Opening Insight

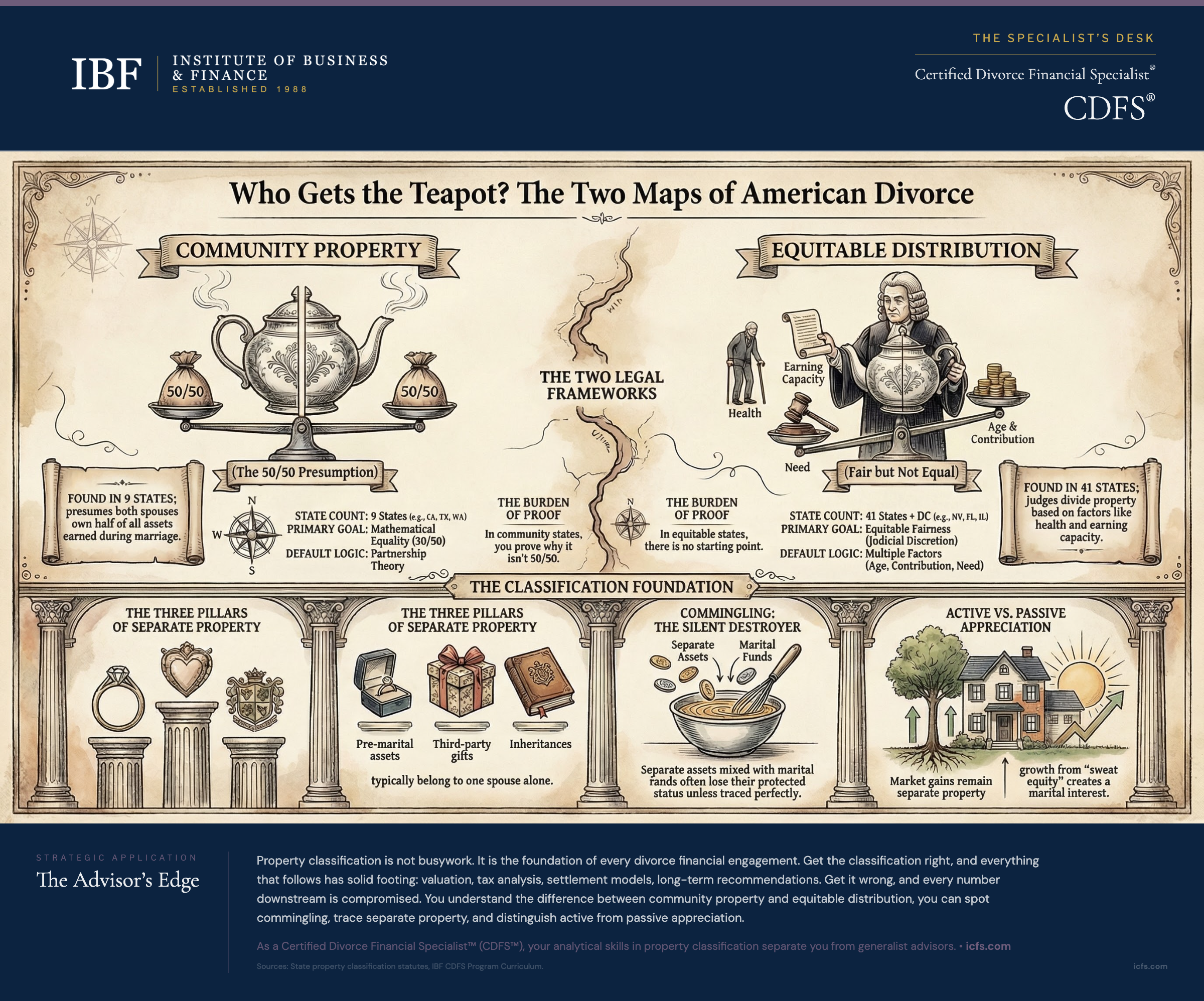

Most financial advisors have never thought about the difference between community property and equitable distribution until a divorce client asks, "What will my share be?" The answer is not what the client expects. It is not "50/50" or "whatever is fair." The answer is "it depends on where you live." The law in nine states presumes that each spouse owns half of all marital property. In the other 41 states, a judge decides what is fair based on a dozen different factors. This single legal distinction shapes every number in the divorce financial analysis.

The framework your client's state uses is not optional context. It is the foundation. Get it wrong, and every settlement model, every tax analysis, every recommendation that follows is built on sand. Get it right, and the client has a realistic map of what to expect.

The Two Frameworks That Divide the Country

Community Property: The 50/50 Presumption

Nine states follow community property rules: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. (Alaska allows married couples to opt into community property by agreement, and Florida, Kentucky, South Dakota, and Tennessee offer community property treatment through trusts for specific planning purposes.)

In community property states, the default rule is simple: all property acquired by either spouse during the marriage belongs equally to both spouses, regardless of who earned it or whose name is on the title. When the marriage ends, each spouse is entitled to half of the community property.

This rule applies to everything earned during the marriage. If one spouse earns $120,000 and the other earns $80,000, their combined $200,000 in annual income is community property. The retirement contributions funded by that income are community property. The savings accounts funded with joint earnings are community property. The difference in earning power does not change the classification.

The community property system reflects a partnership theory of marriage. Both spouses contribute to the marital enterprise through income, homemaking, child-rearing, or supporting the other spouse's career. Both are entitled to an equal share of the result.

When you work with a client in a community property state, the initial classification is straightforward: everything acquired during the marriage is presumed community unless proven otherwise. Your analytical energy goes toward identifying separate property claims and tracing, not toward arguing for a larger share. The fight in community property cases is almost always about what is NOT community, not about what is.

Equitable Distribution: Fair But Not Equal

The remaining 41 states and the District of Columbia follow equitable distribution. Under this framework, courts divide marital property "equitably," meaning fairly but not necessarily equally. A judge may award one spouse 60% of marital assets and the other 40%, or 70/30, or any split the judge considers fair based on the circumstances.

Courts weighing equitable distribution apply multiple factors. While specific factors vary by state, most statutes include some version of these:

- Length of marriage. Longer marriages tend toward more equal splits.

- Income and earning capacity. A lower-earning spouse may receive more assets to offset the income disparity.

- Age and health. Older or less healthy spouses may receive more to account for reduced earning years.

- Contributions to the marriage (including homemaking). Non-financial contributions are recognized.

- Standard of living during the marriage. Courts try to preserve reasonable post-divorce standards.

- Tax consequences of property division. After-tax value matters, not face value.

- Dissipation or waste of marital assets. A spouse who wasted assets may receive less.

- Prenuptial or postnuptial agreements. Enforceable agreements can override statutory factors.

- Custody arrangements. The primary custodian may receive the marital home.

- Each spouse's separate property. More separate property may reduce the marital share.

In equitable distribution states, you need to model a range of outcomes. A judge applying these factors has considerable discretion. Two judges could reach different conclusions on the same case. Your job is not to predict the judge's decision. Your job is to show what different splits look like financially so the client can evaluate settlement offers against the range of likely trial outcomes.

The Practical Difference

In practice, the distinction between community property and equitable distribution is less dramatic than the rules suggest. Equitable distribution courts frequently arrive at divisions that are close to equal, even though the range of outcomes is wider than in community property states. The key difference is not necessarily the final split. It is the process.

In community property states, the 50/50 split is the starting point, and either spouse must prove a reason to deviate. In equitable distribution states, there is no automatic starting point. The entire division is determined by the court's analysis of the statutory factors. This means more uncertainty, more room for negotiation, and more need for the financial analysis you provide.

Why the Details Matter: State-Specific Rules

Community property and equitable distribution are not monolithic categories. States within each framework have their own rules that shift the analysis significantly.

Texas: A community property state that does not require equal division. The Texas Family Code § 7.001 allows a "just and right" division, meaning judges can award unequal splits based on earning capacity, health, the needs of minor children, fault, and other factors. A Texas divorce can look more like an equitable distribution case than a traditional community property case.

California: A community property state with a strong presumption of equal division, but with exceptions. California Family Code § 852(a) requires an express written declaration before transmutation can occur between spouses. California also allows reimbursement or unequal allocation when community funds were used for one spouse's education or training, or when one spouse has misappropriated community assets.

New York: An equitable distribution state that applies an active/passive framework to valuation dates. Passive assets like stock portfolios are generally valued as of the date of trial (capturing market-driven changes), while active assets like a business are generally valued as of the date of commencement (so the titled spouse does not benefit from post-filing efforts). Courts treat this framework as a guidepost rather than a fixed rule, retaining discretion to select the date that produces the most equitable result, as established in McSparron v. McSparron (1995).

Knowing your state's specific rules within its general framework is essential before you run any analysis. The broad framework (community property vs. equitable distribution) tells you the starting point. The state-specific rules tell you where the exceptions live.

The Classification Question That Underlies Everything

Regardless of framework, the same fundamental question applies: is this asset marital property (subject to division) or separate property (belonging to one spouse alone)?

Marital property generally includes all assets acquired by either spouse during the marriage, with funds earned during the marriage. Separate property includes three primary categories:

- Pre-marital assets. Property owned before the marriage. A spouse's $150,000 brokerage account brought into the marriage is separate property (assuming it remains traceable and uncontaminated by marital funds).

- Gifts to one spouse. Property received as a gift by one spouse, not the couple. A gift from one parent to one child is separate. A gift from both parents to both spouses is marital.

- Inheritances to one spouse. Property received through inheritance by one spouse. An inheritance is separate property even if the inheritance arrived during the marriage.

The practical problem: separate property claims are only as strong as the evidence supporting them. In a divorce, the spouse claiming separate property bears the burden of proving it. This means your client needs documentation showing the asset existed before the marriage or was received as a gift/inheritance, the asset remained identifiable and traceable, and the asset was not commingled with marital funds.

If Kevin's $150,000 pre-marital brokerage account was maintained in a separate account, never funded with marital income, and never mixed with marital assets, his separate property claim is strong. If he deposited his paychecks into that account, used it to pay marital expenses, and mixed it with his spouse's money, the $150,000 separate property claim becomes a tracing exercise, and possibly a losing argument.

Commingling: The Silent Destroyer of Separate Property Claims

Commingling occurs when separate property is mixed with marital property to the point where the separate component can no longer be identified. The classic example: a spouse deposits a $50,000 inheritance into the joint checking account, then uses that account for daily expenses, paychecks, bills, and transfers for ten years. By the time of divorce, the inheritance has been so thoroughly mixed with marital funds that it cannot be identified.

Commingling does not automatically destroy a separate property claim. It creates a tracing problem. If the spouse can trace the separate funds through the account history and show what happened to each dollar, the separate property claim survives. If the funds are so thoroughly mixed that tracing is impossible, the separate property claim fails and the entire account is treated as marital.

Common commingling scenarios:

- Depositing inheritance or gift funds into a joint account used for marital expenses

- Using separate property to pay marital debts (mortgage, credit cards, living expenses)

- Adding marital funds to a pre-marital account

- Reinvesting separate property proceeds alongside marital investment funds

- Using a pre-marital business to generate marital income without tracking contributions

When you identify a potential commingling situation, ask one question first: is the separate property traceable? If the account has clean records showing the original deposit, subsequent deposits, and withdrawals, tracing may be straightforward. If the account is a joint account that has been used as the family's operating account for 15 years, the tracing will be expensive and the outcome uncertain. Help the client and attorney assess whether the tracing cost is justified by the potential separate property recovery.

Transmutation: Accidental or Intentional

Transmutation is the legal process by which property changes its character, from separate to marital, from marital to separate, or from one spouse's separate property to the other spouse's separate property. Transmutation can happen intentionally or accidentally.

Intentional transmutation occurs when a spouse deliberately changes the ownership or character of property. Common examples:

- Adding a spouse's name to a pre-marital asset (adding to the title of a pre-marital rental property)

- Signing a written agreement changing the character of property (a postnuptial agreement converting separate property to marital)

- Using separate property to purchase a jointly titled asset (using an inheritance for the down payment on a marital home)

Accidental transmutation occurs when a spouse's actions change the property's character without intending to do so. The most common accidental transmutation: adding a spouse's name to a bank account "for convenience" so the other spouse can write checks or access funds in an emergency. In many jurisdictions, adding the other spouse's name to a separate account creates a presumption that the owning spouse intended to gift the account to the marriage.

Some states have specific transmutation requirements. California requires an "express written declaration" before transmutation can occur between spouses. This means separate property cannot be converted to community property in California without a written document meeting statutory requirements. Other states allow transmutation by conduct alone, without any written agreement.

When Separate Property Appreciates: Active vs. Passive

When separate property increases in value during the marriage, the classification of that increase depends on why it grew. This active/passive distinction is one of the most consequential, and most frequently litigated, issues in divorce property classification.

Passive appreciation occurs when separate property increases in value due to market forces, inflation, or other factors unrelated to either spouse's efforts. Passive appreciation of separate property remains separate property in most jurisdictions.

Examples:

- A pre-marital stock portfolio that increases in value due to market gains, with neither spouse actively managing the portfolio

- Pre-marital real estate that appreciates due to neighborhood development and general market trends

- An inherited painting that increases in value due to the artist's growing reputation

The key test: did the increase result from something the market did, or something a spouse did? If the market caused it, the appreciation is passive and remains separate.

Active appreciation occurs when separate property increases in value due to the efforts, skills, or labor of either spouse during the marriage. In most jurisdictions, active appreciation of separate property creates a marital interest in the increase.

Examples:

- A pre-marital business that grows during the marriage because the owning spouse worked in the business (the growth reflects the spouse's labor, which is marital)

- A pre-marital rental property that increases in value because the couple spent marital funds on renovations and the other spouse managed tenant relations

- A pre-marital brokerage account in many jurisdictions that increases in value because the owning spouse actively traded securities and made investment decisions during the marriage

The active/passive distinction creates some of the hardest questions in divorce property classification. Consider a pre-marital business. If a spouse owned a small consulting practice worth $100,000 at the date of marriage and it is now worth $500,000, the classification of the $400,000 increase depends on what drove the growth. If the spouse worked 60 hours a week building the business, most courts would classify some or all of the $400,000 increase as marital property because it reflects the spouse's labor during the marriage. If the business grew passively because the industry expanded and the spouse's role was minimal, more of the increase would remain separate property.

The active/passive distinction matters enormously for business owners and active investors. When you identify a separate property asset that has appreciated significantly during the marriage, always ask: "Why did it grow?" If the answer involves either spouse's time, effort, skills, or use of marital funds, you have a potential active appreciation claim. Flag it for the attorney and begin gathering the evidence needed to analyze the growth pattern.

The Valuation Date Question: Which Day Matters?

Property classification answers "whose property is this?" Valuation answers "what is it worth?" But there is a question between those two that can shift the financial outcome dramatically: "What date do we use to determine the value?"

Different jurisdictions use different valuation dates. The three most common are:

- Date of separation: Captures value at the time the marital partnership effectively ended. Post-separation gains or losses belong to the earning/owning spouse.

- Date of filing: Used by many equitable distribution states. Captures value at the formal beginning of the divorce process.

- Date of trial or settlement: Used by several equitable distribution states (including New York for passive assets). Captures the most current value; can create incentives to delay proceedings.

Some states use different dates for different types of assets. New York courts typically apply an active/passive framework where passive assets (like a stock portfolio) are generally valued as of the date of trial, because market-driven changes should be shared. Active assets (like a business) are generally valued as of the date of commencement, so the titled spouse does not benefit from post-filing efforts. However, courts retain discretion to select whichever date produces the most equitable result. Some other states allow similar court discretion to choose the most equitable date.

The valuation date matters because market values change. Consider a joint brokerage account worth $200,000 on December 1 (the date of separation), $180,000 on January 15 (the date of filing), and $240,000 on June 1 (the date of trial). The asset being divided is the same portfolio, but the value being divided differs by $60,000 depending on which date the court uses.

If the jurisdiction uses the date of separation, and the court awards one spouse 50%, that spouse receives $100,000. If the jurisdiction uses the date of trial, that spouse receives $120,000. The $20,000 difference is entirely a function of the valuation date, not any change in the parties' circumstances or contributions.

This is not theoretical. Markets can move significantly between separation, filing, and trial, especially when divorces take 12 to 18 months to finalize. Always determine the applicable valuation date in your jurisdiction before running any financial analysis. Ask the attorney at the start of the engagement: "What valuation date does this court typically use?" If the answer is discretionary or asset-specific, model multiple dates and show the client the range.

Dissipation: When One Spouse Wastes Marital Assets

Dissipation occurs when one spouse uses marital assets for a non-marital purpose during the breakdown of the marriage. Courts take dissipation seriously because it represents one spouse unilaterally reducing the other spouse's share of the marital estate.

Dissipation typically involves spending marital funds on:

- An extramarital relationship (gifts, travel, housing for a paramour)

- Gambling losses beyond the couple's historical norm

- Substance abuse expenses

- Excessive or unreasonable spending during the divorce process

- Destroying, hiding, or transferring assets to prevent division

- Failing to maintain marital assets (letting property fall into disrepair)

Not all spending constitutes dissipation. Normal living expenses, even generous ones, are not dissipation if they are consistent with the couple's historical spending pattern. A spouse who has always spent $3,000 per month on personal expenses is not dissipating by continuing to spend $3,000 per month during the divorce. A spouse who suddenly increases personal spending to $8,000 per month after filing for divorce raises a dissipation flag.

When reviewing financial records, look for these warning signs: sudden increases in cash withdrawals, new credit card accounts opened near separation, large transfers to family members or friends, business revenue declining without explanation, cryptocurrency purchases, expensive gifts to non-family members, paying down one spouse's separate debt with marital funds, or sudden "bad" investments.

Your role in dissipation is analytical: identify the red flags, document the evidence, and quantify the amounts. A dissipation analysis typically involves establishing the historical spending pattern, identifying the deviation, tracing the funds, and quantifying the claim. When you identify potential dissipation, document it clearly and present the evidence to the attorney. Do not characterize the spending as dissipation; that is a legal conclusion. Your job is to show the numbers and let the evidence speak.

Key Takeaways

- Know your state. Community property states presume 50/50 division; equitable distribution states divide based on multiple factors. This single distinction drives your entire analysis.

- Separate property requires proof. Pre-marital assets, gifts, and inheritances are separate in both frameworks, but the claiming spouse must document and defend the claim.

- Commingling is the killer. When separate property mixes with marital property, tracing becomes expensive and uncertain. Flag commingling early.

- Active appreciation creates marital interest. When separate property grows because of a spouse’s effort, that growth is typically marital. Market gains remain separate.

- The valuation date changes the numbers. Different dates produce different values. Always confirm which date your jurisdiction uses, then model alternatives.

- Dissipation is a quantifiable claim. Establish the baseline spending pattern, identify deviations, and present the evidence. Let the attorney build the legal argument.

The Advisor’s Edge

Property classification is not busywork. It is the foundation of every divorce financial engagement. Get the classification right, and everything that follows has solid footing: the valuation, the tax analysis, the settlement models, the long-term recommendations. Get it wrong, and every number downstream is compromised.

As a Certified Divorce Financial Specialist™ (CDFS™), your analytical skills in property classification separate you from generalist advisors. You understand the difference between community property and equitable distribution, you can spot commingling and trace separate property through complex account histories, you can distinguish active from passive appreciation, and you know how to flag dissipation and asset concealment.

This foundation positions you to do the real work of divorce financial planning: creating realistic settlement scenarios, modeling tax consequences, structuring property divisions in ways that minimize tax liability, and helping clients understand the long-term financial impact of their divorce decisions. The framework comes first. The strategy comes second.

Your next step is to work with the client and attorney to build a complete property classification worksheet: every asset listed, classified, documented, and assessed for completeness. That worksheet becomes the source of truth for all subsequent analysis.

For a closer look at how property classification intersects with the most contested asset in many divorces, see Business Valuation in Divorce: What Advisors Need to Know Before the Expert Shows Up.

Sources and Notes: This article synthesizes property classification frameworks from the Uniform Marriage and Divorce Act, state-specific family codes (including Texas Family Code § 7.001 and California Family Code § 852(a)), and case law including McSparron v. McSparron (1995). Specific state rules may vary; consult local counsel for jurisdiction-specific guidance.