Why Retirement Plans Are the Most Dangerous Asset in Divorce

Retirement accounts are often the largest single asset in a divorce, second only to the marital home and sometimes exceeding it. They are also the most dangerous to divide incorrectly. A mistake with a bank account costs your client some money. A mistake with a retirement plan can cost your client tens of thousands of dollars in unnecessary taxes, lost survivor benefits, or years of delay while a rejected order works its way through the court system again.

The danger comes from complexity. Every plan type has its own division rules, its own administrator, and its own court order requirements. A 401(k) divides differently than a defined benefit pension. A 403(b) has restrictions a 401(k) does not. Governmental 457(b) plans follow different rules entirely. Military retirement operates under its own federal statute. And IRAs, which many advisors assume work like other retirement accounts, do not require a QDRO at all.

This complexity means that the payoff for getting it right is enormous. A well-drafted QDRO takes weeks, not years. The alternate payee gains clear control over her share and can plan accordingly. The participant spouse achieves a clean break from the other’s retirement benefits. When division is structured correctly, retirement assets become the cleanest part of a settlement to execute.

What Makes a QDRO “Qualified”

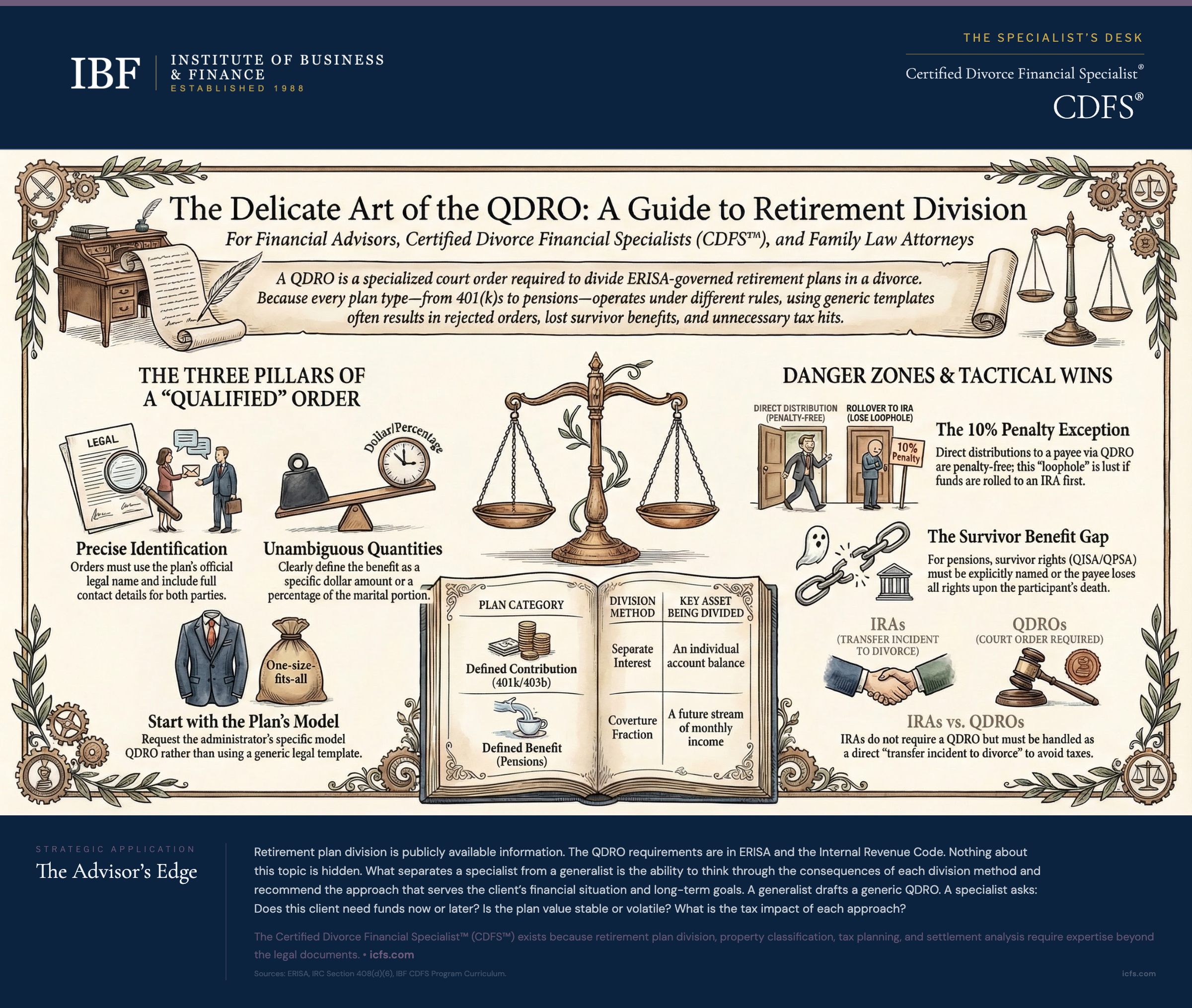

A Qualified Domestic Relations Order (QDRO) is a court order that directs a retirement plan administrator to pay a portion of a participant’s benefits to an alternate payee, typically the non-employee spouse. The word “qualified” is not decorative. It means the order meets specific requirements under the Employee Retirement Income Security Act of 1974 (ERISA) and the Internal Revenue Code. If the order does not meet those requirements, the plan administrator will reject it, and the alternate payee receives nothing until a qualifying order is submitted.

ERISA Requirements for Qualified Status

ERISA governs most private-sector employer-sponsored retirement plans. For a domestic relations order to be “qualified” under ERISA, it must include four required elements and satisfy several negative constraints.

The four required elements are:

1. Full identification of participant and alternate payee. Names and last known mailing addresses at minimum. Social Security numbers are not required by statute but are strongly recommended for plan processing.

2. Specific plan identification. Not “retirement plan” or “the 401(k).” The official name of each retirement plan covered by the order, as it appears in the plan document.

3. Amount or percentage of the benefit. A dollar amount or a percentage, specified clearly as to whether it applies to the total balance or marital portion only. Ambiguous formulas are a leading cause of rejection.

4. Number of payments or time period. When payments begin, how long they continue, and how frequently. Open-ended language without a defined endpoint causes rejections.

In addition to these four elements, a QDRO cannot require a plan to provide a type of benefit, a form of benefit, or an amount of benefit that the plan does not otherwise offer. This is the most important constraint. If the plan does not allow lump-sum distributions, the QDRO cannot order one. If the plan only pays monthly annuities, the QDRO must use that form. The order conforms to the plan, not the other way around.

The Single Biggest QDRO Mistake: Generic Templates

The number one reason QDROs are rejected on first submission is that the order does not match the specific language and provisions required by the plan document. Every rejected QDRO means more attorney fees, more delay, and more risk that the participant spouse changes jobs, takes a distribution, or dies before the order is corrected.

The solution is simple but often overlooked: Before any QDRO is drafted, request the plan’s Summary Plan Description (SPD) and the plan’s specific QDRO procedures. Most large employers have a model QDRO that their plan administrator will accept. Starting from the plan’s model rather than a generic template eliminates the most common rejection reasons.

Plan-Type Division Rules: Each Has Its Own Playbook

The number-one error in retirement plan division is treating all plans the same. A 401(k) divides differently than a defined benefit pension. A 403(b) has restrictions a 401(k) does not. Governmental 457(b) plans follow different rules entirely. Getting the wrong playbook is worse than having no playbook at all.

401(k) Plans: Separate Interest or Shared Payment

A 401(k) is a defined contribution plan, meaning the participant has an individual account with a specific balance. Division is relatively simple because there is a specific dollar amount to divide. The QDRO directs the plan administrator to transfer a portion of the account to the alternate payee.

Two primary approaches exist:

Separate Interest. The alternate payee’s share is segregated into a separate account within the plan; the alternate payee may then elect to roll it to an IRA or take a distribution. The alternate payee controls investment decisions and timing of distributions independently. This approach is best when the alternate payee wants control, does not need immediate income, and plans to manage the funds long-term. The investment risk transfers entirely to the alternate payee.

Shared Payment. The alternate payee receives a percentage of each distribution the participant takes. No separate account is created. This approach works when the participant is already retired and receiving distributions, or when the alternate payee wants to mirror the participant’s decisions. The risk is that the alternate payee depends on the participant’s distribution choices and timing.

For most divorces, separate interest is the better choice. It provides a clean break and puts the alternate payee in control.

Defined Benefit Pensions: Dividing a Future Income Stream

A defined benefit (DB) pension does not have an individual account balance. Instead, it promises a monthly payment at retirement based on a formula, typically combining years of service, final average salary, and a multiplier. Dividing a DB pension is fundamentally different from dividing a 401(k) because you are dividing a future income stream, not a current account balance.

Two primary approaches exist for DB pension division:

Deferred Distribution. The participant spouse remains the plan member and receives his full pension benefit. The alternate payee receives a share of his monthly pension payments when he retires, calculated using the coverture fraction. Example: If the marriage lasted 12 years and the participant participated in the plan for 15 years, the coverture fraction is 12/15 = 80%. If the marital portion is 80% and the court awards the alternate payee 50% of the marital portion, she receives 40% of the pension payment.

The advantage of deferred distribution is simplicity. The plan does not need to valuate the pension. The disadvantage is that the alternate payee is dependent on the participant: she does not receive payments until he retires, and if he dies before the QDRO includes survivor benefit protections, she may lose the benefit entirely.

Present Value Offset. An actuary calculates the present value of the marital portion of the pension. The alternate payee receives other assets (or a payment) equal to her share of that present value. The pension-holding spouse keeps his full pension and owes her nothing when he retires.

The advantage of present value offset is a clean break. Both parties know the value of their settlements at divorce and owe each other nothing in the future. The disadvantage is the cost and complexity of the actuarial valuation, and the risk that the discount rate used in the calculation proves inaccurate over time.

403(b) Plans: Annuity Contract Complications

403(b) plans are used by public educational institutions (public schools, colleges, universities) and nonprofits. They function like 401(k) plans in most respects but often involve annuity contracts. This matters for division because an annuity contract may impose surrender charges if the funds are transferred or withdrawn before a specified date. Note that governmental 403(b) plans for public school employees are generally not subject to ERISA, which may affect the order format required to divide them.

The QDRO for a 403(b) must identify the specific annuity contract (if applicable) and address how surrender charges are allocated between the parties. Some advisors overlook this, and the alternate payee receives funds net of surrender charges she did not anticipate.

If the 403(b) is held in a mutual fund subaccount rather than an annuity, the division is similar to a 401(k).

Governmental 457(b) Plans: No Age-55 Exception

Governmental 457(b) plans are offered by state and local governments. They function like 401(k) plans for division purposes but have an important distinction: there is no 10% early withdrawal penalty for distributions before age 59-1/2. This is true for both the participant and the alternate payee. The trade-off is that 457(b) distributions are also not eligible for the age-55 exception (discussed below).

If your client is the alternate payee on a 457(b) and needs funds before 59-1/2, the lack of penalty is a benefit. If your client is the participant and the alternate payee is receiving distributions, neither of you loses anything to early withdrawal penalties.

Military Retirement: The 10/10 Rule and DFAS

Military retirement benefits are governed by the Uniformed Services Former Spouses’ Protection Act (USFSPA), not ERISA. The benefits are administered by the Defense Finance and Accounting Service (DFAS).

A former spouse can receive direct payments from DFAS only if (1) the marriage lasted at least 10 years, and (2) at least 10 of those years overlapped with the service member’s creditable military service (the “10/10 rule”). If the marriage was only 8 years long and 8 of those years involved military service, the former spouse still has a legal right to a share, but DFAS will not make direct payments. The service member must pay the former spouse directly.

If the 10/10 rule is met, the division works this way: the former spouse receives a percentage of the service member’s monthly retirement pay, calculated either as a fixed percentage or using the coverture fraction. The DFAS order is not called a QDRO, but it serves the same function.

The Coverture Fraction: The Default Calculation

The coverture fraction is the default method for determining the marital share of a retirement plan. It assumes that contributions and growth were roughly uniform across the entire participation period.

Here is how it works: If a participant was in a plan for 15 years and married for 12 of those years, the coverture fraction is 12/15 = 80%. The marital portion of the plan is 80% of the balance on the divorce date. The non-marital (separate property) portion is 20%.

Example: Kevin participated in his 401(k) for 15 years (180 months). He was married to Laura for 12 years (144 months). The account balance at divorce is $285,000.

Coverture Fraction = 144/180 = 0.80 Marital Portion = $285,000 x 0.80 = $228,000

If the court awards Laura 50% of the marital portion, she receives $228,000 x 0.50 = $114,000.

When the Coverture Fraction Is Imprecise

The coverture fraction is a reasonable default, but it is not always accurate. If Kevin’s salary and contributions were significantly lower in his first three years (before marriage) than in his later years, the coverture fraction may overstate the marital portion. Conversely, if Kevin’s salary plateaued after marriage but his premarital contributions benefited from more years of compound growth, the fraction may understate the marital portion.

When contribution patterns were uneven, the tracing method produces a more accurate result. Tracing uses actual account statements from the date of marriage and the date of separation to identify which balance belonged to premarital contributions and which to marital contributions. Tracing is more expensive and time-consuming, but when the difference between the two methods is material, it is worth the cost.

The QDRO Penalty Exception: Lost If Rolled to an IRA

Under IRC Section 72(t)(2)(C), a distribution paid directly to an alternate payee from a qualified plan pursuant to a QDRO is exempt from the 10% early withdrawal penalty. This applies regardless of age. The rule has no age requirement. The key point is simply: if you are an alternate payee receiving funds under a QDRO directly from the plan, there is no penalty.

For comparison, there is a separate tax rule called the Rule of 55 (IRC Section 72(t)(2)(A)(v)) that allows the participant (not the alternate payee) to take distributions before age 59-1/2 without penalty if they separate from service in or after the year they turn 55. This rule applies to 401(k)s, 403(b)s, and pensions, and does not apply to 457(b) plans.

Here is the catch for alternate payees: if funds from a QDRO are rolled to an IRA, the Section 72(t)(2)(C) exception is lost. Distributions from the IRA before age 59-1/2 are subject to the 10% penalty (unless another exception applies, such as a Roth conversion).

This matters for client strategy. If your client is the alternate payee, is under age 59-1/2, and needs cash, she should take the distribution directly from the plan under the QDRO first. This distribution is penalty-free. She should then roll the remainder to an IRA for long-term growth. The sequence preserves the penalty-free option for the amount needed now and locks in tax-deferred growth for the rest.

Example: Maria is 45 and receives $150,000 as an alternate payee under a QDRO. She needs $30,000 for immediate expenses and wants to invest the remaining $120,000 for retirement. The optimal strategy is to take $30,000 directly from the plan (taxable as ordinary income, but with no 10% early withdrawal penalty, saving $3,000). The remaining $120,000 is rolled as a direct trustee-to-trustee transfer to a traditional IRA. The IRA funds grow tax-deferred, and Maria avoids the 10% penalty on the $30,000 she needed now.

Survivor Benefits: The Most Expensive QDRO Omission

Survivor benefits in a defined benefit pension are a hidden trap in QDRO drafting. A DB pension typically provides a QJSA (Qualified Joint and Survivor Annuity) or QPSA (Qualified Preretirement Survivor Annuity) that pays the participant’s surviving spouse (and sometimes children) benefits if the participant dies.

If the QDRO does not specifically address survivor benefits, the alternate payee loses all rights to the pension if the participant dies before retirement, or receives nothing if she is the survivor of a participant who has already retired. This is among the most expensive omissions in divorce financial planning.

A well-drafted QDRO specifies how survivor benefits are allocated. The alternate payee may be entitled to a share of the QJSA/QPSA benefit that mirrors her share of the pension itself. The specific language depends on the plan’s rules and the parties’ intentions, but the issue must be addressed explicitly.

IRAs: No QDRO Required, But Easy to Get Wrong

IRAs are not employer-sponsored retirement plans and are not governed by ERISA. They do not require a QDRO for division. Instead, IRAs are divided through a transfer incident to divorce under IRC Section 408(d)(6).

A transfer incident to divorce occurs when IRA assets are transferred from one spouse’s IRA to the other spouse’s IRA pursuant to a divorce decree, a separation agreement, or a court order. The transfer is not taxable. It is not reported as a distribution by the transferring spouse or as a contribution by the receiving spouse. The receiving spouse simply becomes the owner of the transferred IRA assets.

How to Divide an IRA Correctly

The transfer must meet two conditions: (1) it must be pursuant to a divorce or separation instrument (divorce decree, written separation agreement, or court order), and (2) it must be a direct transfer from one IRA to another IRA (or the account ownership is simply changed to the other spouse’s name).

If these conditions are met, the transfer is tax-free and penalty-free. No QDRO is needed, no plan administrator review is required, and the transfer can typically be completed by the IRA custodian within a few weeks using their standard paperwork.

The most common mistake with IRA division is withdrawing funds from one spouse’s IRA and depositing them into the other spouse’s account rather than executing a direct transfer. If the IRA owner withdraws $100,000, they owe income tax on the full amount plus a 10% penalty if under 59-1/2. Even if they give the $100,000 to their spouse, the tax and penalty hit belongs to the person who made the withdrawal. The proper method is always a direct transfer between custodians (or a reregistration of the account), not a withdrawal and deposit.

When dividing IRAs, use the IRA custodian’s “transfer incident to divorce” form or “change of ownership” form. Do not process it as a distribution and contribution. If the custodian is unfamiliar with the process, cite IRC Section 408(d)(6) and request a direct trustee-to-trustee transfer. This is routine for large custodians but smaller custodians occasionally need guidance.

When QDROs Are Rejected: The Six Most Common Mistakes

QDROs are frequently rejected on first submission. Understanding the most common mistakes gives you a roadmap to avoid them.

Mistake #1: Using the Plan’s Official Name Incorrectly. If the order says “Johnson Manufacturing 401(k)” but the official plan name is “Johnson Manufacturing Retirement Plan for Salaried Employees, 401(k) Subdivision,” the plan administrator will reject it for not matching the plan document.

Mistake #2: Ordering a Benefit Form the Plan Does Not Offer. If the plan does not allow lump-sum distributions to alternate payees, the QDRO cannot order one. Some plans require the alternate payee to wait until the participant reaches the plan’s earliest retirement age. If your client needs access before then, the solution is to request a separate interest arrangement (if the plan allows) or find a different asset to negotiate in the settlement.

Mistake #3: Failing to Address Annuity Surrender Charges. For 403(b) plans with annuity contracts, the order must specify how surrender charges are allocated. If the order is silent, the plan may deduct surrender charges from the alternate payee’s share.

Mistake #4: Omitting Survivor Benefit Language. If the QDRO does not address the QJSA/QPSA benefit for a DB pension, the alternate payee’s right to survivor benefits is ambiguous or lost. This is a major omission.

Mistake #5: Using Ambiguous Percentage or Dollar Language. If the order says “50% of the plan,” it is not clear whether that means 50% of the total balance or 50% of the marital portion (as determined by the coverture fraction). Plans will reject ambiguous orders.

Mistake #6: Failing to Verify the Plan’s Segregation and Payment Procedures. Each plan has its own procedures for segregating the alternate payee’s share and timing distributions. If the QDRO does not reference the plan’s specific procedures, the administrator may reject it for inconsistency with the plan’s administrative operations.

Key Takeaways

- Request the plan’s model QDRO before drafting. The most common rejections are due to a mismatch between the order and the plan’s official terms. Using the plan’s model or specific QDRO procedures eliminates most rejection reasons.

- Identify the plan type and use the correct division method. A 401(k) divides by account balance. A DB pension divides by formula or present value offset. A 403(b) requires attention to annuity restrictions. A 457(b) has no early withdrawal penalty. Military retirement follows DFAS procedures. Each plan type has its own playbook.

- Use the coverture fraction as a default, but check for uneven contributions. When salary or contribution patterns were uneven, the tracing method (using actual account statements) produces a more accurate result. The difference may justify the cost.

- If your client needs immediate cash and is under 59-1/2, take the distribution directly from the plan under the QDRO first. This avoids the 10% early withdrawal penalty. Roll the remainder to an IRA. The sequence matters.

- For DB pensions, address survivor benefits explicitly. If the QDRO does not specify how the QJSA/QPSA is allocated, the alternate payee may lose all rights to the pension if the participant dies. This is one of the most expensive oversights in divorce financial planning.

The Advisor’s Edge

Retirement plan division is publicly available information. The QDRO requirements are in ERISA and the Internal Revenue Code. The plan’s division rules are in its Summary Plan Description. The IRA transfer rules are in IRC Section 408(d)(6). Nothing about this topic is hidden.

What separates a CDFS™ from a generalist is the ability to think through the consequences of each division method and recommend the approach that actually serves the client’s financial situation and long-term goals. A generalist sees a retirement plan and drafts a generic QDRO. A specialist asks: Does this client need the funds now or later? Is the plan value stable or volatile? Will the client ever be remarried? What survivor benefits matter? What is the tax impact of each approach? These questions demand professional judgment, not just template compliance.

The Certified Divorce Financial Specialist™ (CDFS™) credential exists because retirement plan division, property classification, tax planning, and settlement analysis require expertise that goes far beyond the legal documents. The six mistakes outlined above are preventable, but only if someone is thinking about the consequences before the order is drafted. That someone should be your financial advisor.

For a detailed look at how QDRO distributions and retirement account division interact with filing status, basis carryover, and after-tax settlement value, see The Tax Consequences of Divorce: What Changed After 2017 and What Advisors Miss.

Sources and Notes: This article reflects QDRO requirements under ERISA and the Internal Revenue Code, IRA transfer rules under IRC Section 408(d)(6), and the early distribution penalty exception under IRC Section 72(t)(2)(C). Plan-specific division rules are based on standard Summary Plan Description provisions for 401(k), 403(b), 457(b), and defined benefit plans. Coverture fraction methodology follows standard actuarial practice. This article is refreshed annually.