The Control Premium

Most clients are employees. Their income is set by an employer, their withholding is automated, and their tax planning options fit on a single page. Business owners are different. They control timing of income recognition. They choose the entity structure. They determine when and how to exit. That control creates tax planning opportunities that can be worth more than years of operating profits. But only if the advisor understands the options.

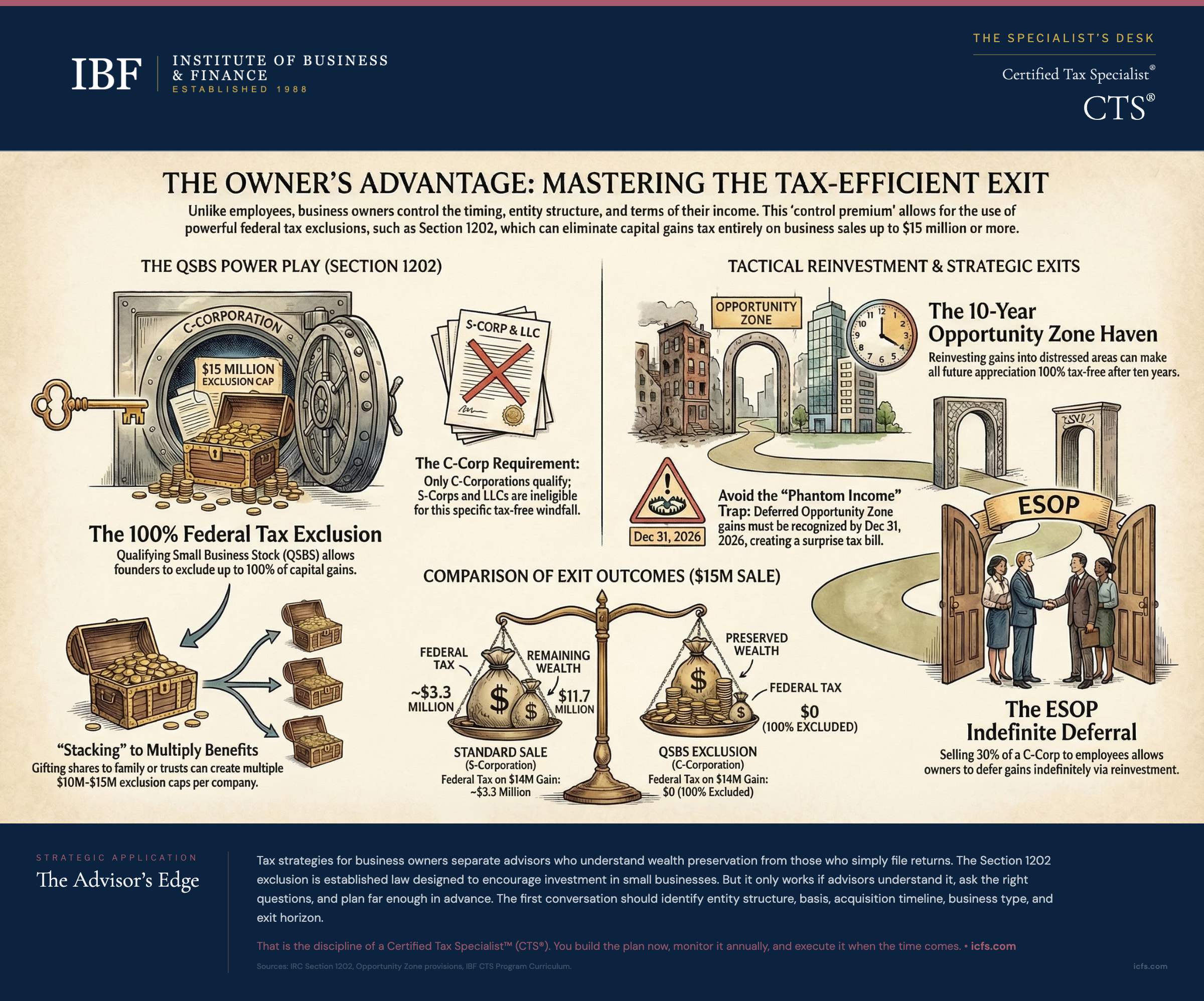

A tech founder selling a company for $15 million with a $1 million cost basis faces different outcomes based on entity choice. If structured as an S corporation, the $14 million gain triggers $3.3 million in federal tax at the 23.8% combined rate. If structured as a C corporation with QSBS-qualifying stock and stacking strategies, the entire gain might be excluded. That difference determines whether the owner keeps the full proceeds or surrenders one-third to taxes.

This article covers three core strategies: Section 1202 QSBS exclusions, Opportunity Zone investments for gains reinvestment, and multi-strategy exits combining installment sales, ESOPs, and charitable timing.

Section 1202: The QSBS Opportunity

The most powerful capital gains exclusion in the tax code is Section 1202. It allows shareholders of Qualified Small Business Stock to exclude up to 100% of their gain from federal income tax upon sale. Congress enacted it in 1993 to encourage investment in small businesses. It has evolved significantly, particularly through the One Big Beautiful Bill Act signed July 4, 2025.

What Makes Stock Qualify

QSBS eligibility requires both corporate and stock requirements to be met simultaneously.

The corporation must be a C corporation at issuance. S corporations, LLCs, and partnerships cannot issue qualifying stock. This is the first surprise for many advisors who work with S corp owners: if the business was never structured as a C corporation, QSBS planning is not available regardless of the size of eventual gain.

The corporation must meet a gross asset test at the time the stock is issued. For pre-OBBBA stock (issued before July 5, 2025), the $50 million limit applied at any time before and immediately after issuance. For post-OBBBA stock (issued after July 4, 2025), OBBBA increased the limit to $75 million (indexed for inflation), measured at issuance only. Gross assets are measured immediately after the stock issuance and include the cash from the stock itself. A company that raises $60 million in venture capital five years after founding could have stock issued at different times with different QSBS eligibility. Shares issued when the company was small qualify. Shares issued after the company exceeded the threshold do not.

The corporation must be engaged in a qualified trade or business. This disqualifies professional services (health, law, engineering, accounting, actuarial science, consulting, performing arts, athletics), financial services, brokerage services, farming, natural resource extraction, and hospitality. Also disqualified: any trade or business where the principal asset is the reputation or skill of one or more of its employees. A software company qualifies. A consulting firm built around personal expertise does not.

At least 80% of the corporation’s assets must be used in the active conduct of the qualified business. This means the corporation cannot be sitting on large cash positions or investments unrelated to the core business.

The stock must be acquired at original issuance in exchange for money, property, or services. A client who buys stock from another shareholder does not qualify, even if the company is small and QSBS-eligible. The stock must come directly from the corporation to the shareholder.

Exclusion Amounts: The OBBBA Restructure

The OBBBA introduced a significant change. Before July 2025, QSBS required a full five-year holding period. If you held it four years and eleven months, you got zero exclusion. OBBBA moved to graduated tiers.

For stock acquired after July 4, 2025, the exclusion percentage depends on holding period: 50% exclusion for holding between 3–4 years, 75% exclusion for 4–5 years, and 100% exclusion for 5 years or more. For stock acquired on or before July 4, 2025, exclusion depends on the original acquisition date: stock issued August 11, 1993 to February 17, 2009 receives 50% exclusion after 5 years; stock issued February 18, 2009 to September 27, 2010 receives 75% exclusion after 5 years; stock issued September 28, 2010 to July 4, 2025 receives 100% exclusion after 5 years. You cannot restart the clock on pre-OBBBA stock to access the shorter windows.

The exclusion is capped per shareholder, per company. The cap is the greater of a fixed dollar amount or 10 times the shareholder’s adjusted basis. For pre-OBBBA stock, the fixed cap is $10 million. OBBBA increased it to $15 million (indexed) for stock issued after July 4, 2025. For a founder who contributed $100,000 and sells for $12 million, the per-issuer cap determines how much gain is excludable. Gain above the cap is taxable.

Multiplying the Benefit Through Stacking

The per-issuer cap applies per shareholder. A founder expecting gains to exceed the cap can gift shares to family members before sale. Each recipient becomes a separate taxpayer with their own exclusion cap. A founder could also establish multiple irrevocable trusts, gift shares to each, and multiply the cap.

Consider David Patterson, who founded a software company. If David sells alone and his gain exceeds the per-issuer cap, significant gain is taxable. If David gifts shares to his spouse, adult children, and multiple irrevocable trusts before sale, each recipient has their own cap. By distributing the ownership, David can exclude substantially more gain in aggregate.

This requires advance planning. Shares must be gifted before the sale is imminent, and each recipient must hold through to the sale. The IRS has recognized that non-grantor irrevocable trusts are separate taxpayers with separate caps. Grantor trusts do not provide separate caps.

The Entity Choice Question

QSBS is available only for C corporation stock. For companies expecting substantial exits, this often makes C corporation status more attractive despite the theoretical disadvantage of double taxation. The 21% flat corporate rate established by the Tax Cuts and Jobs Act and preserved by OBBBA has made the C corporation option more competitive.

The decision framework turns on exit timing and gain size. For a business expecting a small exit in the near term, the QBI deduction available to S corporation shareholders is valuable. For a business expecting a substantial exit, the QSBS exclusion available only to C corporation shareholders is often more valuable. For a business with no specific exit plan, S corporation status provides more flexibility because the option to convert to C corporation status exists, though it restarts the QSBS holding period clock.

Opportunity Zone Investments

Opportunity Zones provide a different planning tool. Rather than excluding a specific type of stock, they offer tax benefits for investing capital gains in designated economically distressed areas. The program was created by the Tax Cuts and Jobs Act of 2017 and made permanent by OBBBA.

The mechanism is deferral and exclusion. An investor with a capital gain can invest that gain in a Qualified Opportunity Fund (QOF). The gain is deferred until the earlier of the date the QOF investment is sold or December 31, 2026 (for pre-2027 investments). If the QOF investment is held for 10 years or more, any appreciation in the QOF investment itself is excluded from income.

How It Works

Sarah realizes a $300,000 capital gain in 2018. Within 180 days, she invests it in a QOF developing apartment buildings in an Opportunity Zone. Her gain is deferred until 2026. If she holds the investment for 10 years, the $300,000 post-investment appreciation is excluded entirely.

The QOF self-certifies with the IRS by filing Form 8996. It must hold at least 90% of assets in Qualified Opportunity Zone Property (zone business stock, partnership interests, or tangible property). If acquiring existing property, the QOF must substantially improve it within 30 months (additions to basis exceeding the original building basis).

The 2026 Deadline Trap

For investments made under the original TCJA rules (before January 1, 2027), the deferral period ends December 31, 2026 regardless of when the investment was made. If you invested in a QOF in January 2025, your deferred gain must be recognized by December 31, 2026. You will owe tax on the deferred gain even if your QOF investment is completely illiquid and you have not sold it. The tax is due April 15, 2027.

This creates a “phantom income” situation. Many OZ investors face a surprise tax bill on gains they thought were deferred indefinitely. By the time the 2026 deadline arrives, OZ investments may still be years away from liquidity.

For investors today, the primary benefit of OZ investments is the 10-year exclusion on appreciation, not the deferral. Run the numbers for your client: even without substantial deferral, excluding all appreciation after the investment date can be significant if the client has a 10-year time horizon and real economic substance in the OZ investment.

OBBBA Changes and Post-2026 Rules

OBBBA restructured the program for investments after December 31, 2026. The fixed December 31, 2026 recognition date has been replaced with a rolling deferral structure (5 years for each investment, with a 10% basis step-up at 5 years; the 7-year 15% step-up was eliminated). The 10-year exclusion on appreciation remains available. Qualified Rural Opportunity Funds (QROFs) were created to encourage investment in rural zones, with enhanced benefits including higher basis step-ups. The exact implementation details are still being clarified through Treasury guidance.

The key point for advisors today: for pre-2027 investments, focus on the 10-year appreciation exclusion. For post-2026 investments, wait for clarity on the new rules before committing clients.

Entity Structure and Compensation Planning

For S corporation owners, reasonable compensation is often the largest tax planning issue. S corporations offer pass-through taxation, which allows the owner to take profits out of the corporation without the 21% corporate tax. But the owner must pay themselves “reasonable compensation” for services rendered. Compensation is subject to FICA (combined 15.3% up to the Social Security wage base, then 2.9% Medicare above that, plus an additional 0.9% employee-paid Medicare tax on wages above certain thresholds). Distributions are not subject to employment taxes. This creates an incentive to minimize wages and maximize distributions.

The IRS challenges this constantly. Courts have considered comparable company data, industry surveys, complexity of work, and owner qualifications. In the landmark David E. Watson, P.C. v. United States case (668 F.3d 1008, 8th Cir. 2012), the court determined reasonable compensation was $91,044 based on billing rate data from the firm adjusted for owner premiums. Most practitioners defend 50–60% of net profits for professional service businesses. The better approach: analyze comparable data, document methodology, and review compensation annually.

The Retirement Plan Multiplier

S corp owners can shelter substantial compensation through retirement plans: employee deferrals (2026: $24,500 basic), catch-up contributions for ages 50+ (standard: $8,000; ages 60–63 under SECURE 2.0 super catch-up: $11,250), employer profit-sharing (up to 25% of compensation), and cash balance plans for accelerated savings. For high-income owners over age 50, adding a cash balance plan to a 401(k) shelters hundreds of thousands annually. A 55-year-old earning $300,000 can contribute over $200,000 per year. Cash balance plans require actuarial administration and work best for stable, profitable businesses committing to maintain the plan for several years, not volatile businesses or owners planning near-term exits.

Exit Planning: The Multi-Strategy Approach

Business exits represent the largest financial event most owners will experience. Tax planning should begin years before the anticipated sale, not months.

When QSBS Becomes Dominant

Consider Jennifer, age 52, who owns an S corporation software company currently valued at $8 million with a basis of $200,000. She wants to exit in five years. An outright S corporation sale would result in a fully taxable gain. But Jennifer can convert to a C corporation, implement QSBS stacking through gifts to family trusts, and achieve a 75% exclusion after four years (or 100% after five years). By starting five years early, Jennifer transforms a fully taxable transaction into a potentially tax-free one.

Installment Sales and Spread Recognition

An installment sale spreads gain recognition over the payment period, keeping the owner in lower tax brackets and providing cash flow benefits. A business sold for $2 million with a $500,000 basis creates $1.5 million of gain. If paid at closing, all $1.5 million is recognized in year one. If structured as $400,000 at closing plus $400,000 annually for four years, the owner recognizes $300,000 of gain annually (75% of each payment). At the 23.8% combined rate, this creates $71,400 in annual tax instead of $357,000 in year one.

The gross profit ratio (gain divided by contract price) determines the taxable portion of each payment. Depreciation recapture is recognized in year of sale regardless of payment timing, which is important for equipment-heavy businesses.

ESOPs and the 1042 Rollover

For C corporation owners, an ESOP (Employee Stock Ownership Plan) sale offers Section 1042 rollover benefits. If the owner sells at least 30% of the company to an ESOP and reinvests the proceeds in Qualified Replacement Property (stocks and bonds of domestic operating corporations) within 15 months (beginning 3 months before the sale and ending 12 months after), gain recognition is deferred indefinitely. The gain disappears entirely at death through stepped-up basis.

Eleanor owns a manufacturing company valued at $10 million with a basis of $200,000. She sells 100% to an ESOP and reinvests in a diversified stock portfolio within 12 months. Her $9.8 million gain is deferred. If she holds the replacement property until death, the deferred gain never gets taxed; her beneficiaries receive stepped-up basis.

The ESOP structure also provides employee benefits and can improve company productivity. Research from the National Center for Employee Ownership indicates ESOP companies show higher productivity and lower employee turnover than comparable non-ESOP companies.

Real Estate and 1031 Exchanges

Section 1031 like-kind exchanges defer gain on real property exchanges (personal property no longer qualifies). Real property in the US is generally like-kind to any other real property. Replacement property must be identified within 45 days and the exchange completed within 180 days. If replacement property is worth more, the difference is taxable boot.

Coordinating Multiple Strategies

The most tax-efficient exits combine strategies: installment sales for gains exceeding the QSBS cap, Opportunity Zone investments for additional deferral, and charitable donations of appreciated shares. This requires years of planning. QSBS holding periods cannot be accelerated, entity conversions require new compliance, and trust establishment takes time. By the time a sale is imminent, most opportunities have closed.

Where These Strategies Break Down

Each strategy has clear limits. QSBS exclusions require C corporation status and five-year holding periods. Opportunity Zone investments demand 10-year holds or face forced gain recognition in 2026. S corporation reasonable compensation is fact-dependent; underpayment invites audit. ESOPs require C corporation status and at least 30% employee ownership. Installment sales expose the seller to default risk.

A Conversation in Practice

Marcus owns a commercial real estate development company (C corporation) with a current value of $12 million and a basis of $1.5 million. He is 48 years old and thinking about an exit in seven years, around age 55.

The advisor asks: “When did you establish this company, and how much did you contribute in founder equity?”

Marcus: “I started it in 2015 with $100,000 of my own money.”

The advisor follows: “Did you take any additional capital contributions or issue any new shares after that?”

Marcus: “No, it’s been just me as the sole shareholder. But I’ve reinvested all profits back into the business.”

Marcus’s stock likely qualifies for Section 1202 QSBS treatment. He’s held it over 12 years (well past the five-year threshold), his $100,000 contribution established the gross asset test at issuance, and active real estate development qualifies. The advisor asks about asset composition.

Marcus: “About 70% is development projects I sell within 1–2 years, and 30% is long-term rental properties.”

The 80% test requires assets be used in the active conduct of the qualified business. Development assets clearly count, but IRC Section 1202(e)(7) explicitly disqualifies real estate rental activities: “the ownership of, dealing in, or renting of real property shall not be treated as the active conduct of a qualified trade or business.” Marcus’s 30% allocation to long-term rental properties exceeds the 10% passive real property limit and is likely a disqualifier. The advisor should flag this with a tax specialist immediately as a probable Section 1202(e)(7) issue. The 70% development-for-resale component may qualify separately, but the rental portfolio requires specialist review before proceeding with any QSBS planning.

The advisor proposes: “Seven years from now, you’ll have held the stock for 12+ years, so you’ll get 100% QSBS exclusion. But given the size of the gain (about $10.5 million) and the per-issuer cap at $15 million, most of that is protected. If your gain were larger, or if you wanted additional protection, we could explore gifting some shares to trusts now to set up QSBS stacking.”

Marcus: “I’m not planning to give away control during my ownership. What if the company is worth more than $15 million in seven years?”

The advisor responds: “If the company appreciates significantly, you could have gains exceeding the per-issuer cap. At that point, you might consider a partial exit seven years from now, or an installment sale that allows you to keep the appreciation above the cap under QSBS stacking strategies if structured with family members. Or you could look at an ESOP sale if you want to transition ownership to employees.”

This conversation does not lock Marcus into a strategy. It identifies the options, the time horizons required, and the decisions he needs to make. The advisor follows up annually to track company value and adjust the plan as circumstances change.

Key Takeaways

- Section 1202 QSBS exclusions can eliminate federal tax on capital gains for C corporation founders. Stacking strategies multiply the benefit across family members and trusts.

- QSBS requires C corporation status and a five-year holding period (or 3–5 years for partial exclusions under OBBBA). S corporation owners cannot access QSBS.

- Opportunity Zone investments defer gains and exclude appreciation held 10+ years. For pre-2027 investments, recognition is required by December 31, 2026.

- S corporation reasonable compensation must be documented and defensible. Courts examine comparable company data, not formulas.

- Cash balance plans enable high-income owners to shelter hundreds of thousands annually but require actuarial administration and multi-year commitment.

- Installment sales spread gain recognition over time. Depreciation recapture is recognized in year of sale.

- ESOPs allow C corporation owners to defer gain indefinitely by reinvesting in Qualified Replacement Property. Gain is permanently excluded at death through stepped-up basis.

- Exit planning requires years. QSBS holding periods, trust establishment, entity conversions, and ESOP implementation all require advance work.

The Advisor’s Edge

Tax strategies for business owners separate advisors who understand wealth preservation from those who simply file returns. The Section 1202 exclusion is not a loophole or a secret tax trick. It is established law designed to encourage investment in small businesses. But it only works if advisors understand it, ask the right questions, and plan far enough in advance.

The first conversation with a business-owner client should identify the entity structure, the founder’s basis and acquisition timeline, the business type, and the anticipated exit horizon. From there, the path becomes clear. A software founder in a C corporation gets a different plan than a consultant in an S corporation. A real estate investor gets different options than a manufacturing owner. The tools are available. What determines whether they are used is whether the advisor recognizes the opportunity and starts the planning conversation years before the sale.

That is the discipline of a Certified Tax Specialist™ (CTS®). You do not wait until the exit is imminent. You build the plan now, monitor it annually, and execute it when the time comes.

For a practical guide to managing gains on the investment side, see Tax-Loss Harvesting: A Practical Guide for Financial Advisors.

Sources and Notes: Content draws on CTS Module 2, Chapter 8 (Business Owner Tax Planning) and Module 1, Chapter 7 (Entity Selection and Taxation). IRC Section 1202 QSBS exclusion rules reflect OBBBA amendments (P.L. 119-7, signed July 4, 2025). Opportunity Zone provisions per IRC Section 1400Z-2. ESOP tax deferral per IRC Section 1042. David E. Watson, P.C. v. United States, 668 F.3d 1008 (8th Cir. 2012). This article reflects tax law as of March 2026 and is refreshed annually or as legislation changes.