When Roth Conversions Actually Make Sense

Your 62-year-old client just retired. He has $1.8 million in a traditional 401(k), a pension starting in three years, and eleven years before Required Minimum Distributions begin at age 73. He asks: “Should I do Roth conversions?”

The answer depends on a straightforward economic question: Is it cheaper to pay taxes now or later? But the question also depends on several complications that most clients never consider.

A Roth conversion moves money from a traditional retirement account to a Roth account. The converted amount is taxed as ordinary income in the year of conversion. Once in the Roth, future growth and qualified distributions are tax-free. The fundamental trade-off is simple: pay taxes at today’s rates to avoid taxes at tomorrow’s rates.

Whether that trade makes sense depends on understanding your client’s current tax bracket, projecting their future tax bracket, calculating how long their money will remain invested, and then accounting for ripple effects on Medicare premiums and Social Security taxation.

The Mechanics: What Actually Happens in a Roth Conversion

Start with the basics. Your client has $100,000 in a traditional IRA. They convert the entire balance to a Roth IRA. The conversion is treated as a distribution from the traditional IRA, creating $100,000 of ordinary taxable income in the year of conversion.

If your client is in the 22% federal bracket (and we ignore state taxes for simplicity), they owe $22,000 in federal income tax. This is the critical point: the tax must be paid. If your client pays that $22,000 from outside retirement funds (a savings account, for example), then the Roth receives the full $100,000 and can begin growing tax-free immediately.

But here is what often happens in practice: the client does not have outside funds available. They pay the $22,000 tax from the IRA itself, leaving only $78,000 to convert. This reduces the conversion benefit substantially because they have fewer dollars compounding tax-free going forward.

For clients under age 59 1/2, the situation is worse. If they use IRA funds to pay the conversion tax, that portion triggers the 10% early withdrawal penalty on top of ordinary income tax.

Always recommend paying conversion taxes from non-retirement funds. It is the first decision that determines whether conversion makes sense at all.

Break-Even Analysis: How Long Until Conversion Pays Off

The break-even period answers a practical question: How many years must the converted funds remain invested before the Roth’s tax-free growth overcomes the upfront tax cost?

The math depends on three variables: the tax rate paid on conversion, the tax rate that would apply to future traditional distributions, and the investment return.

If your client converts at 22% and expects to withdraw in retirement at 22%, the Roth wins immediately. The longer the time horizon, the greater the advantage because tax-free compounding wins over tax-deferred growth.

If your client converts at 24% and expects to withdraw at 22%, they paid a higher rate now than they will pay later. This is not automatically bad. A longer time horizon and compound growth can still produce a Roth advantage. But the break-even period is longer: roughly eight years at 6% annual returns.

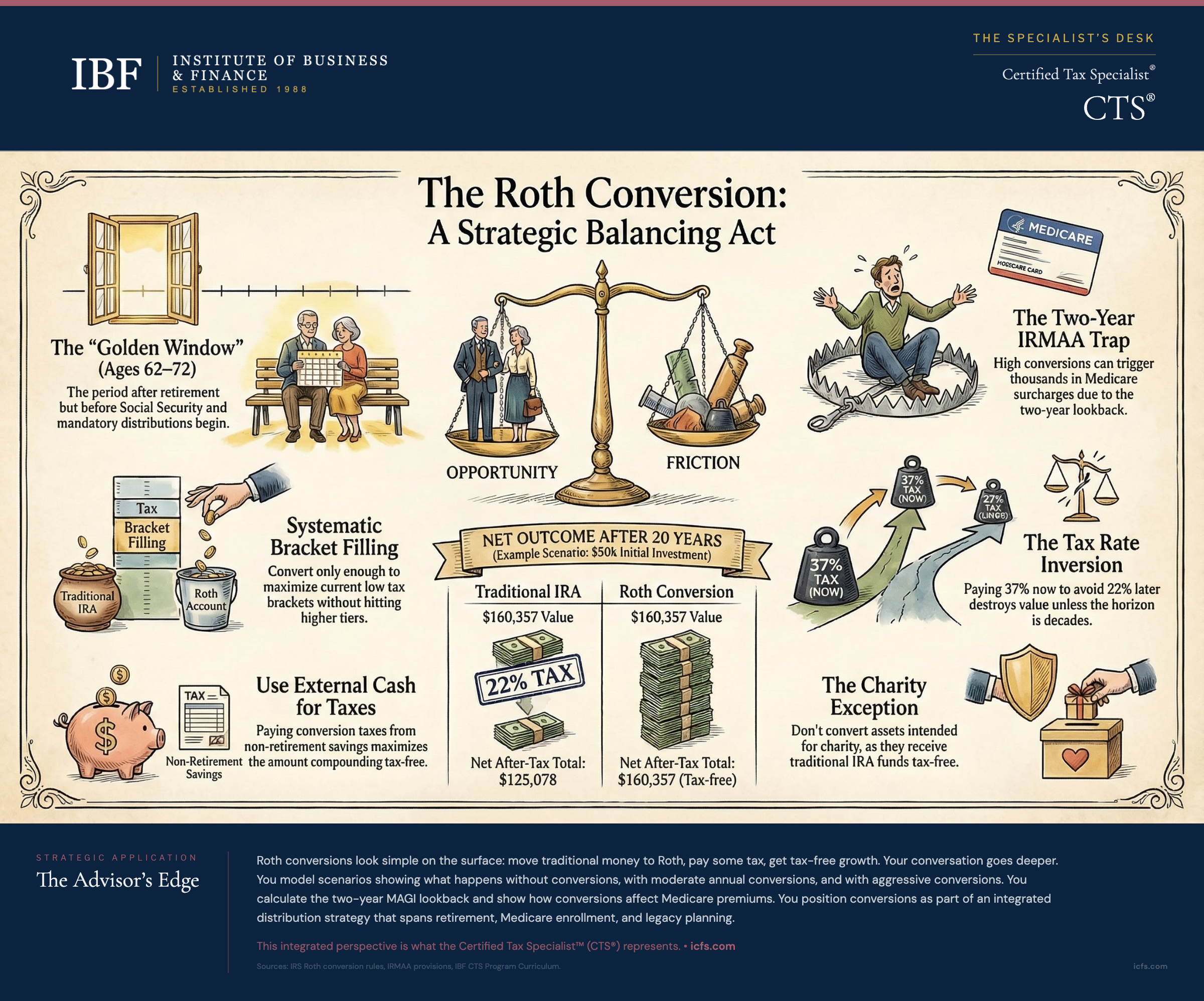

Consider Daniel, age 58. He is in the 24% bracket now. He expects to be in the 22% bracket in retirement. He converts $50,000, paying $12,000 in tax from his savings account. At 6% growth over 20 years, his Roth grows to $160,357, all tax-free. Without conversion, his traditional IRA would grow to the same $160,357, but at 22% tax on withdrawal, he nets $125,078. The Roth advantage: $35,279. Even though Daniel paid a higher rate now, the 20-year time horizon made conversion worthwhile.

The deeper lesson: time horizon matters more than the rate comparison. Clients in their 50s with 30-year lifespans are strong conversion candidates. Clients in their 80s with short horizons gain less benefit.

The Roth Conversion Window: The Key Timing Insight

Many clients experience unusually low income in their early retirement years. They have left their jobs (income drops) but have not yet claimed Social Security or Required Minimum Distributions (income has not risen back). This temporary low-income period is the Roth conversion window.

Consider a typical timeline. A client earns $150,000 at age 55-62, placing them in the 24% bracket. They retire at 62 and have zero salary. Suddenly they are in the 12% or 22% bracket. They will claim Social Security at 67 (increasing taxable income), and RMDs will begin at 73 (increasing it further). So there is a window, roughly ages 62-72, when income is unusually low.

This window is not infinite. Social Security claiming increases taxable income through provisional income rules. Medicare enrollment at 65 triggers exposure to IRMAA surcharges. But for the years it remains open, it represents an opportunity to convert at rates the client may never see again.

Susan, age 63, retired last year. Her current taxable income is just $25,000 from interest and dividends. She is currently in the 12% bracket and has room to convert up through the 22% bracket. She will claim Social Security at 67. For the next four years, she could convert $75,000 annually, moving $300,000 into Roth over four years while staying in the 12% and 22% brackets. Her traditional IRA balance drops, reducing future RMDs. At age 73, her mandatory distributions are significantly lower than they would have been.

The inverse is also true. A client who is currently in the 32% or 37% bracket and expects to drop to 22% or 24% in retirement should generally wait. Paying 37% now to avoid 22% later destroys value.

Bracket Filling: The Core Strategy

Bracket filling is the most practical conversion strategy. The concept is simple: convert enough each year to fill lower tax brackets without spilling into higher ones.

Step 1: Calculate taxable income from all non-conversion sources (wages, pensions, Social Security, investment income). Step 2: Identify where the client sits in the current bracket and how much room remains. Step 3: Convert an amount equal to the remaining bracket space.

Thomas and Linda are married filing jointly. Thomas is 67 with a $48,000 pension. Linda is 65 with Social Security starting this year at $32,000. They have $15,000 in investment income. Their taxable income before conversion: $48,000 (pension) + $27,200 (85% of Social Security, which is taxable) + $15,000 (investment income) = $90,200.

The 22% federal bracket for married couples extends to an indexed threshold. They have substantial room before reaching the 24% bracket. By converting an amount that uses the remaining bracket space (but does not exceed the top of the 22% bracket), they can move substantial sums to Roth at favorable rates.

Bracket filling captures the arbitrage between current low rates and expected higher future rates. Systematically filling the 22% bracket year after year moves hundreds of thousands of dollars at favorable conversion rates. The alternative—converting nothing—leaves the traditional balance to grow, increasing future RMDs and likely pushing the client into higher brackets when distributions become mandatory.

When Conversions Break Down: Real Limitations

Roth conversions are not universally beneficial. Several situations make conversion clearly disadvantageous.

High current tax rates are the first sign to wait. A client currently in the 35% or 37% bracket who expects to drop to the 22% bracket in retirement should generally delay conversions. Paying 37% now to avoid 22% later destroys value unless the time horizon is extremely long.

Imminent need for funds is another problem. Clients under age 59 1/2 face complications if they may need access within five years. A conversion taxable portion withdrawn within five years triggers a 10% early withdrawal penalty. Converting and then withdrawing defeats the purpose.

High state taxes create another constraint. A client in a high-tax state like California (top marginal rate 13.3%, with effective rates of 9.3% to 12.3% for most retirees) planning to retire in Florida (0% state rate) should wait. Converting in California means paying both federal and state tax that could be avoided entirely by converting after the move.

Clients with substantial pension or Social Security income may never drop to low brackets regardless. If their “floor” income keeps them in the 24% bracket year after year, converting at 24% gains nothing. The rate arbitrage disappears.

And here is a limitation many advisors miss: charitable intent. A client planning to leave retirement assets to a charity at death should not convert. Charities receive traditional IRA assets tax-free. Converting prepays taxes that would never be owed. Charity receives Roth or traditional accounts the same way. Ask about charitable intent before recommending conversion.

Client Conversation: How to Structure the Discussion

When a client asks about Roth conversions, the conversation should follow a clear structure.

First, understand the client’s timeline and aspirations. How many years until they claim Social Security? How many years until RMDs begin at 73? How long does the client expect to live (life expectancy estimate, not age)? Are they interested in leaving wealth to heirs or spending everything? Clients focused on legacy planning often favor conversion. Clients focused on spending in retirement care less.

Second, project their tax situation. What is their current marginal bracket? What do they expect it to be in 10 years, 20 years? This requires looking at pension income, Social Security income, and other sources. It requires honesty about tax law. Current rates are historically low by post-WWII standards. Clients concerned about future increases have a legitimate planning point.

Third, calculate break-even. Using your client’s investment assumptions (what return do they expect?), how long until the Roth advantage exceeds the conversion tax? For a client in their 50s with a 30-year horizon, break-even might come in eight years. For a client in their 70s with a 10-year horizon, break-even might never come.

Fourth, model second-order effects. Specifically, run three scenarios: (1) no conversion, (2) moderate annual conversions, (3) aggressive conversions. For each scenario, calculate projected Medicare premiums at enrollment (using the two-year MAGI lookback). Run Social Security taxation calculations to see how much Social Security becomes taxable at each conversion level. These effects are often substantial and frequently overlooked.

Finally, present the analysis neutrally. Not “you should convert” but “here is what your after-tax wealth looks like with no conversions, here is what it looks like with $50,000 annual conversions, and here is what it looks like with $100,000 annual conversions. Here are the Medicare and Social Security effects at each level.”

The Hidden Cost: Medicare Premiums (IRMAA)

Income-Related Monthly Adjustment Amounts are surcharges added to Medicare Part B and Part D premiums for higher-income beneficiaries. This is where many conversion plans backfire.

Medicare uses Modified Adjusted Gross Income from two years prior. A conversion in 2026 affects premiums in 2028. Robert converted $150,000 in 2024 at age 64. His other income that year was $85,000. Total MAGI: $235,000, placing him in IRMAA Tier 4 ($205,001–$499,999). Two years later, when he enrolled in Medicare at 65, the conversion-triggered IRMAA hit in his second year of coverage at 66 when SSA used his 2024 MAGI. His combined Part B and Part D surcharges totaled roughly $6,355 annually (assuming Part B and Part D enrollment) in additional Medicare premiums.

Robert did not anticipate this when planning his conversion. The extra cost, multiplied over several years of Medicare coverage, reduces his conversion benefit substantially.

Planning around IRMAA requires looking ahead. Complete large conversions before Medicare enrollment (conversions at ages 63-64 affect IRMAA at ages 65-66). Manage conversion amounts carefully near IRMAA thresholds. A conversion that pushes income $1,000 over a threshold triggers the full surcharge for that tier. Stay below thresholds when possible.

Create a multi-year calendar showing when each year’s income affects Medicare premiums. Many clients do not realize the two-year lag. This visual helps clients understand why their conversion plan extends beyond just “filling brackets.”

Key Takeaways

- Roth conversions trade taxes paid today for tax-free growth tomorrow. Whether the trade makes sense depends on comparing current and future tax rates and calculating break-even periods based on investment time horizon.

- The conversion window between early retirement and age 73 (when RMDs begin) offers historically low-income years ideal for conversions. This window closes as Social Security and RMDs begin, making timing critical.

- Bracket filling is the core strategy: convert enough each year to use lower bracket space without spilling into higher brackets. Systematic annual bracket filling converts hundreds of thousands of dollars at favorable rates.

- Always recommend paying conversion taxes from non-retirement funds. Using IRA funds to pay the tax reduces the amount converted and may trigger penalties if the client is under 59 1/2.

- Second-order effects on Medicare premiums (IRMAA) and Social Security taxation often exceed the basic tax benefit. Model these effects before recommending conversions, using a two-year lookback for IRMAA impact.

- Conversions do not make sense for all clients. High current brackets, short time horizons, planned state relocation, high floor income in retirement, and charitable intent are all reasons to wait or avoid conversions.

The Advisor’s Edge

Roth conversions look simple on the surface: move traditional money to Roth, pay some tax, get tax-free growth. Most advisors who discuss them focus on the tax benefit and the bracket space available today.

Your conversation goes deeper. You model scenarios showing what happens without conversions, with moderate annual conversions, and with aggressive conversions. You calculate the two-year MAGI lookback and show your client how conversions affect Medicare premiums at enrollment. You run Social Security taxation calculations to show how much Social Security becomes taxable at each conversion level.

You acknowledge the limits. High current brackets, short time horizons, and charitable intent are all legitimate reasons to avoid conversions. You never push conversions as a one-size-fits-all solution.

This approach requires more work. But it is how you turn a simple tax strategy into a genuine planning conversation. You help clients understand not just the benefit, but the full cost and timing. You position conversions as part of an integrated distribution strategy that spans retirement, Medicare enrollment, and legacy planning.

This integrated perspective is what the Certified Tax Specialist™ (CTS®) credential represents. Tax planning is not about individual transactions in isolation. It is about understanding how every decision ripples across your client’s entire financial picture over decades.

For a closer look at how RMDs interact with conversion planning, see Required Minimum Distributions: Calculate, Plan, and Avoid the Penalty.

Sources and Notes: Content draws on CTS Module 1, Chapter 4 (Retirement Account Taxation) and Module 2, Chapter 9 (Distribution Planning Strategies). IRMAA thresholds and bracket tiers reflect CMS-published figures for 2026. Federal income tax brackets reflect IRS Revenue Procedure 2025-32. SECURE 2.0 RMD age provisions per P.L. 117-328, Section 107. This article is refreshed annually or as tax law changes.