors managing clients across multiple states need to account for these differences.

The Client Conversation: Framing Tax-Loss Harvesting

Many clients have heard of tax-loss harvesting but do not understand what it actually involves or what it is worth to them specifically. The conversation works best when you can show a dollar amount.

Start with a portfolio-level review. Pull up the unrealized gains and losses. Show the client how much in losses is currently available, what those losses would be worth at their marginal rate, and how harvesting would work mechanically. A statement like, “You have $35,000 in unrealized losses across these four positions. At your tax rate, harvesting those losses would save approximately $8,330 in federal taxes this year,” is concrete and compelling.

Then explain the process: you will sell the loss positions, immediately reinvest in similar but not identical securities to maintain market exposure, and after 31 days you have the option to swap back. The portfolio stays invested. The risk profile stays roughly the same. The tax bill goes down.

For clients with retirement accounts, address the coordination issue directly. Explain that you will need visibility into their 401(k) or IRA holdings to avoid wash sale violations, and discuss how automatic contributions should be managed during the 31-day window. This is a natural opportunity to demonstrate the value of holistic financial planning across all accounts.

For high-net-worth clients, the direct indexing conversation follows naturally. If a client has a $500,000 or larger taxable portfolio and a high marginal rate, showing them the incremental harvesting capacity from owning individual stocks versus an index fund makes the case on its own. Frame the tax alpha as a multi-year projection, not a single-year guarantee, and be transparent about the decay curve.

Key Takeaways

- Build a loss budget into every annual review. Pull unrealized losses across all client taxable accounts and calculate their dollar value at the client’s marginal rate. Present that number alongside the rebalancing and cash flow plan.

- Monitor monthly, not just in December. Set threshold triggers (e.g., harvest when an individual position loss exceeds $5,000 or 5% of position value) and review all taxable accounts on a monthly or quarterly cadence. Year-end-only harvesting leaves significant tax alpha on the table.

- Audit retirement plan holdings before every harvest. Pull the client’s 401(k), IRA, and HSA holdings and check for overlap with any position you plan to sell. (IRS guidance on HSAs in the wash sale context is less explicit than for IRAs, but the prudent approach is to treat them as within scope.) A wash sale triggered by a retirement account contribution permanently destroys the loss deduction.

- Document your replacement security rationale. For every swap, record why the replacement is not “substantially identical” (different index, different construction methodology, different provider). There is no IRS safe harbor, so your documentation is your defense.

- Set direct indexing expectations with a decay curve. When presenting direct indexing to high-net-worth clients, show multi-year projections that reflect the front-loaded benefit (1.5% to 2% year one) tapering to 0.3% to 0.5% after a decade. Do not pitch it as a permanent annual windfall.

- Use specific identification, not FIFO. Confirm that every client’s brokerage account is set to specific lot identification rather than the default FIFO method. Then select lots by both highest basis and holding period to maximize the tax value of each harvest.

The Advisor’s Edge

Tax-loss harvesting separates advisors who actively manage after-tax returns from those who focus only on pre-tax performance. The mechanics are learnable. The value is measurable. And the process, once built, scales across your practice.

The advisors who deliver the most value here are the ones who think systematically: monitoring throughout the year, coordinating across all client accounts, selecting lots intentionally, and documenting every decision. That discipline is what turns a well-known concept into actual dollars saved.

The CTS® designation builds this kind of tax-planning depth across capital gains management, loss harvesting, Roth conversions, charitable giving strategies, and more. To see the full scope of what CTS-designated advisors study, explore the program overview.

For tax strategies specific to business owners and exit planning, see Tax Strategies for Business Owners: QSBS, Opportunity Zones, and Exit Planning.

Sources and Notes: Content draws on CTS Module 1, Chapter 6 (Investment Taxation) and Module 2, Chapter 12 (Capital Gains Management). Tax alpha research referenced from the CFA Institute Financial Analysts Journal (2020). Capital gains rate thresholds and NIIT thresholds reflect IRS-published figures for the 2026 tax year. Direct indexing adoption data from Fidelity 2024 RIA Benchmarking Study and Cerulli Associates (2024). The $3,000 capital loss deduction limit is set by IRC Section 1211(b) and has not been adjusted for inflation since 1978. This article is refreshed annually or as tax law changes.