A client walks into your office worth $25 million. Their estate attorney mentions the federal estate tax exemption. The client feels relieved. No tax due, so the job is done.

Except it is not.

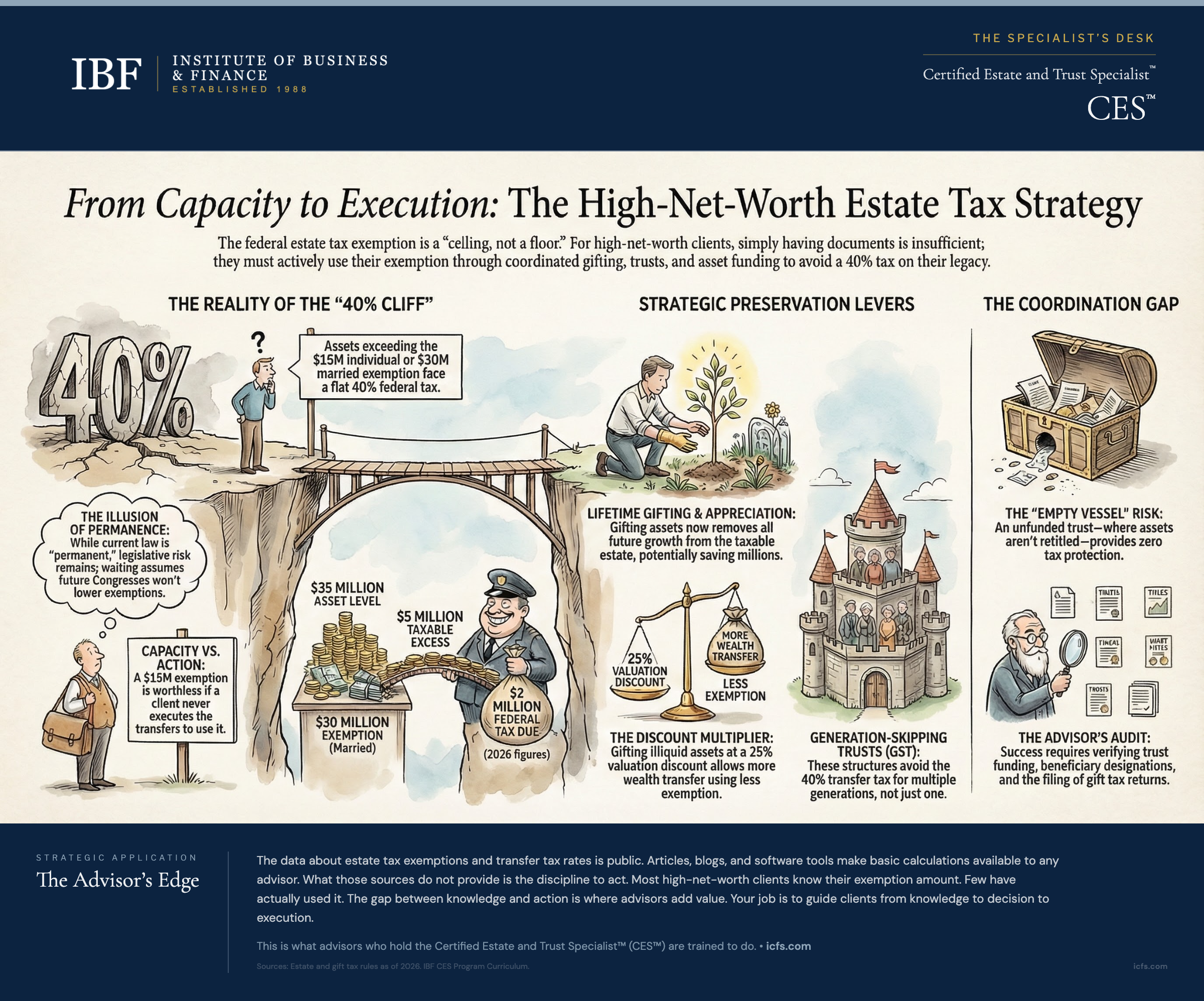

The exemption is a ceiling, not a floor. It creates capacity for tax-free transfer, but transfer requires action. A $15 million exemption becomes worthless if a client never uses it. Worse, exemption amounts are not guaranteed forever. Recent legislation made the current exemption permanent, but Congress could change the law in the future. Clients who assume today’s exemption will exist when they die are making an assumption about future legislation.

This is where estate tax strategy diverges from estate planning documents. The documents create structures. The strategy determines which structures matter, when to implement them, and how to coordinate them to minimize transfer tax while achieving your client’s real goals: smooth transfers to their chosen beneficiaries, family harmony, and business continuity.

The Estate Tax Reality for High-Net-Worth Clients

For clients above $7 million to $10 million in net worth, estate tax becomes a plausible outcome. For clients above $15 million, it is a legitimate planning consideration. For clients above $25 million, it is virtually certain without aggressive planning.

The math is straightforward. The federal exemption for 2026 stands at $15 million per individual or $30 million for a married couple. These amounts are indexed annually for inflation. The federal tax rate on amounts exceeding the exemption is 40 percent. So a client with $25 million in assets, married, has a $10 million taxable excess ($25M minus $30M exemption). Before any planning, that excess produces $4 million in federal estate tax alone.

Add state estate taxes to this picture, and the numbers become more severe. Twelve states plus Washington, D.C. impose their own estate taxes, and several others impose inheritance taxes on heirs. Many state exemptions fall far below federal thresholds. A client living in New York or Connecticut or Massachusetts faces additional tax exposure even if their federal taxable estate is zero.

For married couples, portability provides a baseline: when the first spouse dies, unused exemption transfers to the surviving spouse if the executor files Form 706, even when no tax is owed. This election is not automatic. Failing to file timely means unused exemption may be lost, though late-filing relief under Rev. Proc. 2022-32 is available for qualifying estates within five years of the decedent's date of death.

This is the threshold where clients stop asking “Do I need estate planning?” and start asking “How much tax do I owe?” The questions shift from probate avoidance to wealth preservation.

The Exemption Is Permanent, but Congress Can Change the Law

The permanence of current exemption amounts is law today. The One Big Beautiful Bill Act, enacted in 2025, made the exemption permanent with no sunset date or expiration. This represents a shift from previous uncertainty when exemptions were scheduled to expire.

But permanence is only as durable as legislation. A client at age 50 might safely assume the exemption will not substantially change before age 80 or 90. A client at age 70 has less runway. Congress could change the law. The question is not whether a statutory cliff exists, but whether political risk is real.

This creates a planning imperative: clients who use available exemption sooner rather than later lock in that decision. A $5 million gift executed at age 55 cannot be reversed by future legislation. Waiting assumes exemptions remain favorable when the client needs them most.

For a client with $20 million in assets and a married couple’s combined exemption of $30 million in 2026, exemption today is substantial. At higher exemption levels, the urgency to gift is lower. At lower exemption levels, the need for prior gifts becomes acute. This is why clients approaching age 70 should not defer planning assuming favorable exemption levels.

High-net-worth clients often assume they have years to implement planning. The legislative uncertainty around exemption levels should change that assumption. A client with $20 million at age 55 is not in crisis. But at age 65 or 70, when the timeline to use current exemptions is finite, the case for action becomes clear.

This is where strategy becomes operational: clients who recognize the exemption timeline can use their current exemption now through coordinated gifting and trust structures. Those who wait may find themselves under less favorable circumstances.

Lifetime Gifting: The Exemption in Motion

The estate tax exemption is a unified credit that covers both lifetime gifts and death transfers. A client who gives nothing away during life retains the full exemption to apply at death. A client who makes taxable gifts during life reduces the available exemption at death by the amount given.

This creates a strategic choice that high-net-worth clients must make deliberately: use the exemption now, through gifts, or preserve it for death, when transfers happen automatically.

The advantages of lifetime gifting are significant. First, gifts remove future appreciation from the taxable estate. A client at age 55 who gifts $2 million now removes not just $2 million but all future growth on that $2 million from transfer tax. Over 20 years, if the assets grow at 6 percent annually, that exemption used in a gift preserves $6.4 million in wealth compared to retaining the assets until death.

Second, gifts can be structured to multiply exemption value. The annual exclusion allows gifts of $19,000 per donor per recipient per year (2026 amount, indexed annually) without using any lifetime exemption. A married couple with five children can transfer $190,000 per year ($19,000 times five recipients times both spouses) completely tax-free and exemption-free. Over 15 years, that represents $2.85 million transferred without touching lifetime exemption capacity.

Third, gifts can leverage valuation discounts for business interests, real estate, and partnership stakes. A client may own a real estate portfolio or business interest worth $5 million. Gifting that interest at a 25 percent discount (for lack of control, lack of marketability, and other factors recognized in tax law) means the taxable gift is $3.75 million, not $5 million. The client has transferred $5 million of wealth but only consumed $3.75 million of exemption. The 25 percent difference stays in the family tax-free.

Trust Structures: Multiplication Without Accumulation

Gifts alone accomplish much. Gifts combined with trust structures accomplish more.

A straightforward gift from parent to adult child transfers wealth and uses exemption. An irrevocable trust created for the benefit of children and grandchildren transfers the same amount of wealth while:

First, removing all future growth from the taxable estate of the grantor. The parent contributes $2 million to an irrevocable trust. The trust owns investment assets. Over 20 years, those assets grow to $8 million. The original grantor’s estate includes nothing. The appreciation occurred outside the estate.

Second, providing control and management beyond the grantor’s lifetime. A gift to an adult child is done. An irrevocable trust can specify distributions over decades, provide for management by corporate trustees if individual trustees are inappropriate, protect assets from creditors and divorce claims, and ensure funds benefit grandchildren and subsequent generations.

Third, enabling generation-skipping transfer tax planning for families with substantial wealth. The generation-skipping transfer tax (GST) is a supplemental tax that applies when wealth passes to generation-skipping beneficiaries (typically grandchildren or more distant descendants) in ways that would otherwise avoid estate tax at the intermediate generation. The GST exemption equals the estate tax exemption ($15 million per individual in 2026), though unlike the estate tax exemption, the GST exemption is not portable between spouses. Each individual must allocate their own GST exemption or it is lost. A client with wealth destined for grandchildren can allocate GST exemption to an irrevocable trust, locking in tax-free transfer to multiple generations. The 40 percent transfer tax is avoided not just once but twice, three times, or more as successive generations inherit and pass wealth forward.

For clients with family net worth in the $50 million to $500 million range, generation-skipping trusts are among the most valuable planning tools available. A $10 million trust leveraging both estate tax and GST exemptions can grow to approximately $160 million over 50 years (at 5.7 percent annual real returns, a long-term stock market approximation) with zero transfer tax.

The most common structures for this purpose include Grantor Retained Annuity Trusts (GRATs), which transfer appreciation above an IRS assumed rate to beneficiaries tax-free; Spousal Lifetime Access Trusts (SLATs), which remove assets from both spouses’ estates while preserving indirect access; and Intentionally Defective Grantor Trusts (IDGTs), where the grantor pays income tax on trust earnings while the assets grow outside the estate. Each structure involves different trade-offs in terms of control, risk, and complexity. Charitable Remainder Trusts and Charitable Lead Trusts serve clients with philanthropic goals by combining estate tax reduction with income tax benefits, though the principal ultimately passes to charity (CRT) or generates a charitable income stream before reaching heirs (CLT).

Coordination: Where Plans Fail

Estate tax strategy fails not in the conception but in the execution. Documents are drafted. Trusts are created. The plan sits in a folder.

Then a client dies. The estate is discovered to be $35 million. The attorney is called. The question is urgent: “Did the client fund the trust?”

Funding a trust means retitling assets so the trust owns them. An unfunded trust is an empty vessel. It controls nothing. Assets titled in the client’s name alone pass through probate or by beneficiary designation, completely outside the trust, defeating the entire purpose.

This is where the coordination fails. An attorney drafts a $2 million irrevocable gifting trust. The client signs it. The attorney hands over a funding list with 10 items. The client intends to fund the trust but gets busy. The exemption gets used for nothing. The client dies. The $2 million is still in their personal account. It flows through probate and into their taxable estate, creating the very tax exposure the trust was designed to prevent.

Your role as quarterback includes verification. After documents are signed, you verify:

- Is the trust funded? (assets retitled to the trust’s name)

- Are beneficiary designations updated? (to avoid naming the client’s estate, forcing assets through probate)

- Is the corporate trustee in place and ready to act? (if the trust requires professional management)

- Are gift tax returns filed? (if required, to lock in the exemption allocation)

These are not glamorous tasks. They do not appear in the estate plan document. They are checklists and phone calls. They are also the difference between plans that work and plans that fail.

The Limitation: Legislative Risk and Planning Uncertainty

Estate tax strategy for high-net-worth clients operates under a shadow: legislative risk.

The current exemption is permanent law. It is also law that can be changed by Congress. A client at age 50 might safely assume the exemption will not substantially change before age 80 or 90. A client at age 70 has less runway.

This creates a structural problem. Clients want certainty. Tax law provides none. The best planning responds to this uncertainty by: (1) using available exemption sooner rather than later, when the timeline is long and risk is high, and (2) structuring plans to function under both high and low exemption scenarios.

A client who gives away $5 million at age 55 under a $15 million exemption has taken concrete action. Even if Congress changes exemption amounts in the future, that $5 million gift happened. It used exemption when exemption was available. A future change does not undo it.

A client who waits, assuming the exemption will always be $15 million, may find that assumption wrong. At age 80, under different exemption levels, regret is expensive but irreversible.

The other limitation is family dynamics. Estate tax planning often requires clients to make difficult decisions about wealth distribution during lifetime. A $3 million gift to an adult child is generous. It is also final. A client who makes such a gift and later has family conflict, estrangement, or changed circumstances cannot undo the gift or reclaim the exemption. Irrevocable means irrevocable.

A third limitation is over-transferring. A client who moves $10 million into irrevocable trusts to reduce estate taxes, then faces unexpected medical costs or a business downturn, may find themselves unable to access assets they need. The high permanent exemption actually reduces the urgency of aggressive transfers, giving advisors room to recommend more conservative approaches. Additionally, strategies involving illiquid assets (GRATs, IDGTs, family partnerships) depend on valuations the IRS can challenge. Aggressive valuations attract audit attention, and a successful IRS challenge can result in retroactive gift taxes or reduced planning effectiveness. State estate taxes compound the problem. Twelve states plus DC impose their own estate taxes with exemptions far below the federal $15 million; Oregon starts at $1 million. A client who owes nothing federally may face a meaningful state estate tax bill.

This is why discovery and goals conversations must precede planning implementation. Clients who fully understand the trade-offs, the permanence of irrevocable decisions, and the true costs of tax avoidance are better equipped to make informed choices.

Client Conversation: The Tax Question in Context

The client asks: “How much estate tax will I owe?”

The answer is usually: “Maybe nothing, if we plan.”

This opens the conversation but often closes client understanding. Clients want a dollar figure. Tax strategy requires talking about behavior, timing, and trade-offs.

Here is how the conversation might proceed:

“Your current exemption covers your first $15 million if you’re single, or $30 million if you’re married. That exemption is permanent under current law, but Congress could change tax law in the future. Your estate is currently around $25 million. Without any planning, your heirs might owe roughly $4 million in federal estate tax in a scenario where the exemption is lower or you’ve made significant additional gifts. In a high-exemption scenario, you owe nothing. The risk is whether you want to rely on exemptions remaining at their current level.”

The client’s next question is usually: “What’s my option?”

“We have several. First, we could use your current exemption through strategic gifts during your lifetime. This locks in the exemption as it exists today and removes future appreciation from your estate. Those gifts can be structured through trusts that provide management and control well after you’re gone. Second, we could coordinate your beneficiary designations so assets transfer efficiently outside probate and feed the right trusts at the right time. Third, we could evaluate whether business interests, real estate, or other illiquid assets qualify for valuation discounts that reduce the taxable value of gifts. Each approach has different trade-offs in terms of control, family dynamics, and flexibility.”

The client usually pauses here. The idea of giving away money, even if it’s tax-free and even if it’s to family, feels foreign to many wealthy clients.

“The way I think about it,” you can offer, “is that your exemption is an asset with finite value and uncertain longevity. You can use it now, deliberately and thoughtfully, to transfer wealth to your chosen beneficiaries under your terms. Or you can leave it unused, hope Congress keeps exemptions high, and deal with transfer tax consequences if that hope is wrong. The question isn’t ‘Do I have to give away money?’ The question is ‘Do I want to control how my wealth transfers, or do I want to let circumstance and tax law decide?’”

This conversation reframes planning from tax avoidance to wealth transfer control. Most clients understand that frame.

Key Takeaways

- Calculate realistic estate tax exposure now, not after death. Use current exemption amounts and your state’s estate tax rules to determine whether transfer tax is relevant to your situation. For married clients, model scenarios where exemptions are higher and lower. For single clients, consider both the current exemption and lower exemption amounts as planning anchors.

- Recognize that Congress can change exemption amounts. Current law sets the exemption at $15 million per individual, with no sunset date. That is not the same as permanence in a political sense. Clients approaching age 70 should not defer planning assuming favorable exemption levels will remain unchanged indefinitely. Build plans that work under multiple exemption scenarios.

- Layer gifting, trusts, and beneficiary designations into a coordinated plan. Annual exclusion gifts work alongside lifetime exemption gifts. Irrevocable trusts remove appreciation from your estate while providing management and control. Beneficiary designations coordinate with trust structures to route assets efficiently. One element in isolation accomplishes little. The same elements coordinated accomplish substantial wealth preservation.

- Fund trusts completely and verify funding status. An unfunded trust is theater. After irrevocable trusts are created and signed, verify that assets are actually retitled into the trust’s name. This requires ongoing attention and coordination with custodians, real estate title companies, and corporate trustees.

- Use valuation discounts for concentrated or illiquid assets. Business interests, real estate, partnership stakes, and other assets often qualify for valuation discounts for lack of control (DLOC), lack of marketability (DLOM), and other factors recognized in tax law. These discounts are applied sequentially rather than additively, and combined discounts commonly range from 25 to 45 percent depending on the asset and circumstances. This multiplies exemption value. An asset with a 25 percent discount means the same amount of wealth transfers for 75 percent of exemption cost.

- Lock in exemption allocation through gift tax returns before circumstances change. Filing a gift tax return allocates exemption to specific gifts. Once filed and the statute of limitations expires, that allocation is locked in. Clients should not assume allocation can wait indefinitely. Life changes, health changes, law changes. Lock in allocation while you can.

The Advisor’s Edge

The data about estate tax exemptions and transfer tax rates is public. Articles, blogs, and software tools make basic calculations available to any advisor. What those sources do not provide is the discipline to act.

Most high-net-worth clients know their exemption amount. Few have actually used it. The gap between knowledge and action is where advisors add value.

This gap exists because planning requires decisions. Which assets to gift? When? To whom? Through which structures? What if circumstances change? What if family relationships shift? Clients with $20 million in wealth do not make $2 million decisions lightly. They hesitate. They want certainty. Tax and estate planning provides none. It provides options and trade-offs instead.

Your job is to guide clients from knowledge to decision to execution. This is what advisors who hold the Certified Estate and Trust Specialist™ (CES™) designation are trained to do. The designation recognizes the ability to identify estate tax exposure, understand the mechanics of transfer tax law, coordinate beneficiary designations and documents, and serve as quarterback for implementation. The technical knowledge is necessary. The discipline to follow through is what actually preserves wealth.

Sources and Notes: This article synthesizes estate and gift tax rules as of 2026. Federal exemption amounts are indexed annually for inflation. State estate tax laws vary significantly; consult the Reference Atlas for state-specific rules. This article is refreshed annually to reflect exemption adjustments and legislative changes.