The Medicare Enrollment Stakes

Your client turns 65 and decides to delay Medicare enrollment. Three years later, they change their mind. What happens next is not good.

They face a permanent 20% increase in Part B premiums. Add Part D late enrollment penalties, and the cost compounds. Over a 25-year retirement, missing the Initial Enrollment Period by a few months can cost tens of thousands of dollars in extra premiums. The penalties never expire.

This is where the CSS designation adds the most direct value. Social Security has flexibility. Clients can claim at 62, wait until 70, or anywhere in between. Medicare does not work that way. Medicare operates on rigid enrollment windows. Miss the deadline, and you pay forever.

The second layer of complexity sits in IRMAA. Higher-income clients face surcharges on both Part B and Part D premiums based on income from two years prior. This two-year lookback creates a planning window if you know how to use it.

This article walks you through both layers: the enrollment periods themselves and the income management strategies that reduce IRMAA exposure without sacrificing retirement security.

The Initial Enrollment Period: Your Client’s Primary Window

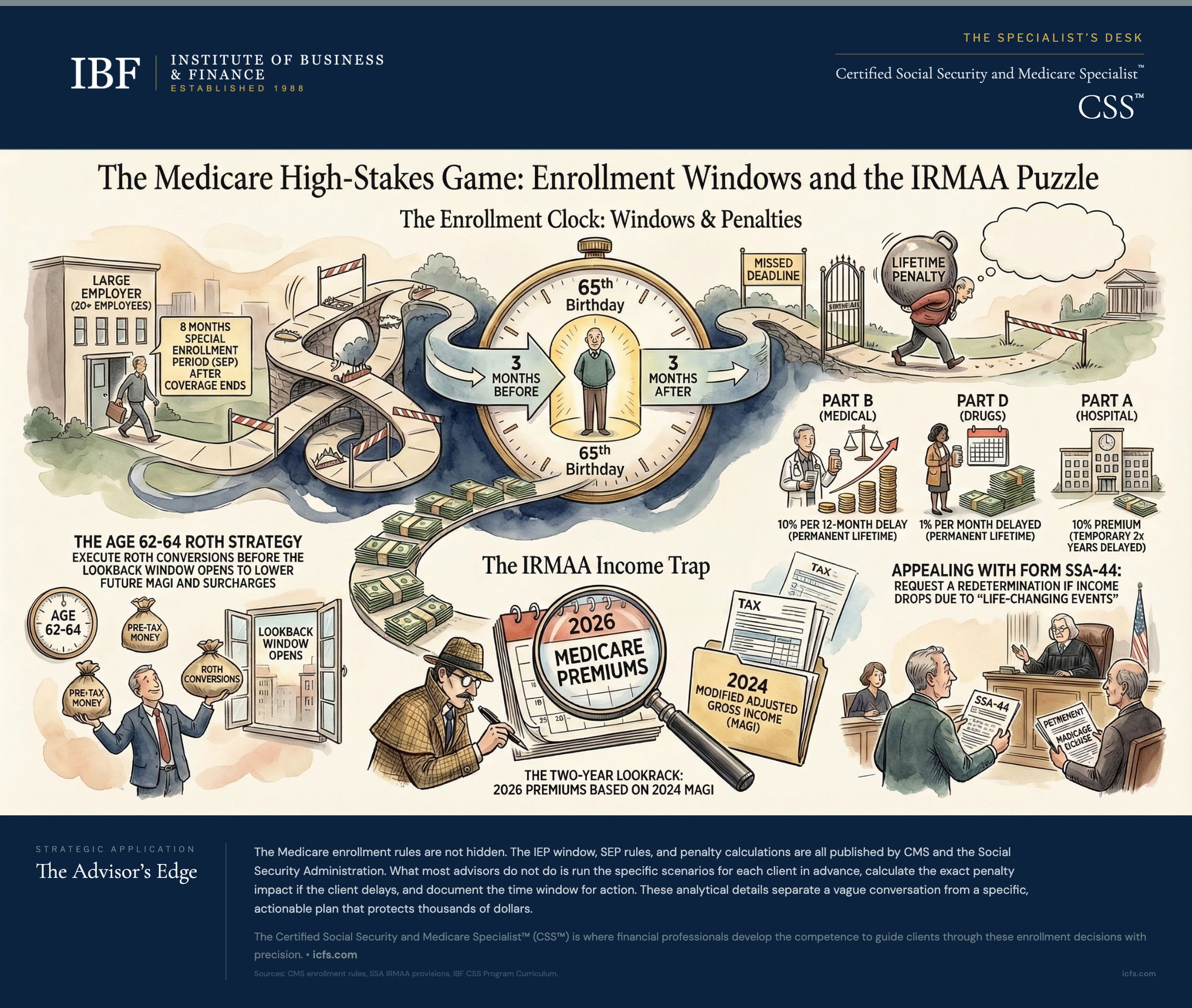

The Initial Enrollment Period spans seven months, centered on your client’s 65th birthday. It runs from three months before their birthday month, includes the birthday month, and extends three months after.

Margaret turns 65 on June 15. Her IEP runs March 1 through September 30. Robert turns 65 on April 1 (first of month), so his IEP begins February 1 and ends August 31. For first-of-month birthday clients, enrolling in the three months before their IEP means coverage begins one month earlier, the first of the month preceding their birthday month.

The specific enrollment month matters because it determines when coverage begins:

- Enroll during the three months before the birthday month: coverage starts the first day of the birthday month (no gap)

- Enroll during the birthday month or the three months after: coverage starts the first of the following month (creates a gap). The later in the IEP you enroll, the longer the gap, up to four months if you wait until the last month of your IEP.

Patricia turns 65 in June. If she enrolls in March, April, or May, her Medicare coverage begins June 1. If she waits until June, coverage starts July 1, creating a one-month gap. Waiting until August means coverage starts September 1, a three-month gap.

This timing matters most for clients without other health coverage. Those with employer coverage may tolerate the gap. Those retiring at 65 with no employer plan cannot.

Automatic vs. Voluntary Enrollment

Clients already receiving Social Security benefits are automatically enrolled in Medicare Parts A and B. Their Medicare card arrives about three months before their 65th birthday with no action required.

This automatic enrollment creates a critical decision point. If a client has employer coverage and wants to delay Part B, they must actively decline it. Inaction means enrollment and premium deductions from Social Security. This matters especially for clients with qualifying employer group health coverage (through their own or a spouse’s employment with 20+ employees).

Clients not yet receiving Social Security must actively apply for Medicare. They can apply online at ssa.gov, visit a Social Security office, or call 1-800-772-1213. Advise them to apply during the three months before their birthday month to ensure coverage starts at 65.

This distinction between automatic and voluntary enrollment is where many clients stumble. A client pursuing delayed Social Security claiming (to maximize benefits at 70) may not realize that Medicare requires separate action. They assume “Medicare will take care of itself” when Social Security is claimed later. It does not work that way. Medicare eligibility and Social Security claiming are linked administratively but separable in timing.

When Employer Coverage Changes the Rules

Clients with active group health insurance through current employment (their own or their spouse’s) can delay Medicare enrollment without permanent penalties, but only if three conditions are met:

- The employer has 20 or more employees

- The coverage is through current employment (not COBRA, retiree coverage, or former employer benefits)

- They enroll in Medicare within eight months of the coverage ending

This Special Enrollment Period is the most important exception to the penalty rules you will encounter with working clients.

Consider a client who works until age 68. Their employer has 150 employees. They have group health coverage. They can skip the IEP at 65 without penalty. When they retire at 68, their eight-month SEP clock begins the month their employer coverage ends. They can enroll in Medicare anytime during that eight-month window without facing late enrollment penalties.

The employer size matters. If the employer has fewer than 20 employees, Medicare becomes primary at 65 regardless of coverage. The client should enroll during their IEP to avoid complications.

Documentation matters too. When clients eventually enroll after delaying, CMS will ask for employment verification: employer name, address, employment dates, health plan dates, and contact information. Advise clients to gather this documentation before leaving employment. HR departments respond faster to current employees.

The General Enrollment Period Safety Net (and Its Costs)

Clients who miss their IEP can still enroll during the General Enrollment Period, which runs January 1 through March 31 each year. Coverage begins the first day of the month after enrollment. This timing reflects a 2023 rule change; previously, GEP enrollees waited until July 1 for coverage to begin.

But the GEP comes with a cost. These clients face late enrollment penalties for every month they delayed beyond their IEP.

The math is straightforward. Part B penalties equal 10% of the standard premium for each full 12-month period delayed. A client who turned 65 in October, missed their IEP (which ended in January), and did not enroll until the following January has delayed 12 months. Their Part B premium increases by 10%, permanently.

The Part A penalty (10% of premium, applied for twice the number of years delayed) is temporary. Part B and Part D penalties are permanent.

The timing creates a compounding problem. A client who turned 65 in October and misses the IEP cannot enroll until January at earliest. Coverage then begins February 1, creating approximately a four-month gap from their 65th birthday. They face penalties for the entire delay, even though the GEP shortens their gap.

Part D Penalties: Calculated Differently, Equally Permanent

Part D (prescription drug) enrollment follows similar logic but uses a different calculation. The penalty equals 1% of the national base beneficiary premium for each full month of delay without creditable coverage. For 2026, the national base beneficiary premium is $38.99 per month. This base premium is recalculated annually, so penalty dollar amounts change each year.

A client who delayed 18 months without prescription drug coverage faces an 18% permanent surcharge on whatever Part D plan they choose. In 2026, that would be approximately $7.02 per month ($38.99 × 18%) added to their Part D premium for life.

Creditable coverage matters. If a client had prescription drug coverage through their employer, TRICARE, VA benefits, or certain other programs, they can delay Part D enrollment without penalty. When that coverage ends, they have 63 days to enroll in Part D without triggering the penalty.

Many clients do not know whether their employer coverage qualifies as creditable. Employers must provide annual notices stating creditable status. Instruct clients to keep these notices. They are proof that delay was permissible if questions arise later.

The surprise for many clients: employer coverage ends, they assume it transitions automatically, and they do not realize a gap exists. When they eventually enroll, they discover they owe years of penalty surcharges. This is one of the most common sources of preventable cost in Medicare.

The Annual Election Period and Coverage Changes

Existing beneficiaries face a different enrollment window each year. The Open Enrollment Period runs October 15 through December 7. During this time, beneficiaries can:

- Switch from Original Medicare to Medicare Advantage

- Switch from Medicare Advantage to Original Medicare

- Change from one Medicare Advantage plan to another

- Change Part D plans

Changes take effect January 1. A beneficiary who changes plans in November still has about six weeks before the change takes effect, allowing time to get their affairs in order.

Separate from the OEP, Medicare Advantage enrollees have the Medicare Advantage Open Enrollment Period from January 1 through March 31. During this window, those already in Medicare Advantage can switch to a different MA plan or return to Original Medicare.

Use this annual window in your client relationships. Schedule Medicare reviews in September, before the October OEP begins. This allows time to analyze options, compare plans, and make deliberate decisions instead of rushing in early December.

Managing IRMAA: The Income Timing Game

Income-Related Monthly Adjustment Amounts apply a surcharge to both Part B and Part D premiums for beneficiaries with income above certain thresholds. The critical detail: IRMAA uses a two-year lookback on Modified Adjusted Gross Income (MAGI).

Premiums in 2026 are based on MAGI from 2024. A client retiring in 2026 will pay IRMAA surcharges based on income from when they were working. This timing mismatch catches many new retirees by surprise.

For 2026, the standard monthly Part B premium is $202.90. IRMAA begins when individuals exceed $109,000 MAGI (or $218,000 for married filing jointly), with surcharges ranging from $81.20 to $487.00 per month depending on income tier and whether the beneficiary has Part D.

But the two-year lookback also creates a planning window. Clients can manage their MAGI in years that will affect their future Medicare premiums.

Roth Conversions Before the Lookback Window Opens

Consider a client age 62 who plans to retire at 65. They have a $1.2 million traditional IRA. Without planning, their retirement MAGI will trigger IRMAA surcharges.

Between ages 62-64, while still working, they execute systematic Roth conversions. They convert $150,000 per year, paying taxes at their current marginal rate. By age 65, they have shifted $450,000 to the Roth.

In retirement, their required IRA withdrawals are smaller (the IRA balance is smaller). Roth distributions do not count toward MAGI. Their combined income may now stay below the first IRMAA threshold. The result: they save thousands of dollars per year in premium surcharges over their Medicare years.

Life-Changing Events and IRMAA Appeals

The two-year lookback is not absolute. Clients who experience certain life-changing events can request IRMAA redetermination using Form SSA-44. Qualifying events include:

- Marriage, divorce, or death of a spouse (can increase or decrease IRMAA depending on combined income)

- Work stoppage or significant work reduction

- Loss of income-producing property (disaster, fraud). Note: voluntary sale or transfer of income-producing property does not qualify. The loss must be involuntary and beyond the client’s control.

- Loss of pension income

- Employer settlement payment received due to an employer’s bankruptcy, closure, or reorganization

This is particularly valuable for new retirees whose current-year income is dramatically lower than the lookback year. A client who retired in January 2026 may receive an IRMAA surcharge based on their 2024 working income. But they can request redetermination based on their reduced 2026 income.

The process requires documentation of both the life event and the income change. Flag this opportunity for any client whose circumstances have changed significantly.

IRMAA Planning Intersects with Tax Planning

IRMAA thresholds do not align with federal tax brackets. A client might have room in the 22% tax bracket but find that filling it triggers the next IRMAA tier. The incremental cost of IRMAA may exceed the tax benefit of the additional income recognition.

When doing tax projection work for Medicare-enrolled clients, add a row for IRMAA impact. The true marginal rate on additional income includes not just federal and state taxes but also potential IRMAA surcharges.

Coordinating Medicare Enrollment with Social Security Decisions

This is where the CSS designation’s value becomes clear. Social Security and Medicare are administratively linked but strategically separable.

Clients receiving Social Security at 65 are automatically enrolled in Medicare Parts A and B. Clients who delay Social Security must separately apply for Medicare if they want coverage at 65.

Scenario 1: Claiming Social Security Before 65

The client is already receiving Social Security when they turn 65. Medicare is automatic. The only decision: does employer coverage warrant declining Part B? If yes, they must return a declination form. Inaction means enrollment.

Scenario 2: Delaying Social Security, Enrolling in Medicare at 65

The client wants maximum benefits from delayed claiming but also wants Medicare coverage starting at 65. They must apply for Medicare separately through ssa.gov or a Social Security office. They select Medicare enrollment without Social Security. Part B premiums are paid directly (not deducted from a Social Security check that does not exist yet).

This dual timing is counterintuitive but powerful. A client can claim Social Security at 70 while having had Medicare coverage for five years.

Scenario 3: Delaying Both Past 65

With qualifying employer coverage, clients can delay both Medicare and Social Security past 65. When they eventually retire, they have eight months to enroll in Medicare penalty-free and the option to claim Social Security with delayed retirement credits.

The Client Conversation: When to Bring Up Medicare

Most of your clients turn 65 thinking about Social Security. Medicare feels like a separate issue. Your job is to connect them.

Start this conversation at age 62. At that point, your client is likely thinking about Social Security anyway. Raise Medicare timing alongside Social Security strategy. “We are looking at when to claim Social Security. Medicare works on its own timeline. You cannot delay Medicare the way you can delay Social Security. Let’s look at both together.”

Run specific scenarios. “If you claim Social Security at 62, Medicare is automatic at 65. If you delay Social Security to 70, you need to separately apply for Medicare at 65. Here is the eight-month window if you are working with employer coverage. Here is the penalty math if you miss the enrollment deadline.”

For clients with employer coverage, the conversation is different. “You can stay on the employer plan past 65 without Medicare penalty, but you have an eight-month window after your coverage ends. Let’s track those dates.”

Make it concrete. Create a simple timeline for each client. Mark the IEP dates (seven months around their 65th birthday). Mark the deadlines for claiming Social Security if they want to delay. Mark the eight-month SEP window if they have employer coverage. Make the abstract rules concrete.

Key Takeaways

- The Initial Enrollment Period is your primary window. Seven months around age 65, with the three months before the birthday month offering on-time coverage. Missing the IEP leads to permanent Part B penalties (10% per 12-month delay) and permanent Part D penalties (1% per month delay).

- Employer coverage changes the rules but requires action. Clients with group health coverage from employers with 20+ employees can delay Medicare enrollment without penalty, but they must enroll within eight months of coverage ending. Three conditions must be met: employer size, current employment (not COBRA), and timely action.

- Document employment dates before leaving the job. CMS will ask for employer name, address, employment dates, health plan dates, and contact information. HR departments are far more helpful to current employees than former ones.

- The two-year IRMAA lookback creates a planning window. Premiums in 2026 are based on 2024 income. Clients can manage MAGI through Roth conversions, income timing, and capital gain harvesting in years before the lookback window affects their Medicare premiums.

- Life-changing events reopen IRMAA calculations. Retirement, work reduction, marriage, divorce, and spouse death allow requesting IRMAA redetermination based on current income rather than the two-year lookback. Flag this opportunity for every client whose circumstances change significantly.

- Medicare timing and Social Security timing are linked but separable. Clients receiving Social Security are auto-enrolled in Medicare. Those delaying Social Security must separately apply for Medicare if they want coverage at 65. Both timelines can be optimized independently.

The Advisor’s Edge

The Medicare enrollment rules are not hidden. The IEP window, SEP rules, and penalty calculations are all published by CMS and the Social Security Administration. Any advisor with a calculator and a form can look up the timelines.

What most advisors do not do is run the specific scenarios for each client in advance, calculate the exact penalty impact if the client delays, and document the time window for action. These analytical details separate a vague “you should probably enroll” conversation from a specific, actionable plan that protects thousands of dollars.

The Certified Social Security and Medicare Specialist™ (CSS™) designation is where financial professionals develop the competence to guide clients through these enrollment decisions with precision, connecting Medicare timing to Social Security strategy in ways that serve clients on Monday morning.

For deeper analysis of managing Medicare costs throughout retirement, see Maximizing Social Security Benefits for Married Couples.

Sources and Notes: Medicare enrollment periods, penalty formulas, and IRMAA mechanics described in this article reflect current rules under the Centers for Medicare & Medicaid Services (CMS) and Social Security Administration (SSA) guidance as of 2026. Specific income thresholds, premium amounts, and penalty percentages are set annually. This article is refreshed annually.