Most financial advisors know trusts exist. Fewer understand what each one does, when it makes sense, or how to talk about trusts with clients in plain language. You’ll hear estate attorneys recommend structures with names that sound like alphabet soup: RLT, QTIP, ILIT, AB trust. Each one solves a specific problem, but most clients need just a few types.

Your role as the financial advisor sits between the client and the attorney. You won’t draft trusts. But you’ll answer the question every client eventually asks: “Do I need a trust, and if so, what kind?” You’ll help clients understand why their attorney made a particular recommendation. And you’ll verify that the chosen structure actually matches what the client wanted to accomplish.

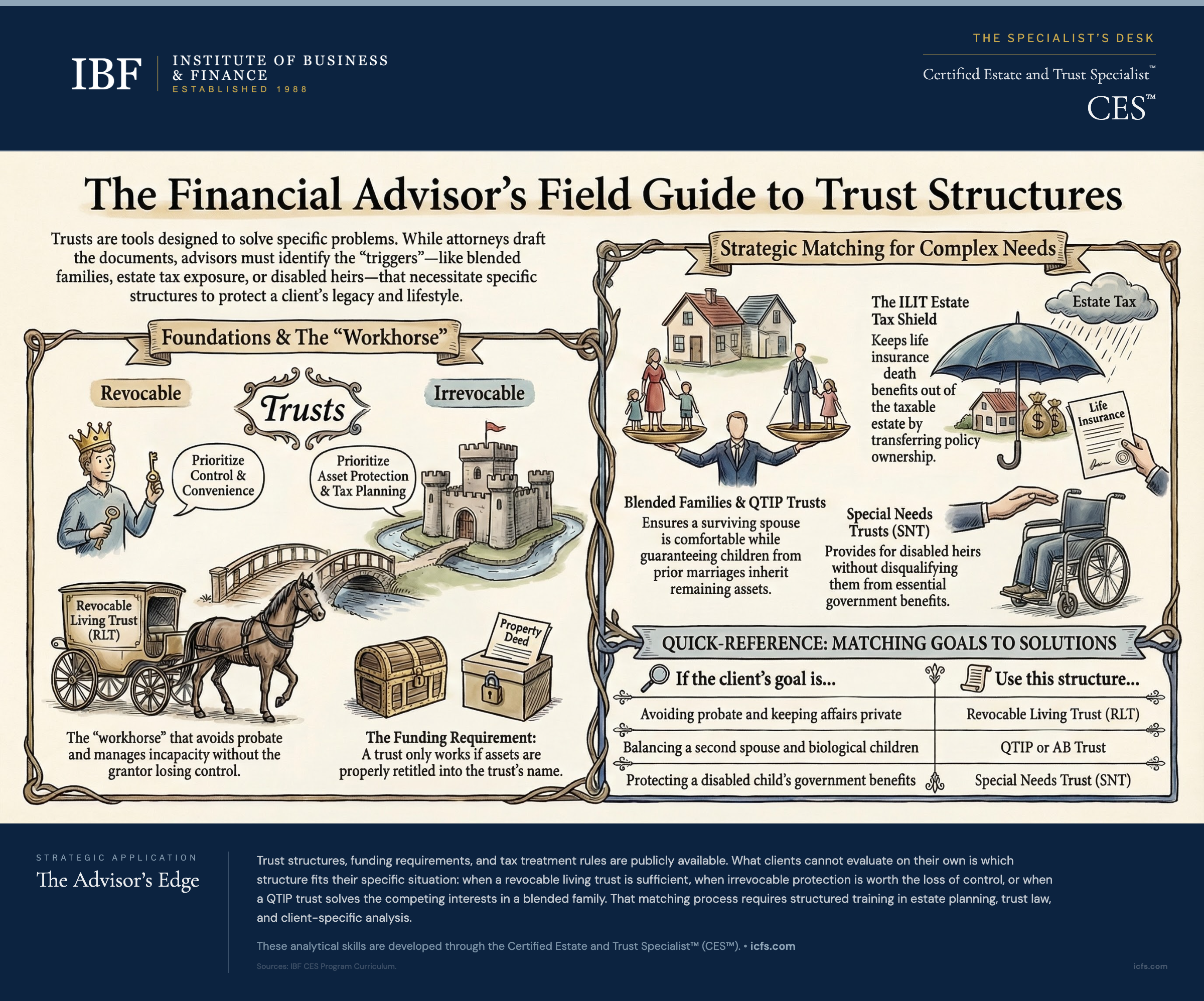

Understanding Trust Basics First

Before diving into trust types, the foundation matters. Every trust involves three roles. The grantor creates the trust and decides what happens. The trustee manages the assets and follows the grantor’s instructions. The beneficiary receives the benefit of the trust property.

The critical distinction is revocable versus irrevocable. A revocable trust can be changed or cancelled anytime. The grantor retains control. An irrevocable trust, once created, cannot be changed. The grantor gives up control in exchange for specific legal benefits: asset protection, estate tax removal, or benefits planning.

This distinction shapes everything that follows. Revocable trusts serve control and convenience. Irrevocable trusts serve protection and planning.

Establishing a trust costs more than preparing a simple will. Trust preparation typically runs $1,500 to $4,000 for straightforward estates, rising to $5,000 or more for complex situations involving multiple properties, blended families, or specialized structures. This higher cost is justified when the client’s circumstances demand the functions a trust provides: avoiding probate across multiple states, managing assets during incapacity, maintaining privacy, or protecting assets from creditors.

The Revocable Living Trust: What Most Clients Need

The revocable living trust, or RLT, is the workhorse of estate planning. It accomplishes three things that wills cannot: it avoids probate, it handles incapacity seamlessly, and it keeps disposition details private.

Here’s how it works. The grantor creates the trust, names themselves as initial trustee, and retains complete control. The grantor can amend the trust, revoke it entirely, or spend all the assets. Nothing changes in daily life except that accounts and real estate are now titled in the trust’s name. During the grantor’s lifetime, the grantor remains the primary beneficiary and trustee.

At death, the successor trustee takes over. This person manages the trust assets and distributes them according to the trust terms. No probate court is involved because the trust, not the individual, owns the assets. The assets never pass through the estate.

The RLT solves the probate problem without requiring the grantor to give up anything. That’s why it’s so popular. For a client with a house and investments titled in the trust, probate is avoided entirely. Retirement accounts and life insurance pass by beneficiary designation, which is separate from the RLT. For a client in multi-state properties, avoiding separate probate proceedings in each state saves time and cost.

Incapacity handling is the second major benefit. If the grantor becomes incapacitated, the successor trustee steps in and manages assets without court guardianship. The client’s financial life continues uninterrupted.

The third benefit is privacy. Wills are public documents. Anyone can walk into the courthouse and see who inherited what. Trusts are private. The public never sees the distribution plan.

What RLTs cannot do: they don’t provide asset protection. Since the grantor retains complete control, creditors can reach trust assets as if the grantor owned them outright. They don’t save estate taxes because the grantor’s retained powers mean all trust assets are included in the taxable estate.

For most clients, the RLT is the only trust they need.

Marital Trusts: When Spouses Need Protection from Each Other

When a married person dies, federal law allows unlimited transfers to the surviving spouse tax-free, except for non-citizen spouses, which require a Qualified Domestic Trust. That sounds ideal for most couples. It creates a problem though: if everything goes outright to the surviving spouse, the first spouse’s estate never uses their own exemption. Marital trusts solve this by capturing some assets in a structure that uses the deceased spouse’s exemption while still benefiting the surviving spouse.

The traditional AB trust, also called a bypass or credit shelter trust, splits assets at the first death into two portions. Trust A holds assets qualifying for the marital deduction. The surviving spouse typically has control over this portion. Trust B holds assets up to the exemption amount. These assets are removed from the surviving spouse’s estate. The surviving spouse can receive income and often principal through provisions for health, education, maintenance, and support, but doesn’t own the assets.

When the surviving spouse dies, Trust A assets are included in their estate, while Trust B assets pass to the next generation without further estate tax.

AB trusts were standard practice when each spouse’s exemption had to be used or lost at death. Modern tax law changed that. In 2011, portability was introduced for deaths in 2011 and 2012, and was made permanent under the American Taxpayer Relief Act of 2012 (effective January 2, 2013). For couples with estates under the combined federal exemption ($30 million for couples in 2026 with a portability election), AB trusts became optional for federal tax purposes.

But AB trusts still matter in specific situations. Assets in the B trust are protected from the surviving spouse’s creditors. That protection doesn’t exist with portability. States with their own estate taxes don’t recognize portability. A couple in a state with a lower exemption might use an AB structure to capture both state exemptions. Assets in the B trust, and all future growth, are excluded from the surviving spouse’s estate. For assets that appreciate significantly, the estate tax savings can be substantial. And portability doesn’t apply to the generation-skipping transfer tax exemption. Clients planning for grandchildren might still benefit.

The QTIP trust (Qualified Terminable Interest Property) solves a different marital problem. The surviving spouse receives all income from the trust for life, but cannot control who receives the remainder. The deceased spouse’s trust document determines where the remainder goes.

QTIP trusts serve blended families especially well. When spouses have children from prior marriages, the QTIP ensures the surviving spouse is provided for while guaranteeing that the deceased spouse’s children eventually receive the trust principal. Consider William, age 72, married to his second wife Margaret for 15 years. William has two children from his first marriage. William wants Margaret to live comfortably if he dies first, but also wants to ensure his children eventually receive his assets. A QTIP trust gives Margaret lifetime income while guaranteeing William’s children receive the remainder after Margaret’s death.

QTIP trusts can create tension. The surviving spouse wants more income or principal access. The remainder beneficiaries want assets preserved. The trustee, often a child or professional, must balance competing interests. These dynamics deserve discussion during planning, not after the first death when conflict is harder to resolve.

Irrevocable Life Insurance Trusts: Keeping Death Benefits Out of the Estate

Life insurance death benefits escape income tax. They don’t escape estate tax. If the deceased owned a life insurance policy at death, the full death benefit is included in the taxable estate. For a client with a $5 million estate and a $3 million life insurance policy, the estate becomes $8 million for tax purposes.

The Irrevocable Life Insurance Trust solves this by removing the policy from the insured’s estate entirely. The trust, not the insured, owns the policy. When the insured dies, the death benefit passes to the trust, not to the insured’s estate. The beneficiaries receive the proceeds according to the trust terms.

The grantor creates an irrevocable trust and names it as owner and beneficiary of a life insurance policy. As a general rule, the grantor should not be the trustee, as this would create estate inclusion problems through possession of incidents of ownership over the policy. Typically, the grantor gifts money to the trust annually, and the trustee uses these contributions to pay the policy premiums.

Because the trust is irrevocable, the grantor gives up control over the policy. They cannot change beneficiaries, borrow against cash value, or surrender the policy. This permanent relinquishment of control is precisely what removes the policy from the taxable estate.

One critical timing issue: if the insured transfers an existing policy to an ILIT and dies within three years, the full death benefit is pulled back into the estate. The safest approach is for the ILIT to purchase a new policy from inception. The insured never owns the policy, so the three-year rule doesn’t apply. For clients with existing policies, the transfer still makes sense if life expectancy exceeds three years, but the risk must be acknowledged.

A technical detail: contributions to the ILIT for premium payments are gifts. To qualify for the annual gift tax exclusion, gifts must be present interest gifts. Crummey powers solve this. Each beneficiary receives a written notice that they have the right to withdraw their share of any contribution for a limited window, typically 30 to 60 days. If they don’t exercise this right, the contribution stays in the trust. In practice, beneficiaries virtually never exercise these rights because doing so would defeat the estate planning purpose. The result: contributions qualify as present interest gifts, but funds remain in the trust for premiums.

Clients with substantial wealth sometimes structure ILITs to last for multiple generations. The life insurance proceeds fund a trust that benefits children, grandchildren, and more remote descendants. When structured properly, these dynasty ILITs can pass wealth through generations with minimal estate and generation-skipping transfer tax.

Special Needs Trusts: Protecting Disabled Beneficiaries Without Disqualifying Benefits

Families with disabled beneficiaries face a cruel planning dilemma. Government benefits like Supplemental Security Income and Medicaid have strict asset limits. The federal SSI resource limit for an individual is $2,000 ($3,000 for couples), a figure unchanged since 1989. A direct inheritance can disqualify a disabled person from benefits they depend on for housing, medical care, and daily needs.

Special needs trusts solve this problem. The trust holds assets for the disabled beneficiary’s benefit without counting as an available resource for benefits eligibility purposes.

The distinction between third-party and first-party special needs trusts is fundamental. Third-party SNTs are created and funded by someone other than the beneficiary, typically parents or grandparents. Because the disabled person never owned the assets, they are not counted as the beneficiary’s resources. When the beneficiary dies, remaining trust assets pass to whoever the grantor designated, often other family members. No payback to Medicaid is required.

First-party SNTs are funded with the disabled person’s own assets, such as an inheritance received outright or a personal injury settlement. These trusts preserve benefits eligibility but come with a significant catch: when the beneficiary dies, Medicaid must be reimbursed for benefits paid during the beneficiary’s lifetime before any remaining assets pass to other beneficiaries.

Since 2016, ABLE accounts (Achieving a Better Life Experience, formally the Stephen Beck, Jr., Achieving a Better Life Experience Act) offer a simpler alternative for modest amounts. Disabled individuals can accumulate assets up to certain limits without affecting benefits eligibility. The annual contribution limit for 2026 is $20,000. ABLE accounts are easier to establish than SNTs and don’t require trustee management. However, ABLE accounts have annual contribution caps and state-specific lifetime account balance caps (ranging from approximately $235,000 to over $675,000 depending on the state, with caps changing periodically as states adjust their 529 plan limits). For families planning to leave substantial assets to a disabled beneficiary, SNTs remain essential because ABLE accounts are designed for more modest accumulations. In 2026, the ABLE Age Adjustment Act expanded eligibility from disability onset before age 26 to before age 46, significantly broadening the planning population.

Special needs planning requires specialist expertise. An attorney who understands the intersection of trust law, tax law, and government benefits programs is essential. Your role as financial advisor includes identifying clients who have or may have disabled family members who could receive inheritances. Ensure that beneficiary designations, wills, and trusts don’t accidentally leave assets directly to someone who depends on means-tested benefits. Connect clients with qualified special needs planning attorneys.

Advanced Planning Trusts: Recognition and Referral

Several trust structures exist primarily for estate tax reduction. These trusts are complex, require careful drafting, and demand ongoing compliance. Your role is recognition and referral, not implementation.

Spousal Lifetime Access Trusts allow one spouse to create an irrevocable trust for the other spouse’s benefit while removing assets from both spouses’ estates. Before the federal exemption became permanent, SLATs were urgently recommended to lock in high exemptions. With the exemption now permanent and substantial, the tax urgency has diminished for most families. SLATs remain useful for families with estates meaningfully above exemption levels, state estate tax planning, or situations where future appreciation could push estates above exemption.

Grantor Retained Annuity Trusts allow the grantor to transfer assets to an irrevocable trust while retaining an annuity payment for a term of years. If the trust assets grow faster than the IRS assumed rate, the excess passes to beneficiaries gift-tax-free. GRATs work best with assets expected to appreciate significantly.

Qualified Personal Residence Trusts remove a personal residence from the taxable estate while allowing the grantor to continue living there for a term of years. After the term ends, the grantor must pay fair market rent. These are most relevant for clients whose homes represent a significant portion of an above-exemption estate.

Intentionally Defective Grantor Trusts are structured so the grantor pays income tax on trust earnings while assets are excluded from the estate. The grantor’s payment of income taxes is an additional wealth transfer without gift tax consequences. This technique remains powerful for clients who want to transfer appreciation out of their estates.

Charitable Remainder Trusts and Charitable Lead Trusts address clients with substantial assets and charitable intent. A Charitable Remainder Trust allows a grantor to transfer appreciated assets to the trust, receive income for life or a term of years, and pass the remaining principal to charity. The grantor receives an immediate income tax deduction for the present value of the charity’s eventual interest. More importantly, the trust sells appreciated assets without triggering capital gains tax, making it ideal for concentrated positions. A Charitable Lead Trust inverts this arrangement: the designated charity receives income first, and the remainder passes to family members at significantly reduced transfer tax cost. Both structures require substantial assets and genuine charitable commitment, and both demand specialized drafting.

When a client’s estate exceeds federal or state exemption levels, when a specific asset has substantial appreciation potential, when a client expresses strong interest in transferring wealth to future generations, or when asset protection is a primary concern, refer clients to estate planning specialists. Your job is to recognize these triggers and facilitate the right connections.

When Trust Planning Breaks Down

Trust planning fails most often from poor funding. A revocable living trust that doesn’t own the client’s actual assets accomplishes nothing. If a client creates a trust but leaves accounts titled in their individual name, those assets still go through probate. Unfunded trusts are among the most common causes of estate plan failures.

The second failure point is outdated trusts. A trust created 20 years ago might not reflect today’s family situation. Tax laws have changed. The client’s net worth may have grown substantially. Children may have divorced or faced health crises. Disabled grandchildren may have become beneficiaries. A trust written in 2004 isn’t equipped to handle today’s reality.

ILITs and other irrevocable trusts become problematic when circumstances change and the grantor wants flexibility. An ILIT that made sense when the client had substantial taxable estate exposure may not make sense now if the exemption is permanent and high. Irrevocable trusts are tools for specific problems. When the problem changes, the tools that solved it yesterday may hinder flexibility today.

Modern trust law has provided partial relief from irrevocable trust rigidity. Trust decanting, now available in a majority of states, allows a trustee to transfer assets from one irrevocable trust into a new trust with updated terms, effectively modernizing a structure that became outdated. Courts can also modify irrevocable trusts when circumstances change in ways the grantor could not have anticipated at the time of creation. These remedies require attorney involvement and carry limitations, but they have softened what was once an absolute rule: irrevocable trusts are no longer unchangeable in all circumstances.

Advanced planning trusts require ongoing compliance. GRATs must produce the right annuity payments. Dynasty ILITs must stay within generation-skipping transfer tax exemptions. The planning fails if the ongoing compliance work gets neglected.

State-level estate and inheritance taxes demand closer attention in today’s environment. Twelve states plus the District of Columbia impose their own estate taxes, with exemptions far below the federal threshold. Oregon’s estate tax begins at $1 million, creating significant planning concerns even for clients below federal exemption levels. Five states impose inheritance taxes at the state level (Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania). For clients in these states, trust planning for state tax purposes remains essential and relevant, regardless of federal exemption permanence. A client with a $3 million estate in a state with a $1 million exemption faces real state tax exposure that makes trust structures valuable tools, even when federal taxes are not a concern.

In Practice: What This Looks Like

A 58-year-old client with a $4 million estate, married for 10 years, with two children from the first marriage and one from the current marriage, asks: "Do I need a trust?"

Start with what the client wants to accomplish. "Let’s talk about what happens if you’re hospitalized tomorrow and can’t make decisions for three months. How would your family access your accounts?" Most clients haven’t thought through incapacity. That alone makes a case for an RLT.

Next: "If something happens to you, how do you want things to work for your wife and your kids? You’re concerned about taking care of her, but you also want to make sure your two kids from your first marriage get their share eventually, right?" This client needs a QTIP trust, not an RLT. The QTIP solves the blended family problem.

For another client, 72 years old with an $8 million estate, heavy in life insurance: "Your insurance policy has a death benefit of $2.5 million. If you pass away, that becomes part of your taxable estate. At your current net worth, that pushes you above state exemption levels. Have you and your attorney considered whether moving the policy to a trust could help?" That’s the ILIT conversation.

For a client with a disabled adult child: "I want to make sure your daughter is taken care of after you’re gone. But if you leave her money directly, she loses her SSI benefits, and that’s where her medical care comes from. We should talk with an attorney about a special needs trust. It lets you provide for her without disqualifying her from benefits." This is the SNT conversation.

Each conversation flows from the client’s situation, not from trust types. Your job is to identify the problem, then connect it to the right tool.

Key Takeaways

- Most clients need only a revocable living trust. It solves probate and incapacity problems without requiring the grantor to give up control. For clients with straightforward situations and modest complexity, an RLT is sufficient.

- Marital trusts address blended family dynamics. When spouses have children from prior marriages, AB trusts and QTIP trusts ensure both spouses are provided for while protecting each spouse’s children’s inheritance. These structures require trade-offs around flexibility and trustee complexity.

- Irrevocable life insurance trusts remove death benefits from the taxable estate. For clients with substantial life insurance and taxable estate exposure, moving the policy to an ILIT prevents the death benefit from inflating the estate tax calculation. Remember the three-year rule for existing policies.

- Special needs trusts preserve government benefits eligibility. Families with disabled beneficiaries must structure inheritances carefully to avoid disqualifying the disabled person from SSI or Medicaid. Third-party SNTs funded by parents or grandparents avoid Medicaid payback requirements.

- Advanced planning trusts require specialist referral. SLATs, GRATs, QPRTs, and IDGTs serve specific high-net-worth situations. Your role is recognition (knowing when they might apply) and referral (connecting clients with estate planning specialists).

- The federal exemption environment has changed the planning conversation. With the exemption permanent and high, most clients won’t owe federal estate tax. Trust planning now emphasizes control, protection, privacy, and family coordination rather than tax reduction. State estate taxes remain relevant for some clients.

- Trust funding is non-negotiable. A trust that exists on paper but doesn’t own the client’s actual assets provides no benefit. Verify that the client’s accounts and property are properly titled in the trust’s name.

The Advisor’s Edge

This article demonstrates data any advisor can access: trust structures are defined by law, their mechanics are well-documented, and the planning logic is transparent. What makes the difference in practice is something much simpler than complex analysis. It’s asking the right questions. What does this client want to happen? Who needs protection? What problem are we solving?

The analytical skill that matters is matching. Can you hear a client describe their family situation and connect it to the right structure? Can you recognize when a client says "my attorney recommended a QTIP" and understand why that recommendation makes sense for a blended family, or push back if the situation doesn’t fit? Can you identify a client with life insurance, calculate the estate exposure, and know when an ILIT conversation is warranted?

These capabilities are exactly what the Certified Estate and Trust Specialist™ (CES™) program develops. The CES curriculum teaches you the mechanics of each trust structure, the trade-offs, and the applications. More importantly, it teaches you the questions to ask and the frameworks to use when clients describe their situations. It teaches you when to refer and when you have the foundation to advise independently.

The trusts will change. Tax law will change. But the core skill, understanding what clients want and matching them to the right structure, is timeless.

Sources and Notes: This article draws on established estate planning law and trust mechanics. Trusts are created under state law, and specific provisions vary by jurisdiction. For current federal exemption amounts and generation-skipping transfer tax thresholds, consult the Reference Atlas. Trust planning decisions should always be coordinated with qualified estate planning attorneys and tax professionals. This article is refreshed when federal exemption levels change or when significant tax law changes occur.