Why Coordination Matters

Social Security was designed as a solo worker benefit. But the program extends to families, and the way those benefits interact creates both constraints and opportunities.

The Spousal Benefit Foundation

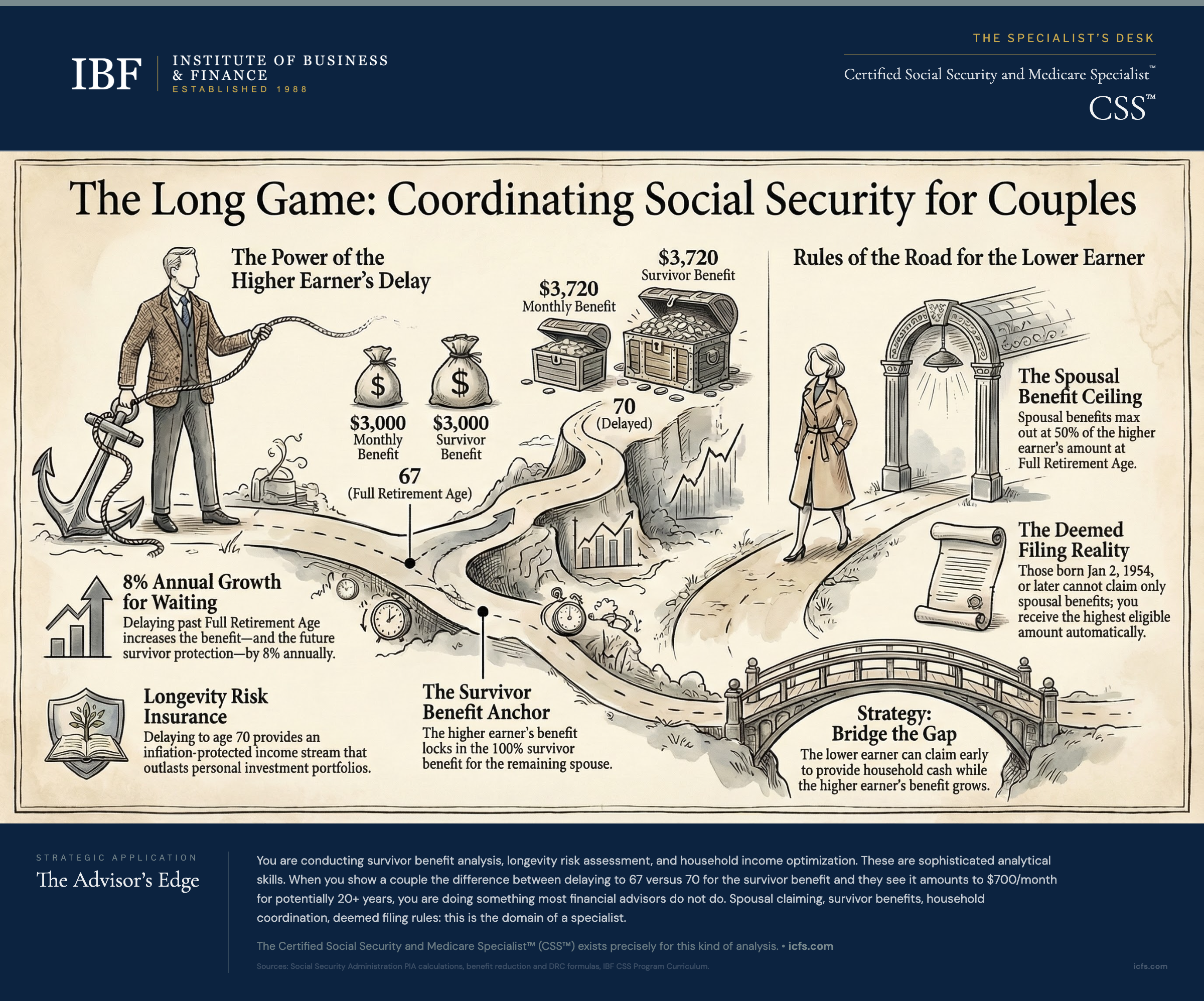

At Full Retirement Age, a spouse can receive up to 50% of the higher earner’s Primary Insurance Amount (PIA). This is the ceiling, not a floor, because 50% is the maximum spousal benefit. The actual amount received depends on when the spouse claims. Claiming at 62 (for those with a full retirement age of 67) reduces it to about 32.5% of the higher earner’s PIA. Waiting until FRA locks in the full 50%. But here is the critical point: spousal benefits do not grow beyond FRA. A spouse who waits until 70 gets the same 50% of the higher earner’s PIA as a spouse who claims at 67.

The spouse’s own retirement benefit, by contrast, grows 8% per year from FRA to 70. For some couples, the lower earner’s retirement benefit ends up higher than the spousal benefit, making their own benefit more valuable to pursue.

The rules that create this picture are the “deemed filing” rules established by the Bipartisan Budget Act of 2015. For anyone born January 2, 1954, or later, when you file for Social Security, you are automatically deemed to have filed for all benefits you are eligible for. You receive the higher amount. You cannot strategically claim one type of benefit while letting another grow.

The Survivor Benefit Amplifier

Survivor benefits operate on different math entirely. When a spouse dies, the surviving spouse receives up to 100% of what the deceased spouse was receiving (or would have received at the survivor’s own full retirement age), depending on the survivor’s own claiming age and the applicability of the RIB-LIM (Reduced Initial Benefit Limit) rule, which can apply when the deceased claimed early. If the deceased spouse delayed to 70 and earned 24% in delayed retirement credits, the survivor benefit includes those credits.

Consider a concrete scenario: Thomas has a PIA of $3,000, with a full retirement age of 67. If he claims at 67, his monthly benefit is $3,000. If his wife survives him, her survivor benefit maxes out at $3,000 per month (at her own full retirement age). Now suppose Thomas delays to 70. His benefit grows to $3,720 ($3,000 × 124%). If he dies, his widow receives $3,720 for the rest of her life. The difference: $720 per month, or $8,640 per year, or perhaps $150,000+ over the survivor’s remaining decades.

This is why delayed retirement credits matter so much in married couple planning. They are not just an individual benefit boost; they become a permanent protection for the surviving spouse.

Core Analysis: When and Why to Delay the Higher Earner

The strategic direction for most couples is clear: the higher earner should delay as long as possible, ideally to 70, while the lower earner’s claiming decision depends on the couple’s cash flow needs.

Why the Higher Earner Delays

Survivor Benefit Protection. The higher earner’s delay creates a larger survivor benefit. Women typically outlive men by approximately five years on average, and in most married couples, wives are younger than husbands. The surviving spouse will depend on the deceased spouse’s Social Security to fund decades of retirement. A higher earner who delays to 70 is, in effect, purchasing a larger inflation-protected annuity for the spouse who may survive for 15, 20, or 25 more years.

Household Income Maximization. While the higher earner is delaying, the lower earner can claim. This provides income during the delay period. The household does not starve while waiting for the higher earner’s benefit to grow. Instead, there are two sources of income: the lower earner’s Social Security (even if claimed early) plus portfolio withdrawals or other sources. The higher earner’s benefit eventually kicks in at a much higher level.

Longevity Risk Transfer. Delayed Social Security is longevity insurance. If the higher earner lives into their 80s or beyond, the monthly benefit continues at the maximum level forever, with annual cost-of-living adjustments. Portfolio withdrawals end when assets run out. Social Security does not. By delaying, the higher earner trades certain income now for uncertain (but potentially much longer) income later.

The Lower Earner’s Claiming Sequence

The lower earner’s decision is more nuanced and depends on household cash flow.

If bridge resources exist: Some couples have sufficient savings, pensions, or continued employment income to fund retirement from 62 to 70. Both can delay, maximizing both benefits. At 70, both spouses are receiving benefits; combined household income from Social Security alone might cover most or all expenses.

If cash flow is tight: The lower earner claims at 62, 63, or 64 based on financial need. A 62-year-old receives 70% of their PIA (for those with a full retirement age of 67). A 64-year-old receives 80% (for those with a full retirement age of 67). Both provide cash to the household while the higher earner’s benefit grows by 8% per year. This creates a staggered approach: income from the lower earner now, enhanced income from the higher earner later.

The Deemed Filing Reality

A lower earner born in 1954 or later cannot claim “just” a spousal benefit at FRA while letting their own retirement benefit grow to 70. Deemed filing prevents this. When the lower earner files, they are filing for both their retirement and spousal benefits. Social Security calculates both and pays the higher. Note that deemed filing does not apply to survivor benefits. A surviving spouse can still claim survivor benefits while allowing their own retirement benefit to continue growing.

For lower earners with modest earnings histories, waiting might not make much difference. Their own benefit might never exceed 50% of the higher earner’s PIA. In that case, claiming at 62 provides income for eight years with no long-term cost, because their household will be relying on the higher earner’s survivor benefit anyway once the higher earner dies.

Limitation: Where Coordination Strategies Fall Short

Married couple coordination strategies work well for those with clean benefit records and straightforward earnings histories. But several situations complicate the picture.

Divorced Spouses and Multiple Marriages. If one spouse was previously married for 10+ years, they might qualify for divorced spouse benefits. These benefits exist independently and do not reduce the other spouse’s benefits. But they add complexity to the claiming strategy.

Government Pension Offset and Windfall Elimination Provision. The Social Security Fairness Act, signed in January 2025, repealed both the GPO (Government Pension Offset) and the WEP (Windfall Elimination Provision) effective for benefits payable January 2024 onward. These provisions previously reduced benefits for individuals with government pensions from non-covered employment. The repeal is an immediate windfall for affected households, and advisors should revisit planning for clients with government pensions to ensure their benefits are calculated correctly under the new rules.

Same-Sex Marriage Recognition. All same-sex couples married on or after June 26, 2015, should have clean benefit records. Couples married before that date might need to verify their benefits account for the marriage.

Remarriage Rules and Long Survivor Periods. A surviving spouse who remarries at 60 or later does not lose eligibility for survivor benefits on the deceased spouse’s record. This creates a planning consideration for remarriage scenarios.

Client Conversation: How to Discuss Coordination

Walking a married couple through coordinated claiming requires a systematic approach.

Step 1: Gather the Data. Obtain Social Security benefit estimates for both spouses. You need both spouses’ numbers to do any meaningful comparison.

Step 2: Identify Who Is the Higher Earner. This is usually obvious from the PIA figures. The higher earner is the one with the larger PIA, which is the benefit at FRA.

Step 3: Show the Survivor Benefit Implications. Create a simple table showing what the survivor benefit would be at each claiming age. The survivor benefit is insurance for the survivor. $700⁄month for 20 years is $168,000. This framing helps couples take it seriously.

Step 4: Model Household Income Under Different Scenarios. Show what the couple’s combined Social Security looks like if both claim at 62, if the higher earner delays to 70 while the lower earner claims at 62, and if both delay. Show what happens to household income if the higher earner dies at 80.

Step 5: Stress the Survivor Scenario. Gently redirect focus: “This is also about what happens if one of you passes away. Statistically, wives outlive husbands by approximately five years on average. If you die at 80 and your spouse lives to 88, that is eight more years they are living on Social Security. The size of your benefit at that point matters enormously.”

Step 6: Identify the Bridging Period. If the higher earner is delaying, ask: “What income sources can you live on until [higher earner’s claiming age]?” If bridging is not feasible, adjust the strategy.

Step 7: Document the Decision. Record the strategy in your client file and summarize it in writing.

Key Takeaways

- The higher earner’s benefit becomes the survivor benefit. When one spouse dies, the survivor receives 100% of the deceased spouse’s benefit. The higher earner’s claiming decision determines this survivor benefit. Delaying to 70 permanently increases survivor protection.

- Deemed filing closes off old strategies. For anyone born January 2, 1954, or later, you cannot claim only spousal benefits at FRA while letting your own benefit grow. Deemed filing means you are filing for both benefits simultaneously.

- Most couples under-delay. Analysis by United Income found that only 4% of retirees in their study actually claimed at age 70, the age that would have been optimal for 57% of them. The remaining couples claim too early, often leaving significant survivor benefit protection on the table.

- Bridge resources make delay feasible. Couples with pensions, substantial savings, or continued employment income can afford to delay the higher earner to 70. Couples with limited resources might delay to FRA instead.

- Age gaps matter. When spouses are significantly different ages, the strategy adjusts. Very large age gaps might make full delay impractical.

- Divorced spouses, government pensions, and remarriage complicate the picture. Couples with prior marriages, non-covered government pensions, or remarriage plans need additional layers of analysis.

The Advisor’s Edge

Most couples think of Social Security as “their benefits,” personal financial assets. In reality, the benefit structure and claiming rules are public knowledge, auditable through official Social Security publications. Your role is to read and apply the publicly available information, positioning you as a guide to the official rules.

You are conducting survivor benefit analysis, longevity risk assessment, and household income optimization. These are sophisticated analytical skills. When you show a couple the difference between delaying to 67 versus 70 for the survivor benefit (and they see that it amounts to $700⁄month for potentially 20+ years), you are doing something most financial advisors do not do.

The Certified Social Security and Medicare Specialist™ credential exists precisely for this kind of analysis. Spousal claiming, survivor benefits, household coordination, deemed filing rules. These are CSS™ domain. Position yourself as a CSS™ to distinguish yourself from advisors who treat Social Security as a rounding error.

Integrate Social Security claiming timing with portfolio withdrawal sequencing, Roth conversions, pension timing, and healthcare coverage. The couple who delays Social Security can execute large Roth conversions during the delay period at lower tax brackets. Frame Social Security as one component of integrated retirement income planning, and show how coordination across multiple income sources amplifies the benefit.

Sources and Notes: Analysis based on Social Security Administration Primary Insurance Amount calculations, benefit reduction and delayed retirement credit formulas from the Social Security Act, and empirical longevity data. The Social Security Fairness Act repeal of the Government Pension Offset took effect January 5, 2025. This article is refreshed annually.