Opening Insight

When a 62-year-old client asks, “Should I claim Social Security now or wait?,” they are not really asking a question. They are asking for permission to feel confident about whatever choice they make. Your job is to show them the full landscape of options, walk them through the break-even points, and help them articulate the factors that matter most to their specific life.

The mechanics are not complicated. Claim at 62 and lock in a smaller monthly check. Claim at Full Retirement Age (67 for most clients) and get 100% of the calculated benefit. Claim at 70 and receive 124% of that benefit. The range is wide: the difference between the lowest and highest possible benefit is 54 percentage points, which means the decision carries real financial weight.

But mechanics do not drive client decisions. Life circumstances do. A client in excellent health with $2 million in savings faces an entirely different calculus than a client with chronic conditions and $150,000 in assets. A single person optimizes for their own longevity. A married couple must consider survivor benefits, which changes the strategy entirely.

Core Analysis: The Claiming Decision Framework

Full Retirement Age as the Reference Point

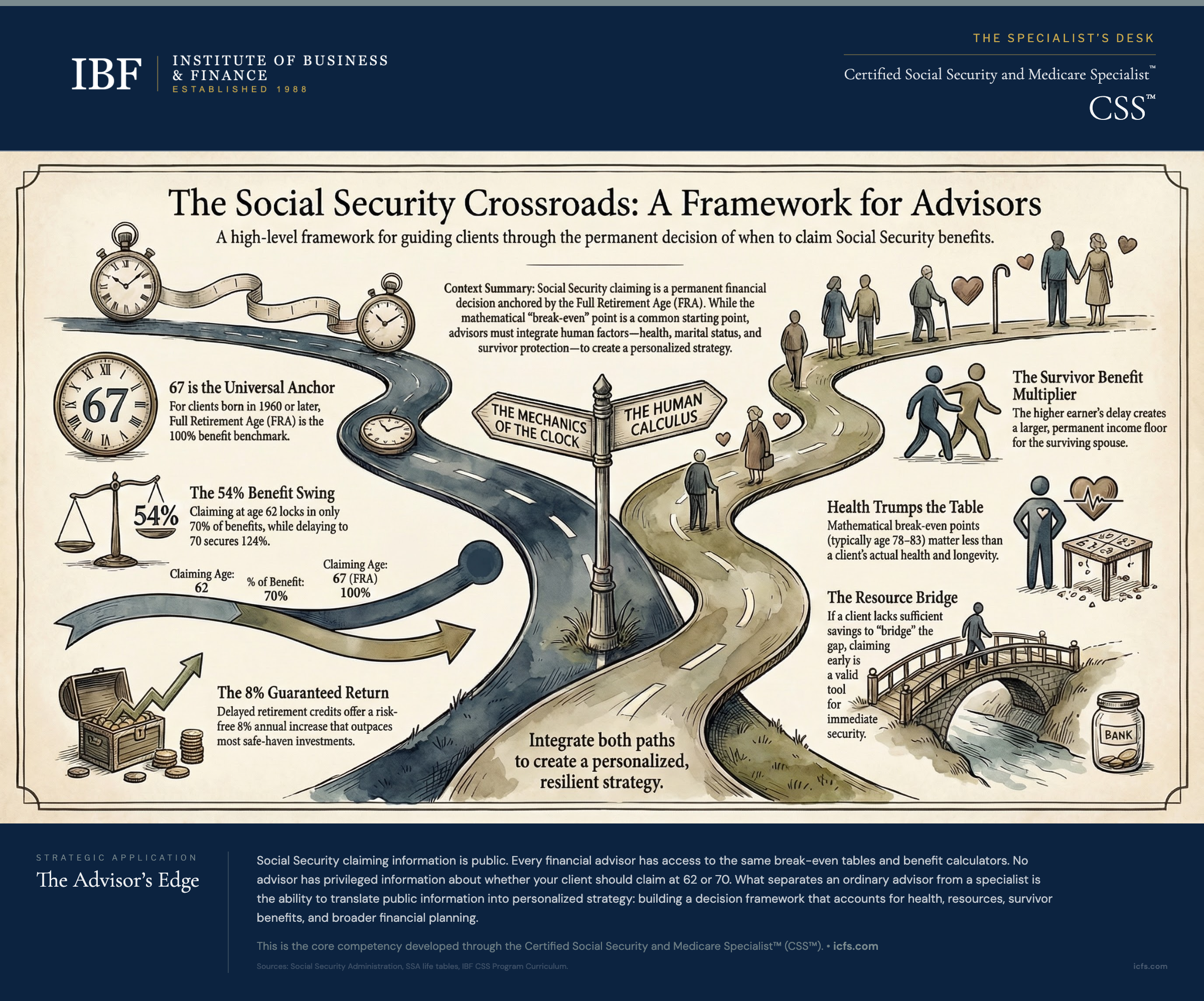

Full Retirement Age (FRA) is the age at which a client receives 100% of their Primary Insurance Amount (PIA). For anyone born in 1960 or later, FRA is 67. This is your benchmark.

Everything else moves up or down from this reference point. Claim before 67 and the benefit shrinks. Claim after 67 and it grows. The schedule is fixed and permanent. It is not like claiming early and “catching up” later.

The specific reduction for early claiming follows a mathematical formula. For a client with FRA of 67, claiming at 62 means claiming 60 months early. The first 36 months are reduced at 5/9 of 1% per month (about 6.67% per year), yielding a 20% reduction. The remaining 24 months are reduced at 5/12 of 1% per month (about 5% per year), yielding another 10% reduction. Total: 30% permanent reduction.

| Claiming Age | Reduction | % of PIA |

|---|---|---|

| 62 | 30% | 70% |

| 63 | 25% | 75% |

| 64 | 20% | 80% |

| 65 | 13.3% | 86.7% |

| 66 | 6.7% | 93.3% |

| 67 (FRA) | 0% | 100% |

| 68 | +8% | 108% |

| 69 | +16% | 116% |

| 70 | +24% | 124% |

A client earning $2,400 per month at FRA receives $1,680 at 62 and $2,976 at 70. The annual difference is $15,552 ($1,296/month × 12), or about $389,000 over 25 years of cumulative additional benefits for the delayed claimer.

Delayed Retirement Credits and the Power of Waiting

If a client delays past FRA, they earn delayed retirement credits (DRCs). The credit rate is 8% per year. This guaranteed permanent increase, when applied to the benefit that results from delayed claiming (including the DRC-enhanced base), receives the same annual cost-of-living adjustments (COLA) as all Social Security benefits, meaning the purchasing power is protected for life.

This matters because 8% compares favorably to what most clients can earn on safe, fixed-income investments. A client who says, “But I can invest the money and earn more,” is conflating average historical returns with guaranteed personal returns. The 8% from Social Security delay has no market risk, no sequence-of-returns vulnerability, and no longevity risk. It pays for as long as the client lives.

Credits accumulate monthly from FRA to age 70. After 70, they stop accruing. There is no advantage to delaying past 70, so advisors should always recommend claiming by 70 at the latest.

Break-Even Analysis: The First Layer

Break-even analysis asks a straightforward question: at what age will the cumulative benefits from delayed claiming exceed the cumulative benefits from early claiming?

Example: A client comparing claiming at 62 versus 67.

If they claim at 62, they receive $1,680/month for 60 months before a delayed claimer starts receiving benefits at 67. That totals $100,800 in early benefits.

At 67, the delayed claimer receives $2,400/month, compared to the early claimer’s $1,680. That is a $720/month advantage.

Break-even point: $100,800 divided by $720/month equals 140 months, or about 11 years and 8 months.

So the break-even age is roughly 78 years and 8 months. If your client expects to live past 79, waiting until 67 produces more cumulative lifetime benefits.

The same analysis for claiming at 62 versus 70 produces a break-even point around age 80-81. For claiming at 67 versus 70, around age 82-83.

But here is the trap in using break-even as a decision rule: it assumes the only thing that matters is total cumulative dollars. For many clients, that is wrong.

What Break-Even Analysis Misses

A single-person break-even calculation ignores several crucial factors.

Time value of money. A dollar received today is worth more than a dollar received five years from now. If a client invests early benefits, the time value of money shifts break-even later. A client who can effectively invest and compound benefits may rationally prefer early claiming, even if it does not maximize cumulative lifetime dollars.

Survivor benefits. For married clients, the break-even calculus is entirely different. When one spouse dies, the survivor receives the higher of their own benefit or 100% of the deceased spouse’s benefit, subject to the widow(er)’s limit if the deceased claimed before Full Retirement Age. A higher earner who delays creates a larger survivor benefit for the remaining spouse. This survivor protection is not captured in individual break-even analysis.

Tax implications. Higher Social Security benefits may push income into higher brackets, affecting the taxation of benefits, portfolio withdrawal strategies, and overall after-tax household income. A client delaying Social Security while drawing down an IRA may face different tax outcomes than a client claiming early and preserving IRA assets.

Cash flow needs. Some clients simply need the money now. Medical bills, housing costs, or family support create immediate income requirements that waiting does not address. Social Security exists to provide income security. If a client needs income, they should claim.

Health status. Break-even analysis assumes average life expectancy. For a client with metastatic cancer or serious chronic conditions, the calculus changes completely. If they are unlikely to reach the break-even age, early claiming maximizes the benefits they will actually receive.

Single Filers: The Longevity Bet

For a single person, the claiming decision is fundamentally a bet on longevity. Claim early and win if you die young. Delay and win if you live long.

The decision framework for single filers has three layers.

First, assess longevity. What does the client know about their likely lifespan? Current health conditions? Family history? Lifestyle factors like smoking or exercise? A client with parents who both lived past 95 faces a different calculation than a client with a terminal diagnosis. Use life expectancy data as a starting point (a 67-year-old man has a median survival age around 84; a 67-year-old woman has a median survival age around 87), but acknowledge individual variation.

Second, assess resources. Can the client afford to delay? Do they have pension income, substantial retirement savings, or continued employment income? A client with $2 million and no pension can easily bridge the gap from 62 to 70. A client with $150,000 in savings and no pension cannot.

Third, assess preferences. Some clients value certainty: they want money in hand now. Others value optimization: they want to maximize lifetime benefits. Neither preference is wrong. Your job is to ensure the client understands the trade-offs and chooses consciously.

The starting recommendation for single filers with above-average longevity and sufficient resources: delay as long as possible. For single filers with health concerns or limited resources: consider claiming earlier, perhaps around 64-66, as a balance between need and optimization.

Married Couples: The Survivor Benefit Changes Everything

When one spouse dies, the surviving spouse receives the higher of their own benefit or the deceased spouse’s benefit, subject to the widow(er)’s limit if the deceased claimed before Full Retirement Age. This calculation inverts the decision-making framework.

Consider a couple where the higher earner (PIA $3,000) and lower earner (PIA $1,200) are both 62.

If the higher earner claims at 62, their benefit is $2,100 per month (70% of PIA). Under the Widow(er)’s Limit Provision (RIB-LIM), the surviving spouse’s benefit would be the greater of: what the deceased was receiving ($2,100), or 82.5% of the deceased’s PIA ($2,475). The survivor receives $2,475 at their own Full Retirement Age.

If the higher earner delays to 70, their benefit is $3,720 per month (124% of PIA). If they die, the surviving spouse receives $3,720 at their own Full Retirement Age (no RIB-LIM cap applies because the deceased had already reached FRA when claiming).

The difference is $1,245 per month for the surviving spouse’s remaining life. If the survivor lives another 15 years as a widow, that difference is approximately $224,100 in additional lifetime benefits.

This is why the coordinated couple strategy typically favors the higher earner delaying to 70 while the lower earner claims earlier based on household cash flow needs.

If the couple can fund retirement from other sources (savings, pensions, continued employment), both can delay. If they need income, the lower earner claims at 62 while the higher earner delays. The lower earner’s benefit provides cash flow during the delay period. At the survivor stage, the lower earner’s benefit becomes irrelevant because the higher earner’s larger benefit replaces it.

Women statistically outlive men by about five years. Among married couples both aged 65, roughly two-thirds of the time the wife will be the surviving spouse. This makes protecting the survivor benefit (usually by having the higher earner delay) particularly important for household longevity risk.

Limitation: When This Framework Breaks Down

This framework assumes clients can articulate their longevity expectations and their resource situation with enough clarity to make a decision. In practice, several scenarios complicate the analysis.

Health transitions. A client in good health at 62 may receive a serious diagnosis at 65. A client with chronic conditions may stabilize unexpectedly. Life expectancy is not fixed; it shifts. Some advisors recommend building in trigger points: if health circumstances change materially, revisit the claiming decision.

Asset depletion. A client with sufficient resources to delay may face unexpected expenses: medical bills, a nursing home, supporting a grandchild. If delaying requires depleting savings unsustainably, early claiming may preserve overall financial security. This requires ongoing monitoring, not a one-time decision.

Divorce. A client in a second marriage may have different survival benefit concerns than in their first marriage. Divorced benefits are themselves a complex topic (eligible if the marriage lasted 10 years, the ex is at least 62, the client is unmarried, and the client has been divorced for at least 2 continuous years, unless the ex-spouse has already filed). Claiming strategy in a remarriage requires different thinking than for a first-marriage couple.

Required Minimum Distributions and taxation. For a client with a large traditional IRA, the interaction between RMDs, Social Security taxation, and portfolio withdrawals creates a complex optimization problem. Early Social Security claiming may push income into higher brackets. Late claiming may allow Roth conversions during a low-income window. The tax tail can wag the claiming dog.

Market conditions. A client whose portfolio lost 30% right before they wanted to claim may face a different cash flow situation than expected. The portfolio withdrawal strategy and the claiming strategy must interact. This is why Social Security claiming cannot be analyzed in isolation.

Client Conversation: Translating Numbers into Decisions

When a client asks, “When should I claim?,” start with their Social Security statement. Pull up the benefit estimates at ages 62, FRA, and 70. Show the numerical range.

Then ask questions in this sequence:

“What is your health like right now? Do you have any serious conditions, or is your family history on the early side or the late side?” Listen more than you talk. A client who says, “My mother and father both died before 75” has given you crucial information. A client who says, “My parents lived past 95, and I am healthy,” has given you different information.

“Do you need the money now, or can you bridge the gap to 70 without Social Security?” A client who says, “I have to claim at 62 or I will struggle with mortgage and healthcare” has answered the question. A client who says, “I have a pension and some savings, so I could wait,” has given you flexibility.

For married couples, ask: “Are you both planning to retire at the same time, or at different times? And if one of you were to pass away, what would the survivor need to live on?”

Then walk through the scenarios. Show the break-even table. Explain that the break-even is not destiny; it is just information. Show what the survivor benefit would be under different claiming combinations.

Finally, ask: “Of the options we have looked at, which feels right to you? And why?”

The conversation should produce a decision that the client can defend, not a recommendation that you impose.

Key Takeaways

- Full Retirement Age is the benchmark, not the recommendation. For clients born after 1960, FRA is 67. Benefits at 62 are 30% lower; benefits at 70 are 24% higher. The decision is not where to claim, but how to think about the trade-offs.

- Break-even analysis is a starting point, not an ending point. The break-even age (roughly 78-79 for claiming at 62 vs. 67) informs the conversation but does not determine the answer. Health, resources, survivor considerations, and tax implications all factor into the real decision.

- For single filers, the decision is fundamentally about longevity and resources. Clients with above-average longevity expectations and sufficient bridge resources should generally delay. Clients with health concerns or limited resources may claim earlier without guilt.

- For married couples, the higher earner’s decision drives the survivor benefit. The higher earner should generally delay to 70 to maximize the survivor benefit that protects the lower earner. The lower earner’s claiming age depends on household cash flow needs.

- Claiming strategy is not independent of broader financial planning. Portfolio withdrawal sequencing, Roth conversion opportunities, pension timing, tax planning, and healthcare coverage all interact with the Social Security claiming decision. Optimal strategy requires analyzing the full financial picture.

- The delayed retirement credit (8% per year) is a feature, not a bug. Frame delayed claiming as earning 8% guaranteed, with annual COLA adjustments, survivor protection, and longevity protection. DRCs enhance survivor benefits but do not increase spousal benefits, which are capped at 50% of the retired worker’s PIA regardless of delay. No investment in the client’s portfolio can match this combination.

The Advisor’s Edge

Social Security claiming information is public. Every financial advisor has access to the same break-even tables and benefit calculators. The Social Security Administration publishes the rules, the formulas, and the life expectancy data. No advisor has privileged information about whether your client should claim at 62 or 70.

What separates an ordinary advisor from a CSS™ specialist is the ability to translate public information into personalized strategy. A CSS™ specialist can walk a client through the claiming options in language that illuminates rather than confuses. They can build a decision framework that accounts for health, resources, survivor benefits, and broader financial planning. They can ask the right questions to surface what matters most to the client.

This is the core competency of financial advising in Social Security planning. Not knowing a rule that the client cannot look up themselves, but knowing how to apply the rules to the client’s specific life.

Certified Social Security and Medicare Specialists™ spend the designated curriculum exploring these claiming scenarios in depth: single filers at various health and resource levels, married couples with different earnings patterns, divorced beneficiaries, longevity risk, survivor protection, and integration with broader retirement planning. The destination of this training is the ability to conduct these conversations with confidence and precision.

The next layer of Social Security planning is Medicare enrollment and IRMAA planning. These decisions happen in parallel with Social Security claiming and interact with it in subtle but important ways. See Medicare Enrollment and IRMAA for a framework on navigating that choice.

Sources and Notes: Information reflects current Social Security law and regulations as of 2026. Break-even ages and benefit examples are illustrative and based on FRA of 67 and average life expectancy data from SSA life tables. Actual claiming decisions require analysis of individual Social Security statements and personal circumstances. This article is refreshed annually.