What Advisors Get Wrong (and Keep Getting Wrong)

Seven years into the post-TCJA alimony rule, most practitioners understand intellectually that the deduction is gone. But the behavior change has not caught up. Advisors continue to structure settlements as if the tax subsidy still exists. They prop up alimony amounts that no longer make economic sense. They fail to run side-by-side comparisons of property-based structures versus support-based structures. They miss the fact that every settlement has two values: face value and after-tax value.

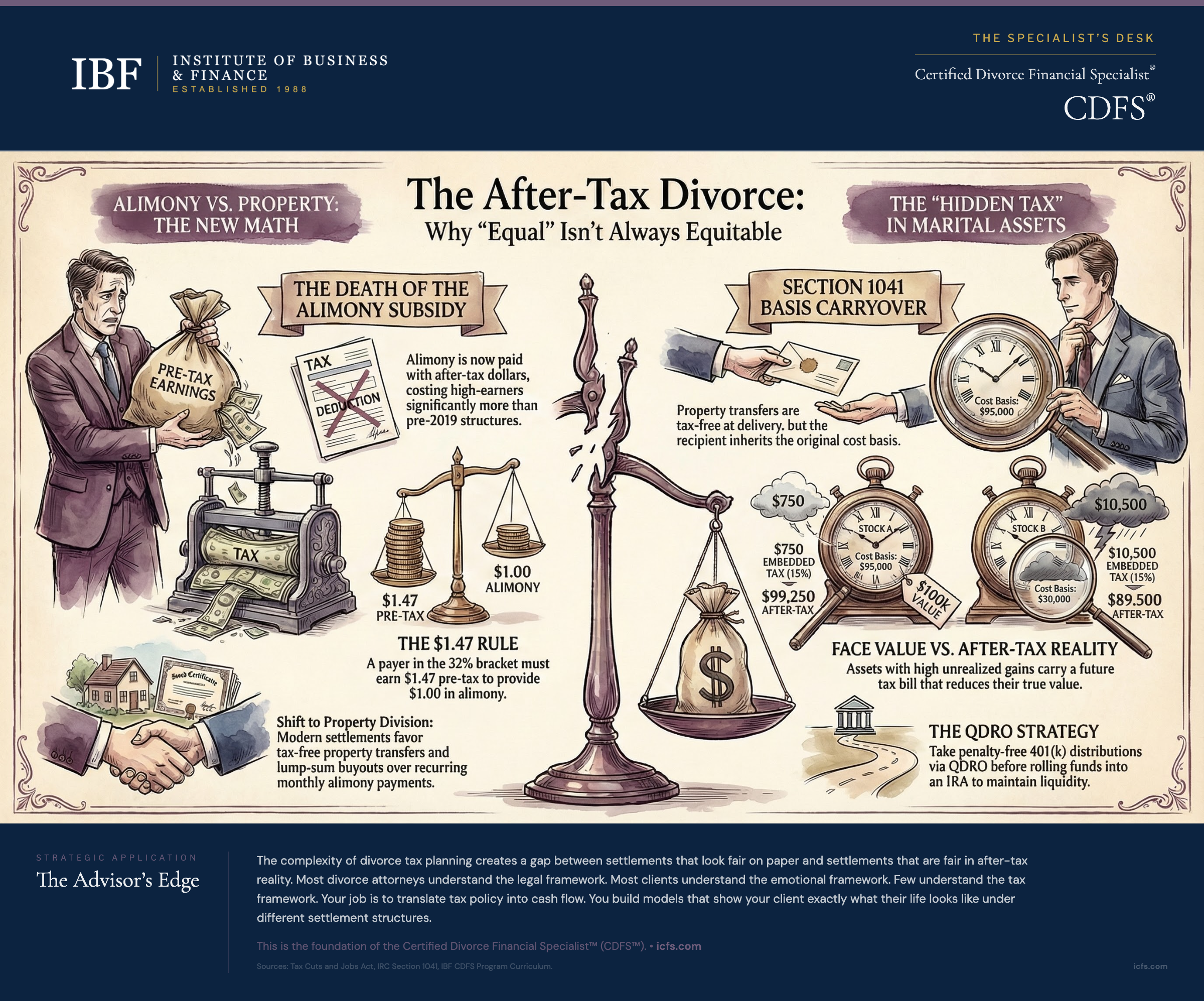

Here is what has changed: every dollar of spousal support that Kevin pays to Laura now costs Kevin a full pre-tax dollar (adjusted for his marginal rate). Before 2019, the math was different. The tax code was subsidizing the transfer. Now it is not. This matters because it makes property division, lump-sum buyouts, and retirement account divisions vastly more attractive than monthly alimony payments running for years.

The second mistake advisors make is treating Section 1041 as if it eliminates tax. It does not. Section 1041 defers the tax and transfers the basis. Laura may receive Kevin’s stock without triggering a taxable gain, but she inherits his $40,000 cost basis on a stock that is worth $150,000. When she sells it, she recognizes the $110,000 gain. That tax liability is embedded in the asset. Settlements that ignore basis are settlements that shortchange one spouse by tens of thousands of dollars.

Filing Status Strategy: The December 31 Rule

Your client’s marital status on December 31 determines their filing status for the entire year. This bright-line rule creates a critical strategic window. A couple married on January 1 but divorced by December 31 files as unmarried for the full year. A couple that finalizes the decree on January 2 must file as married.

When the divorce is expected to finalize near year-end, run both scenarios immediately. Calculate the combined tax liability under Married Filing Jointly, and calculate each spouse’s separate tax under Single or Head of Household status. The difference can exceed $10,000 for higher-income couples.

Why Head of Household matters. If your client has a qualifying dependent child who lived with them more than half the year, and your client paid more than half the cost of maintaining the home, your client qualifies as Head of Household even if technically still married on December 31 (provided they file separately from the ex-spouse and the ex-spouse did not live in the home during the last six months). Head of Household provides a much higher standard deduction and wider tax brackets than Single filing, making it substantially more favorable for a divorced parent with primary custody.

The practical rule: never finalize the timing of a divorce decree without modeling the tax impact first. A December finalization might save your client thousands compared to a January finalization, or vice versa, depending on their specific income and filing status.

Section 1041: Tax-Free Transfers Are Not Tax-Free Taxes

Section 1041 of the Internal Revenue Code allows tax-free transfers of property between spouses (or between former spouses if the transfer is incident to divorce). No gain or loss is recognized at the time of transfer. But here is what Section 1041 does not do: it does not make the tax disappear. It transfers the basis.

When Kevin transfers his brokerage account to Laura as part of the settlement, Laura takes Kevin’s adjusted basis in those assets. If Kevin’s basis is $95,000 and the current value is $185,000, Laura inherits $95,000 of basis and $90,000 of unrealized gain. When Laura eventually sells those stocks, she recognizes the $90,000 gain.

This matters because every asset in the settlement has two prices: the face value you see now, and the after-tax value you will see when it is sold. A settlement that divides a $400,000 portfolio 50/50 by face value is only fair if the embedded tax liability is also split 50/50. If one spouse receives assets with $200,000 of unrealized gains and the other receives assets with only $40,000 of unrealized gains, they are not dividing equally. They are creating a $24,000 tax difference at a 15% capital gains rate.

Always request tax lot detail from the custodian. Before finalizing any settlement involving investment accounts, request a detailed tax lot report from the brokerage or fund company. This report shows the cost basis and acquisition date for each lot. Without this data, you cannot calculate accurate after-tax values. If you are dividing a $250,000 brokerage account and you know only the total value, not the embedded basis, you are flying blind. The basis difference between the highest-basis and lowest-basis lot can swing the after-tax value by tens of thousands of dollars.

The Alimony Change: Permanent, Not Temporary

For divorces finalized after December 31, 2018, spousal support is not deductible by the payer and not included in the recipient's gross income. This provision has no sunset. It will not expire when other TCJA provisions expire. The One Big Beautiful Bill Act of 2025 extended many TCJA individual tax provisions but did not need to address alimony because it was already permanent.

This permanence reshapes how support fits into the overall settlement. Before 2019, a couple in different tax brackets could create value through alimony. If Kevin was in the 32% bracket and Laura was in the 12% bracket, each dollar of alimony cost Kevin only 68 cents (after the federal tax deduction) while creating a 20-cent net tax subsidy (the government lost 32 cents from Kevin’s deduction but recaptured 12 cents from Laura’s tax on the received amount). The gap was a tax subsidy. Higher alimony was economically possible.

Now, Kevin pays from after-tax income. Laura receives tax-free income. There is no subsidy. Kevin must earn $1.47 in pre-tax income to pay $1.00 in alimony (at the 32% bracket). This math strongly favors property division, which occurs at no tax cost under Section 1041.

The practical shift: modern settlements feature lower alimony amounts and larger property divisions compared to pre-2019 settlements. A settlement that would have included $3,000 monthly alimony for seven years ($252,000 total) now includes $2,000 monthly alimony for five years ($120,000 total) plus an additional $100,000 in property transfer. The total compensation to the lower-earning spouse is similar, but the structure avoids the after-tax drag of monthly payments.

Capital Gains: Basis Carryover and Lot Selection

Every asset in a divorce settlement has a cost basis, and that basis carries with the asset to the receiving spouse. The gap between the current value and the cost basis is the unrealized gain or loss. This embedded gain is a future tax liability that must be factored into settlement fairness.

Consider a simple example. Kevin’s portfolio contains two positions: Stock A worth $100,000 with basis $95,000 (only $5,000 gain) and Stock B worth $100,000 with basis $30,000 ($70,000 gain). If Laura receives Stock B, she inherits $70,000 of embedded gain. At a 15% capital gains rate, that represents $10,500 in future tax liability. If Laura receives Stock A instead, the embedded tax is only $750. The difference is $9,750 in after-tax value, even though both positions are worth $100,000 face value.

Sophisticated practitioners request the custodian to break down every lot (each purchase date and cost basis pair) and then allocate lots to equalize the embedded tax burden, not just the face value. This requires more work upfront but produces a genuinely equitable settlement.

The mutual fund complication: mutual fund shares with reinvested dividends can have dozens or hundreds of individual tax lots accumulated over decades. A mutual fund held for 20 years with reinvested distributions represents a complex basis calculation. Request the mutual fund company's lot detail. Most major custodians can produce this. If they cannot, flag the account for further investigation.

The Marital Home and Section 121 Planning

The marital home is often the largest single asset in a divorce. The Section 121 exclusion allows each taxpayer to exclude up to $250,000 of gain on the sale of a principal residence (or $500,000 for married filing jointly) if they have owned and used the home as a principal residence for at least two of the five years before the sale.

This creates three planning considerations. First, if the couple sells the home before the divorce is final, they can file jointly and claim a $500,000 exclusion. After the divorce, each spouse can claim only $250,000. Selling before the decree can save substantial capital gains tax. Second, if one spouse keeps the home and sells it later, that spouse needs to have lived there for two of the five years before the sale. The other spouse who moved out may lose their Section 121 benefit on that property. Third, IRC Section 121(d)(3)(B) explicitly protects the departing spouse’s exclusion by treating them as using the property as their principal residence during any period they own it while the staying spouse uses it under a divorce instrument. This statutory protection eliminates the need for special drafting beyond ensuring the decree qualifies as a divorce or separation instrument under the tax code.

Retirement Accounts: The QDRO Distribution Sequence

When dividing 401(k)s and other employer plans through a Qualified Domestic Relations Order (QDRO), the non-employee spouse receives distributions that are exempt from the 10% early withdrawal penalty at any age. This QDRO exception is one of the only ways to access retirement funds before age 59-1/2 without a penalty.

The critical tactical sequence: if your client needs immediate cash, take the distribution from the plan under the QDRO before rolling the balance to an IRA. A $25,000 distribution from the 401(k) is penalty-free. Once the funds are rolled to an IRA, the QDRO penalty exception no longer applies. A $25,000 withdrawal from an IRA before age 59-1/2 triggers a $2,500 penalty (10% of $25,000). The order of operations can cost thousands.

For traditional retirement accounts (pre-tax contributions), the distribution is subject to ordinary income tax but exempt from the 10% penalty. For Roth accounts, distributions may be tax-free if qualified. Account for the after-tax value of retirement accounts when dividing the settlement. A $200,000 traditional 401(k) is not worth $200,000 in after-tax terms. At a 22% effective tax rate, it is worth approximately $156,000. At a 32% effective rate, it is worth approximately $136,000. The tax drag on retirement assets is substantial.

Bracket Compression: The Divorce Tax Penalty

When your client transitions from married filing jointly to single or head of household, tax bracket compression becomes a concern primarily for higher-income couples. The tax bracket breakpoints for single filers are narrower than for married filers through the 32% bracket, where MFJ thresholds are exactly double the single-filer thresholds. The standard deduction is lower. The effect varies by income.

For couples with equal incomes under current law, the marriage penalty is minimal or nonexistent below the 35% bracket. A couple earning $200,000 combined ($100,000 each) pays approximately the same combined federal income tax after divorce as before, since the TCJA bracket thresholds are indexed to eliminate the penalty for equal earners. However, high-income couples earning above the 35% bracket, or couples with significantly unequal incomes, do face a real tax penalty upon divorce. Additionally, if one spouse qualifies as Head of Household (due to primary custody of a qualifying dependent), the combined post-divorce tax may actually be lower than filing jointly. The key planning point: model the actual numbers for your client’s specific income level and filing status. Do not assume a penalty exists until you calculate it. For equal earners below the 35% bracket, the penalty may be zero. For higher earners or unequal income couples, Head of Household status may offset or eliminate it.

Client Conversation: When Assets Look Equal But Taxes Are Not

Your client (the higher-earning spouse) receives a settlement proposal that awards each party $300,000 in assets from the marital estate. It looks fair on the surface. But here is what they do not see: the assets your client receives include $150,000 in real estate with a stepped-up basis equal to current value (no embedded gains) plus $150,000 in cash. The other spouse receives $300,000 in investment securities with only $30,000 of cost basis, representing $270,000 in embedded unrealized gains.

At a 15% long-term capital gains rate, the other spouse’s embedded tax is $40,500. Your client’s tax exposure is nearly zero. The other spouse is receiving $300,000 in face value but only approximately $259,500 in after-tax value. Your client is receiving the full $300,000 after-tax value. The settlement is inequitable by $40,500, but nobody sees it until assets are sold years later.

This is where the financial advisor's role becomes critical. You bring the tax dimension to the negotiation. You build a settlement model that shows the after-tax value of every asset, not just the face value. You show your client that receiving $300,000 in assets with $270,000 of embedded gains is not the same as receiving $300,000 in assets with no embedded gains. You create a level negotiating field where both parties understand what they are actually receiving.

Key Takeaways

- Filing status is not a default. It is a strategic decision with dollar consequences. Calculate the tax impact of finalizing before versus after December 31. A difference of two weeks can shift the tax liability thousands of dollars. If your client will be the custodial parent, model Head of Household status; it is more favorable than Single for divorced parents.

- Section 1041 defers tax; it does not eliminate it. Every asset has both a face value and an after-tax value. Request tax lot details from every brokerage and fund company. Allocate lots to equalize the embedded tax burden. Settlements that ignore basis are settlements that shortchange one spouse.

- The post-2018 alimony rule is permanent and reshapes settlement structure. Spousal support is paid from after-tax dollars. Property division under Section 1041 is tax-free at transfer. Modern settlements favor property transfers and lump-sum buyouts over monthly alimony. If your client is the payer, advocate for trading alimony for property. If your client is the recipient, ensure the property allocation is adequate compensation for reduced support.

- Calculate the after-tax cost of every settlement structure. Build a model showing total dollars and present value. A client who hears "$2,000 monthly alimony for ten years" should also see "$240,000 total obligation." The total is what drives the negotiation.

- Retirement accounts have substantial embedded tax liability. A $200,000 401(k) is worth less than $200,000 after tax. Model the after-tax value when dividing retirement accounts. If your client is receiving a QDRO distribution and needs immediate cash, take the distribution from the plan before rolling to an IRA. The QDRO penalty exception applies only to plan distributions, not IRA withdrawals.

The Advisor’s Edge

The complexity of divorce tax planning creates a gap between settlements that look fair on paper and settlements that are fair in after-tax reality. Most divorce attorneys understand the legal framework. Most clients understand the emotional framework. Few understand the tax framework. This is where the advisor becomes indispensable.

Your job is to translate tax policy into cash flow. You build models that show your client exactly what their life looks like under different settlement structures. You quantify the hidden costs of bracket compression, the embedded gains in investment accounts, the tax drag on retirement assets. You turn vague proposals into concrete numbers that both parties can understand and negotiate from.

The practitioners who excel at this work develop a reputation for being the person who brings the financial reality to the negotiating table. Attorneys compete on legal strategy. Your clients’ ex-spouses have their own advisors. But an advisor who can model the post-TCJA tax treatment of property division, alimony, and retirement accounts with precision becomes the most trusted voice in the room.

This is the foundation of the Certified Divorce Financial Specialist™ designation. The CDFS™ curriculum in Chapter 6 walks you through the tax mechanics. Chapter 7 applies those mechanics to spousal support negotiation strategy. Chapter 12 covers real estate strategy and Section 121 planning. Chapter 13 teaches you how to build a complete settlement model that optimizes the total package for your client. Master these tools, and you will be the advisor that family law attorneys call when they need to get the numbers right.

For detailed analysis of retirement account division mechanics and the interaction between QDRO distributions and after-tax planning, see the related article on Dividing Retirement Accounts in Divorce: QDROs and What Advisors Get Wrong.

Sources and Notes: This article reflects tax law as of March 2026, including the Tax Cuts and Jobs Act of 2017 (permanent alimony provisions), the One Big Beautiful Bill Act of 2025, IRC Section 1041, IRC Section 121(d)(3)(B), and QDRO distribution rules under IRC Section 72(t)(2)(C). Tax rates and bracket thresholds reflect current law. Consult a tax professional for client-specific guidance.