Opening Insight

Most advisors know the RMD rule: you must withdraw each year or face a penalty. Many clients think of RMDs as forced spending and resist them. The gap between these two perspectives contains your opportunity.

RMDs are not personal spending requirements. They are tax events. Your client’s $1.2 million IRA at age 73 forces a $45,000 taxable distribution regardless of whether they need the money. But that same $1.2 million, if partially converted to a Roth when your client was 65 and in a lower tax bracket, would have generated smaller RMDs today and years of tax-free income tomorrow. The planning window closes when the first RMD year arrives. It opens five to ten years earlier, during the gap between retirement and mandatory distributions.

Understanding where your client sits in this timeline, and what moves are still available, separates advisors who react to RMDs from advisors who design around them.

Core Analysis

The Age Trigger Question Has Changed

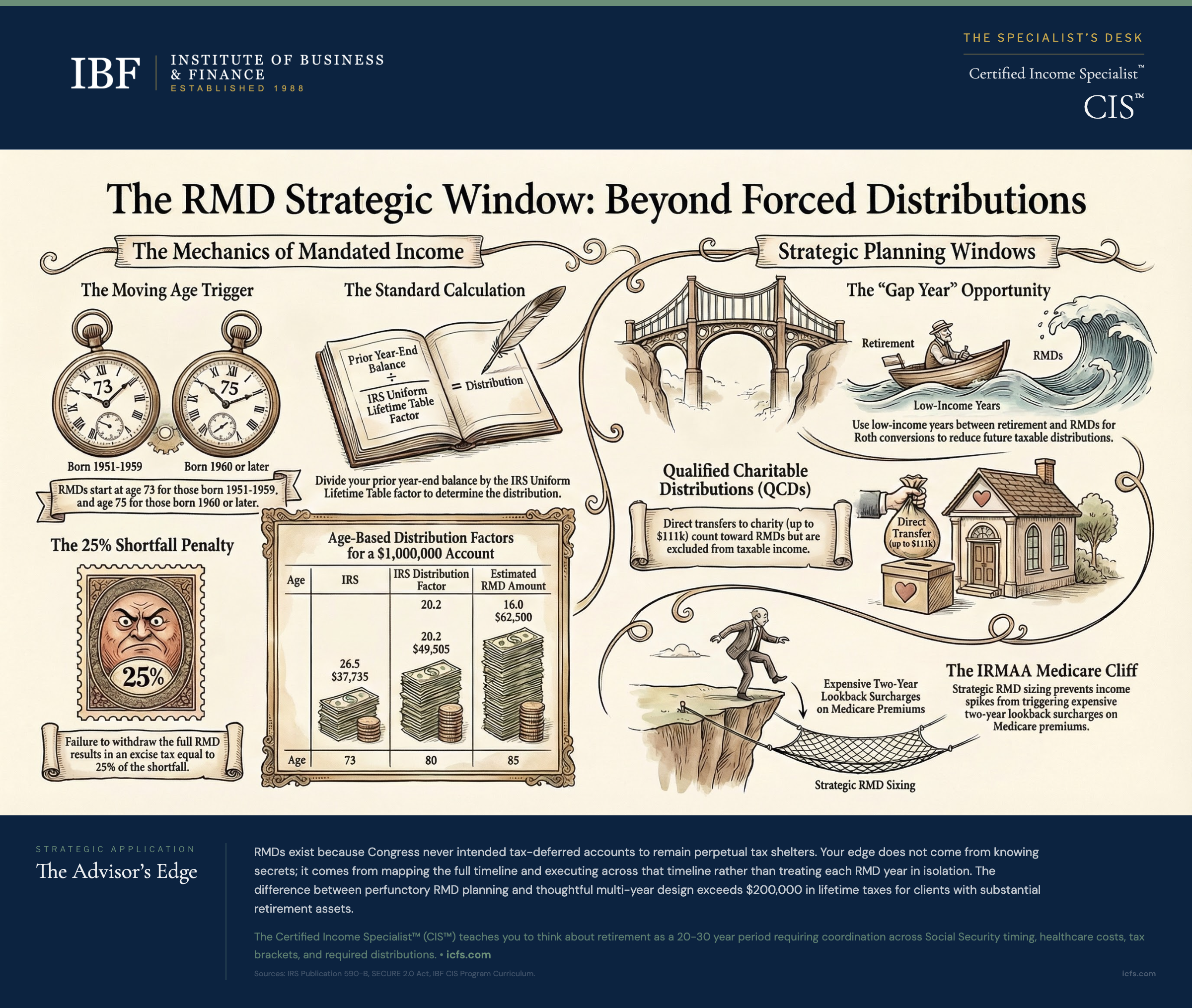

Until recently, RMD age was 72 for most people. That window closed. The SECURE 2.0 law, enacted in December 2022, created a birth-year-based schedule that gradually pushes RMD age higher.

If your client was born before July 1, 1949, they reached RMD age of 70.5 years ago and are already required to distribute. If they were born between July 1, 1949 and December 31, 1950, their RMD age is 72. For those born between January 1, 1951 and December 31, 1959 (a cohort approaching or in RMD age now), the trigger is 73. For anyone born in 1960 or later, RMD age advances to 75, delaying mandatory distributions by two additional years.

This progression matters because later RMD age means more compounding years for tax-deferred growth, but it also means clients have fewer planning windows before distributions begin. A client born in 1952 has already reached 73 or is about to. That five-to-ten-year gap year window between retirement and RMDs has narrowed or closed entirely. The advisor who met this client at age 65 (or 62) had the real planning window; the advisor who first engages at age 72 is managing consequences, not opportunities.

How RMDs Are Calculated

The calculation is straightforward formula: divide the prior year-end account balance by a life expectancy factor from IRS tables.

Victor, age 75, holds a traditional IRA with a December 31 balance of $850,000. The IRS Uniform Lifetime Table lists a distribution period factor of 24.6 for age 75. His RMD is $850,000 divided by 24.6, which equals $34,553. He must withdraw at least that amount this year.

The Uniform Lifetime Table is the default for most account owners. It uses a life expectancy period that increases with age. At 73, the factor is 26.5 (roughly 3.8% of balance). At 80, it’s 20.2 (roughly 5.0%). At 85, it’s 16.0 (roughly 6.3%). The RMD percentage escalates with age even if account balances decline. A client with $1 million at age 73 and $900,000 at age 85 still faces a larger RMD at 85 because the denominator shrinks faster than the balance drops.

Two other IRS tables exist. The Joint and Last Survivor Table applies when the sole beneficiary is a spouse more than ten years younger than the account owner. It provides larger distribution periods (smaller RMDs) because it accounts for the younger spouse’s longer expected lifetime. The Single Life Expectancy Table is for inherited IRA beneficiaries, a different situation.

Aggregation Rules Create Flexibility (Within Limits)

Your client may hold multiple IRAs, a 401(k) from a former employer, a 403(b) from years in education or nonprofit work, and assorted other accounts. RMD calculations treat these differently.

For traditional IRAs: calculate the RMD separately for each account, then aggregate the total. The combined RMD can be taken from any one IRA or combination of IRAs. Victor has three IRAs with individual RMDs of $15,000, $12,000, and $7,553. His total IRA RMD is $34,553, but he can withdraw the entire amount from one IRA if that makes administrative sense.

For 401(k)s, 403(b)s, and other employer plans: each plan requires separate calculation and separate distribution. Unlike IRAs, you cannot satisfy a 401(k) RMD by withdrawing from an IRA. Each plan must distribute its own RMD.

This distinction matters because clients often hold employer plan balances they do not want to disturb. Rolling a 401(k) into an IRA before RMDs begin gives you aggregation flexibility. Rolling after RMDs begin is too late; the 401(k) must distribute its separate RMD for that year.

The First RMD Timing Decision Carries Hidden Consequences

Your client’s first RMD is due by December 31 of the year they reach RMD age. But IRS rules permit one delay: they can defer the first RMD until April 1 of the following year. This creates a trap that catches many advisors and clients.

Barbara, born in March 1952, turned 73 in 2025. Her first RMD is for 2025. She can withdraw by December 31, 2025, or delay until April 1, 2026. If she delays, she must take her 2025 RMD by April 1, 2026, and her 2026 RMD by December 31, 2026. Two RMDs in one calendar year. If each is $35,000, Barbara now has $70,000 in taxable income in 2026 concentrated into twelve months. This pushes her into a higher bracket and triggers Medicare surcharges for 2028 (Medicare uses a two-year lookback on income).

The April 1 delay applies only to the first RMD. All subsequent RMDs must be taken by December 31. There is no permanent delay option. Most advisors recommend taking the first RMD in the year triggered rather than deferring, unless a specific tax reason justifies the spike (such as a one-time deduction that offsets the income).

RMDs and IRMAA: The Medicare Premium Consequence

RMDs are included in Modified Adjusted Gross Income (MAGI), the income measure that determines Medicare Part B and Part D premium surcharges under IRMAA rules. If a client’s 2025 income exceeds certain thresholds, their 2027 Medicare premiums rise. By the time they see the surcharge on their premium bill, the damage is done. The income decisions they made two years earlier created the outcome.

This two-year lookback transforms RMD planning from a tax calculation into a healthcare cost calculation. A $50,000 RMD might cost $12,000 in federal income tax (at 24% rate) but add $2,400 in annual Medicare surcharges if it pushes the client into a higher IRMAA tier. The total impact of that distribution is $14,400, not $12,000.

IRMAA brackets are cliff-based, not gradual. Exceeding a threshold by one dollar triggers the full surcharge for that tier. This creates planning opportunities where small adjustments to income can save thousands. Eleanor, age 67, considering a Roth conversion of $130,000, calculates that this pushes her 2026 income to $220,000, exceeding an IRMAA threshold by $2,000. If crossing the threshold costs $2,400 in annual surcharges, she should instead convert $125,000 and save the full surcharge while converting nearly as much. The $5,000 difference in conversion costs her approximately $1,100 in additional tax (at 22% rate) but saves $2,400 in Medicare premiums, a net benefit of $1,300.

Qualified Charitable Distributions: Superior to Donating RMDs

For charitably inclined clients age 70½ or older, a Qualified Charitable Distribution (QCD) allows direct transfer of IRA funds to a qualified charity. The QCD counts toward the RMD but is excluded from taxable income. The 2026 annual limit is $111,000 per person, indexed for inflation, providing meaningful planning opportunity.

Karen, age 76, wants to donate $25,000 to her church. She has three RMD options.

Option 1 (inefficient): Take her $40,000 RMD, pay tax on $40,000 of income, net $30,400 after tax (at 24% rate), and donate $25,000 to the church. She gets a charitable deduction, but the deduction may not fully offset the tax if she does not itemize or faces deduction limitations. Result: $40,000 of taxable income for $25,000 of charity.

Option 2 (better): Use a QCD. $25,000 flows directly from her IRA to the church. This counts toward her $40,000 RMD. She withdraws the remaining $15,000 RMD in cash. Result: $15,000 of taxable income for $25,000 of charity. The QCD excludes the distribution entirely; no charitable deduction is needed because there is no taxable income to shelter.

Option 2 reduces Karen’s taxable income by $25,000 compared to Option 1, saving approximately $6,000 in federal income tax at the 24% marginal rate, plus potential IRMAA savings if the QCD keeps her below a Medicare income threshold. QCDs are powerful because they reduce MAGI, potentially avoiding IRMAA surcharges. For clients who tithe or have regular giving patterns, setting up annual QCDs equal to their giving amount makes the QCD their default charitable vehicle.

The Roth Conversion Window Before RMDs Begin

Once RMDs begin, each dollar the client is forced to distribute consumes a portion of their tax bracket. If their RMD is $40,000 and they want to convert $50,000 from traditional IRA to Roth, they now have $90,000 of income in one year. The marginal tax rate on conversions rises significantly because the RMD has already filled the lower brackets.

Before RMDs begin, particularly during the gap years between retirement and when Social Security starts, the client’s total income is often at its lifetime minimum. This window is ideal for converting larger amounts to Roth. A client retiring at 64 with a targeted Social Security start at 70 has six years of potential gap years where conversions can occur at lower marginal rates. Each $50,000 converted during those years at a 22% rate avoids future conversion at 24% or higher rates once RMDs start.

The mathematics favor early conversion: convert at 22% now while gap years exist, rather than waiting and converting at 24% or higher later when RMDs fill brackets.

Penalties: 25% of Shortfall (Down from 50%)

Failure to take the full RMD triggers an excise tax. SECURE 2.0 reduced this penalty from 50% to 25% of the shortfall. If Victor’s RMD was $34,553 but he withdrew only $20,000, the $14,553 shortfall incurs a $3,638 penalty (25% of $14,553). On top of this, he still owes income tax on the eventual distribution. The penalty drops further to 10% if the error is corrected within two years.

The 25% penalty is still severe. A $10,000 missed RMD costs $2,500 in penalty plus income tax on the eventual distribution. Prevention through calendar reminders and accountability systems is far more efficient than correction.

Beneficiary RMDs After the Owner Dies

Inheriting a retirement account triggers a new RMD schedule with different rules than the original owner’s.

Surviving spouses have the most flexibility. They can:

- Roll the inherited IRA into their own IRA and follow their own RMD schedule

- Stay on the inherited account as beneficiary

- Take a lump-sum distribution

Younger surviving spouses usually win with the rollover. It pushes the RMD start back to their own age 73 or 75.

Non-spouse beneficiaries generally have to empty the account within 10 years.

Five categories of beneficiary, called eligible designated beneficiaries (EDBs), get out of the 10-year rule and can stretch distributions over their own life expectancy:

- Surviving spouse

- Minor child of the owner (only until majority age; then the 10-year clock starts)

- Disabled individual

- Chronically ill individual

- Beneficiary not more than 10 years younger than the owner

Timing matters. If the original owner died after their Required Beginning Date, non-EDB beneficiaries take annual distributions each year of the 10-year window AND empty the account by year 10. If the owner died before their RBD, no annual distributions are required, just account depletion by year 10.

Limitation: When RMD Planning Gets Complicated

RMD planning assumes the client is a U.S. citizen with straightforward account structures. Reality introduces friction.

Non-U.S. residents face different tax treatment. Multiple employer plans create aggregation headaches. Clients with both IRA and 401(k) assets must remember that 401(k) RMDs do not aggregate with IRA RMDs.

The still-working exception (where employees still working at age 73 can defer RMDs from their current employer’s 401(k) but not from IRAs or from other former employers’ plans) confuses many clients. An employee still working at 75 can defer the 401(k) RMD from their current employer while satisfying a separate IRA RMD simultaneously.

QCDs work only from IRAs, not from employer plans. A client with substantial 401(k) assets who wants to use the QCD strategy must first roll the 401(k) to an IRA.

The regulatory landscape for those born in 1959 has been substantially clarified: IRS proposed regulations issued in July 2024 confirm that age 73 is the applicable RMD age for this cohort, resolving a drafting ambiguity in SECURE 2.0. Final regulations had not yet been formally issued as of early 2026, but the proposed regulations provide clear guidance and advisors should plan around age 73 while confirming regulatory status for their specific client situations.

Client Conversation

When a client first reaches within one to three years of RMD age, this conversation should occur:

“Your RMDs begin at age [73 or 75], which is [timeline] away. This is not optional, and the penalty for missing one is steep. Here’s what that means: each year starting then, we’ll calculate a minimum withdrawal from your traditional IRA based on your age and account balance. That withdrawal is taxable income.

The good news is that we have time now to shape the future. If your current income is lower than it will be once RMDs start (because Social Security is not yet flowing, or your pension has not begun), we can move money from your traditional IRA into a Roth IRA now while your tax rate is lower. You pay tax today, but those converted dollars grow tax-free forever and do not count as RMD.

This is a one-time opportunity. Once your first RMD year arrives, those gap years are gone. The question is not whether you’ll have RMDs, but how large they will be. Conversions now make them smaller later.

Let’s model a few scenarios: (1) do nothing, let the IRA grow, and take RMDs as they come; (2) convert $[amount] per year during the gap years at our current [22%] tax rate; (3) convert more aggressively if you can stomach the income spike and want to minimize Medicare surcharges. Each scenario shows your total taxes, your RMD amounts, and your account balances at key milestones. Which path aligns with your goals?”

This frames RMDs not as individual annual events but as part of a multi-year strategy. It acknowledges that planning windows exist, that time is finite, and that choices made now shape outcomes for decades.

Key Takeaways

- RMD age varies by birth year: Age 73 for most current retirees (born 1951-1959), age 75 for those born 1960 or later. Confirm your client’s specific age trigger and document it in your planning notes.

- Calculate using prior-year balance divided by Uniform Lifetime Table factor: Victor, age 75 with $850,000, faces a $34,553 RMD ($850,000 ÷ 24.6). This percentage escalates with age even if balances decline.

- Aggregate IRA RMDs but not 401(k) RMDs: You can take your total IRA RMD from any combination of IRAs, but each employer plan RMD must be taken separately. Roll 401(k)s to IRAs before RMDs begin to gain flexibility.

- First RMD delay creates a two-RMD spike: Deferring your first RMD until April 1 of the next year forces two RMDs in one calendar year, triggering higher tax brackets and IRMAA surcharges. Generally avoid the delay; take the first RMD in the year triggered.

- Use gap years for Roth conversions: The period between retirement and RMD start (age 65-73 for many clients) is the lowest-income period in retirement. Conversions here happen at lower tax rates than conversions after RMDs begin. Model the math; convert strategically.

- IRMAA cliffs matter more than bracket rates: A $50,000 RMD might cost $12,000 in federal tax but add $2,400 in Medicare surcharges if it triggers an IRMAA threshold. Know the thresholds; size income to avoid them where possible.

- Qualified Charitable Distributions beat standard RMD-then-donate: For charitably inclined clients, QCDs exclude distributions from income entirely while satisfying RMD, saving tax compared to taking the RMD and then donating the proceeds.

The Advisor’s Edge

RMDs exist because Congress never intended tax-deferred accounts to remain perpetual tax shelters. The rules are public, standardized, and entirely knowable. Your edge does not come from knowing secrets; it comes from mapping the full timeline and executing across that timeline rather than treating each RMD year in isolation.

The difference between perfunctory RMD planning and thoughtful multi-year design exceeds $200,000 in lifetime taxes for clients with substantial retirement assets. This value accrues from two practices: first, using gap years for Roth conversions before RMDs begin, and second, coordinating distribution sizing with IRMAA thresholds so income spikes do not trigger elevated Medicare surcharges that follow income spikes with a two-year delay.

The Certified Income Specialist™ curriculum teaches you to think about retirement not as a year, but as a 20-30 year period requiring coordination across Social Security timing, healthcare costs, tax brackets, and required distributions. RMD planning is one instrument in this orchestration. Mastering the rules is table stakes. Coordinating them with Roth conversions, Social Security claiming, and pension timing is where you deliver client value that most advisors miss.

These are the skills that transform Monday morning conversations from “Here’s your required withdrawal” into “Here’s the strategy that minimizes your lifetime taxes while securing your income.” That is the Certified Income Specialist™ difference.

For deeper exploration of distribution sequencing, IRMAA planning, and multi-year tax strategy, see the Sequence of Returns Risk.

Sources and Notes: IRS Publication 590-B (Distributions from Individual Retirement Arrangements), Uniform Lifetime Table, IRMAA threshold schedules, and CIS curriculum materials on retirement income distribution and tax planning. This article is refreshed annually.

2026-05-21 22:19:21 UTC[+0000] [notice] Command: icfs.live -- drush ev $node = \Drupal::entityTypeManager()->getStorage('node')->load(1128); echo $node->get('field_body')->value; [Exit: 0] (Attempt 1/1)