Your Client Bought Bitcoin in 2021 and Never Told Their CPA

Your client walks in with a spreadsheet. Over the past four years, they have traded Bitcoin, Ethereum, and a dozen other cryptocurrencies. Some trades were swaps on decentralized exchanges. Some were deposits into yield farming pools. Some were staking rewards that accumulated in their wallet.

They tell you: “I never sold for dollars, so I don’t think I owe taxes on any of this. And I definitely do not have forms for the IRS.”

This conversation is about to change. Next April, their exchange will file Form 1099-DA, the IRS’s new digital asset reporting requirement. The form will show gross proceeds. If your client’s tax return does not match, the IRS will send a CP2000 notice proposing additional tax, penalties, and interest.

Your role is not to become a tax preparer. Your role is to translate the tax fundamentals into a conversation that prepares your client for what comes next. This article covers what advisors need to know about digital asset taxation so you can identify compliance risks, help clients organize records, and build a bridge to their CPA.

The Property Classification Creates Everything

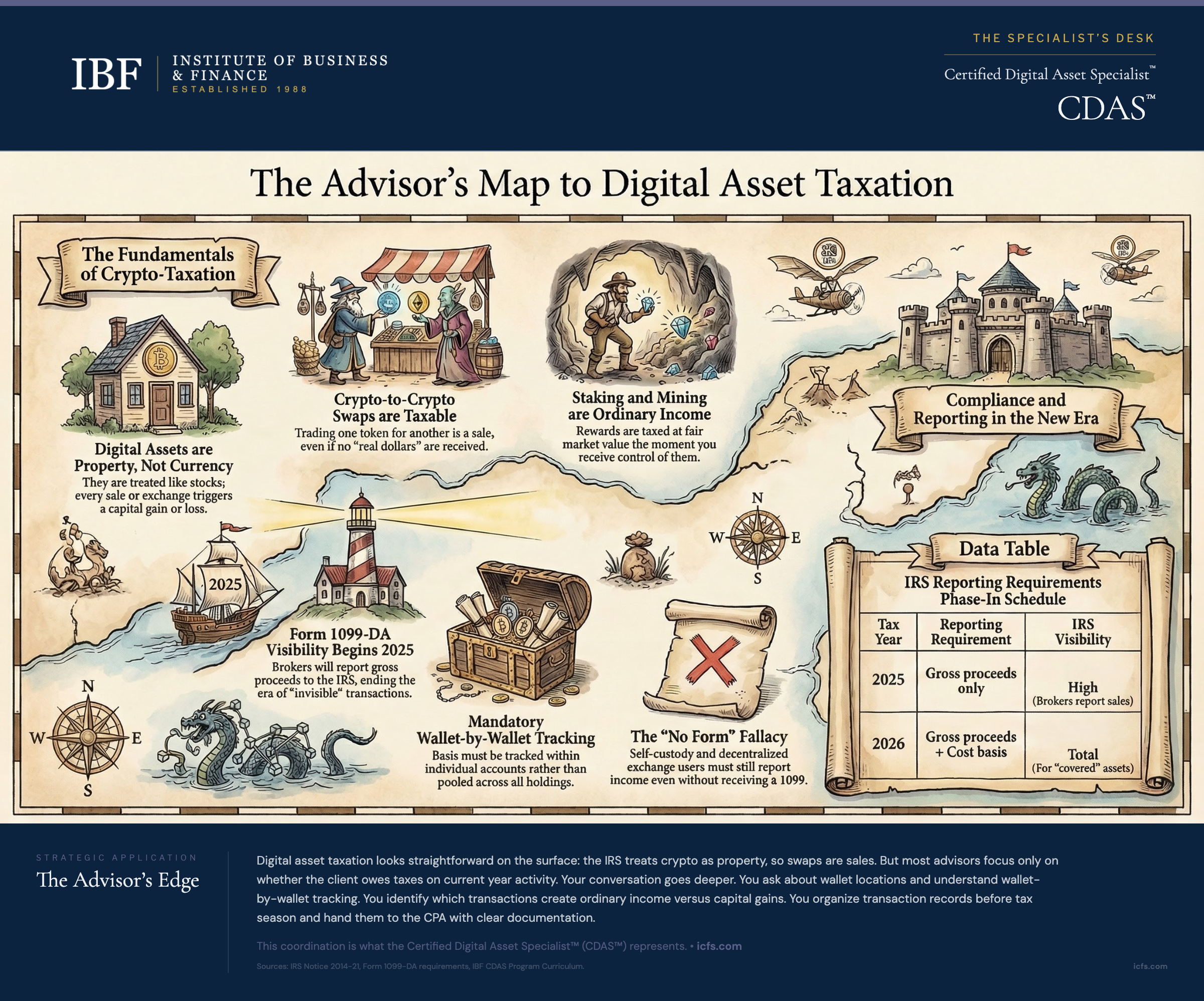

In March 2014, the IRS issued Notice 2014-21, establishing the foundational rule: virtual currency is property for federal tax purposes, not currency.

This classification seems simple but carries profound implications. When you buy and sell property, you have capital gains or losses. When you receive property as compensation, you have ordinary income equal to the property’s fair market value. When you exchange one property for another, you recognize gain or loss immediately.

The property classification means digital assets work like stocks or real estate. Moving dollars between bank accounts is not taxable. Moving Bitcoin from one exchange to another wallet you control is not taxable. But exchanging Bitcoin for Ethereum is a taxable event, just as exchanging shares of Apple for shares of Microsoft would be.

This distinction creates the most common compliance error. Clients believe that because they never sold for dollars, they have no tax obligation. In fact, every crypto-to-crypto swap is a sale triggering gain or loss recognition. A client who swapped Bitcoin for Ethereum a dozen times over the year has a dozen taxable events, even though they never received a single dollar.

The property classification also eliminated what some taxpayers tried in the early years. Before 2018, a few investors argued that swapping one cryptocurrency for another qualified as a like-kind exchange under Section 1031, deferring gain recognition. The Tax Cuts and Jobs Act closed that loophole by restricting like-kind treatment to real property only. Any crypto swap is now a taxable event.

Transactions That Trigger Tax: A Practical Map

Understanding which activities create tax obligations is essential for client conversations. Some transactions are clearly taxable. Others are not.

Sales for fiat currency are taxable. Selling Bitcoin for dollars, euros, or any government-issued currency creates a capital gain or loss. The calculation is straightforward: proceeds minus cost basis equals gain or loss.

Crypto-to-crypto exchanges are taxable. Swapping Bitcoin for Ethereum, trading Ethereum for Solana, or any exchange of one cryptocurrency for another triggers gain or loss recognition on the cryptocurrency disposed of. The amount realized equals the fair market value of what you received at the moment of exchange. The cost basis equals your original purchase price of the cryptocurrency given up.

Payment for goods or services is taxable. Using cryptocurrency to buy a car, pay a contractor, or purchase anything else is a disposition. You recognize gain or loss equal to the difference between the fair market value of what you received and your cost basis in the crypto spent. If you bought Bitcoin for $30,000 and used it to buy a car when Bitcoin traded at $65,000, you have a $35,000 gain.

Staking rewards and mining income are taxable as ordinary income. Under Revenue Ruling 2023-14, staking rewards are taxable at fair market value when you gain dominion and control over the tokens. Mining income follows the same rule: when you receive cryptocurrency as a block reward or transaction fee, you have ordinary income equal to the fair market value at that moment. This income is taxable when received, not when sold. The basis in the tokens equals the amount included in income, and your holding period begins the day after you gain dominion and control.

Airdrops and hard forks are generally taxable as ordinary income. When a blockchain hard fork creates a new cryptocurrency (like Bitcoin Cash forking from Bitcoin in 2017) and you receive it in your wallet, you have ordinary income at fair market value once you can access and dispose of the new tokens. Airdrops follow similar treatment. The key timing question is dominion and control: once you can withdraw, transfer, or sell the tokens, income is recognized.

Transactions that are not taxable include wallet-to-wallet transfers (moving cryptocurrency between your own wallets creates no tax event), purchasing cryptocurrency with fiat currency (you are simply acquiring property), and certain protocol upgrades. When a blockchain upgrades (like Ethereum’s merge from proof-of-work to proof-of-stake in 2022) and existing tokens continue without any swap, the upgrade is generally not taxable because the token is considered a continuation of the same property.

Form 1099-DA: The IRS Now Has Visibility

For years, digital asset transactions went largely unreported because brokers had no obligation to report them. That era is over.

Form 1099-DA, Digital Asset Proceeds from Broker Transactions, is the IRS’s information return for custodial brokers. Beginning with 2025 transactions (reported in 2026), major exchanges like Coinbase, Kraken, and Gemini must file this form with the IRS whenever they facilitate a digital asset sale. The form reports gross proceeds to both the IRS and the taxpayer, similar to how Form 1099-B reports stock sales.

The phase-in matters. For 2025 transactions, brokers must report gross proceeds but cost basis reporting is optional. The IRS will not impose penalties for good-faith compliance efforts. For 2026 transactions, both gross proceeds and cost basis are required for covered securities (digital assets acquired and held with the same broker on or after January 1, 2026).

For noncovered securities (acquired before 2026 or transferred in from another source), brokers will report gross proceeds but leave cost basis blank. Clients will need to determine their own basis from personal records. This matters because without documented basis, the IRS could treat basis as zero, making entire proceeds taxable.

When the IRS receives 1099-DA data that does not match a client’s return, it typically sends a CP2000 notice proposing additional tax. This is not an audit notice, but it requires a response within 30 days. If your client reported the transaction elsewhere or can document a loss, they can respond with evidence. If they failed to report, they need to file an amended return.

One phrase matters: “I never got a 1099-DA” is no longer a valid excuse for underreporting. Decentralized exchange users and self-custody investors will not receive 1099-DAs because those platforms are not custodial brokers. But the absence of a form does not eliminate the reporting obligation. The taxpayer is still responsible.

Cost Basis Methods: Choose Before the Sale

When clients dispose of digital assets acquired at different times and prices, the cost basis method they use determines the gain or loss. The four methods are FIFO, LIFO, HIFO, and Specific Identification.

FIFO (First-In, First-Out) assumes the oldest units are sold first. This is the default method if no specific identification is made. Amanda bought 0.5 Bitcoin for $20,000 in March 2024 and 0.3 Bitcoin for $16,500 in July 2024. In November 2025, when Bitcoin trades at $85,000, she sells 0.5 Bitcoin for $42,500. Under FIFO, the March purchase (oldest) is deemed sold first, creating a $22,500 gain on a $20,000 basis. The holding period exceeds one year, so the gain is long-term.

LIFO (Last-In, First-Out) assumes the most recently acquired units are sold first. Amanda’s sale of 0.5 Bitcoin would include the entire July purchase (0.3 BTC at $16,500) plus 0.2 BTC from the March purchase (0.2 BTC at $8,000). Total basis is $24,500. Gain is $18,000. Some units are short-term, some are long-term. LIFO often produces a lower total gain when prices have risen over time.

HIFO (Highest-In, First-Out) assumes the highest-cost units are sold first, minimizing the current gain. Amanda’s sale would include the July purchase (highest cost per unit at $55,000 per BTC) and some of the March purchase (lower cost). Total basis is the highest available, producing the lowest gain. Like LIFO, this often results in short-term treatment on more recent purchases.

Specific Identification allows Amanda to designate exactly which units are being sold. She could choose to sell only the March purchase (long-term gain) or combine it with the July purchase (mixed character). This provides maximum flexibility but requires documentation at or before the time of sale. The key timing rule is immutable: specific identification must be documented before the transaction executes. Retroactively deciding which lot to sell after viewing price movements is not permitted.

Which method is best depends on the client’s overall tax situation. A client in a high bracket may prefer the lower gain amount from HIFO even with short-term treatment. A client in a lower bracket may prefer long-term treatment from FIFO. The error is choosing after the fact or failing to document the method used.

Wallet-by-Wallet Accounting: The End of Universal Pooling

Before 2025, some taxpayers pooled all their digital assets across all wallets into a single cost basis pool, then applied FIFO globally. Revenue Procedure 2024-28 ended that approach.

Each wallet or exchange account is now a separate container for basis purposes. If your client holds Bitcoin on Coinbase, Bitcoin on Kraken, and Bitcoin in a hardware wallet, each location is tracked separately. When your client sells 0.5 Bitcoin from Kraken, the cost basis must come from units held in Kraken, not from cheaper units in a hardware wallet.

Marcus holds Bitcoin in three locations: Coinbase (0.8 BTC purchased at $30,000 each), Kraken (0.5 BTC purchased at $50,000 each), and a hardware wallet (1.0 BTC transferred from Coinbase). Under the old universal approach, if Marcus sold 0.5 BTC from Kraken, he could have used FIFO globally and assigned the $30,000 basis from his earliest purchase, creating a $15,000 long-term gain.

Under wallet-by-wallet tracking, the Kraken account is its own container. The only Bitcoin in Kraken was purchased at $50,000. That is the basis regardless of cheaper units elsewhere. The gain is $5,000 (0.5 BTC at $60,000 minus $50,000 basis). This creates lower gains in some scenarios and higher gains in others, depending on when purchases occurred in each location.

For clients who missed the deadline, Revenue Procedure 2024-28 provided a one-time safe harbor for allocations before January 1, 2025. Clients who did not complete a proper allocation must still transition to wallet-by-wallet tracking. Coordinating with their CPA to reconstruct the most defensible basis allocation based on available records is essential.

When clients transfer digital assets between wallets, the cost basis travels with the asset, but documentation is critical. Without records of the transfer date, amount, and basis of specific units transferred, the receiving wallet has no basis information. The default FIFO calculation may produce unexpected results.

Staking, Mining, and DeFi: When Income Hits Before Any Sale

Clients with staking and mining activity often do not realize they have ordinary income. This income is recognized when the rewards are credited to their wallet, not when they sell.

Robert stakes 32 Ethereum as a validator. Over the year, he earns 1.5 Ethereum in staking rewards. On December 31, when he can withdraw the rewards, Ethereum trades at $3,200. Robert has $4,800 of ordinary income (1.5 ETH multiplied by $3,200). His cost basis in the 1.5 ETH is $4,800. His holding period begins the day after he gains dominion and control.

The ordinary income character applies regardless of what Robert does next. If he sells the rewards immediately, he may have minimal additional gain or loss. If he holds for a year and sells at a higher price, the appreciation beyond $4,800 becomes long-term capital gain. If the rewards decline and he sells at a loss, the loss is capital and can offset capital gains.

Mining income follows the same principle. When a miner receives cryptocurrency as a block reward or transaction fee, they have ordinary income equal to fair market value at receipt. For miners who operate mining businesses, this income may also be subject to self-employment tax. The basis in the mined coins equals the fair market value at receipt.

DeFi creates tax situations that current guidance does not fully address. When clients deposit tokens into liquidity pools and receive LP tokens, the tax treatment is unclear. Some practitioners treat the deposit as non-taxable, while others argue it is a taxable exchange. When clients withdraw and receive different amounts due to impermanent loss, the analysis becomes complex. Liquidity fees and yield farming rewards are likely ordinary income, but the character of trading fee distributions through LP tokens remains debated.

For clients with significant DeFi activity, the conservative approach is to recommend they work with a crypto-specialized CPA. The guidance gaps create real risk. Your role is identifying that the activity may have tax consequences, not providing the definitive treatment.

Form 1040 Digital Asset Question: A Simple Yes-or-No With Big Implications

The IRS includes a digital asset question on every Form 1040. It asks whether the taxpayer, at any time during the year, received, sold, exchanged, or otherwise disposed of any digital asset.

A taxpayer who answers “No” when they should answer “Yes” has made a false statement on their tax return. The IRS uses this question to flag returns for examination.

The answer is “Yes” if your client sold any cryptocurrency, exchanged one cryptocurrency for another, received cryptocurrency as payment for goods or services, received cryptocurrency from staking or mining, or made any taxable disposition of a digital asset.

The answer is “No” only if they held cryptocurrency without any dispositions, transferred cryptocurrency between wallets they control, or purchased cryptocurrency with fiat currency.

The most common mistake is answering “No” after making crypto-to-crypto swaps. A client who traded Bitcoin for Ethereum should answer “Yes” even though they never sold for dollars. The question asks about exchanges, and a crypto-to-crypto swap is an exchange.

Open Questions and Uncertain Treatment

Wash sale rules currently do not apply to digital assets. Cryptocurrency is property, not a security, so the wash sale rules technically do not restrict a client from selling Bitcoin at a loss, immediately repurchasing, and claiming the loss. This creates a tax planning opportunity that does not exist for stocks.

However, Congress has proposed extending wash sale rules to digital assets multiple times. Pending legislation could make this treatment retroactively unavailable. The conservative approach is to document the client’s rationale and confirm the strategy with their CPA before implementing it.

De minimis exclusions do not exist for digital asset gains. A $5 gain from buying coffee with Bitcoin is technically reportable. This creates practical compliance challenges that have no clear solution. Some practitioners argue for a de minimis rule based on administrative burden, but no formal guidance supports ignoring small gains.

Specific identification requirements demand documentation at the time of sale. The IRS permits specific identification for cryptocurrency, allowing taxpayers to select which lots they are selling. But the identification must be documented at or before the time of sale. Retroactively designating lots is not permitted. For clients with multiple purchase lots, specific identification can materially reduce tax liability by selling highest-basis lots first.

Client Conversation: Translating Technical Rules Into Action

When a client mentions they have cryptocurrency, the conversation should move quickly to the practical tax questions.

If a client says they “moved some coins around,” ask: Did you exchange one cryptocurrency for another, or did you only transfer the same cryptocurrency between different accounts? Exchanging one crypto for another is a taxable event. Transferring between your own wallets is not.

If a client earned staking rewards, explain: Staking rewards are taxable as ordinary income when you receive them, based on fair market value at that time. It does not matter that you did not sell. Your CPA will need the value of those rewards when you received them.

If a client ignored an airdrop for years and then sold it, clarify: The timing of income is debated, but the safest approach is to treat airdrops as income when received. If you did not report it at that time, you may need to amend prior returns.

If a client provides liquidity on decentralized exchanges, acknowledge: DeFi tax treatment is one of the least clear areas. The fees you earn are likely ordinary income, but the treatment of entering and exiting liquidity positions is debated. I recommend working with a CPA who specializes in cryptocurrency. I can help you organize your transaction records to make that conversation productive.

Coordinating With CPAs and Tax Professionals

Your role is not to prepare the client’s tax return. Your role is to identify digital asset transactions that have tax implications, help clients organize their records, explain crypto-specific concepts, and flag potential issues before they become IRS notices.

When coordinating with a client’s tax preparer, provide a complete transaction summary with dates, amounts, and fair market values. Document which cost basis method was used and how it was applied. Summarize any staking and mining income with fair market values at receipt. Provide copies of all Form 1099-DAs received plus any transactions not covered by 1099s. If the client made a safe harbor allocation under Revenue Procedure 2024-28, provide documentation of that allocation.

When clients ask you tax questions that cross into return preparation, redirect appropriately: “That’s the right question for your CPA. What I can tell you is how the transaction works and what documentation you’ll need. Let me summarize that so you can discuss it with your preparer.”

This protects you from practicing tax advice without a license while still providing substantial value. You are the bridge between the technical rules and the CPA’s return preparation.

Key Takeaways

- Digital assets are property. Every sale, exchange, and disposition triggers gain or loss recognition. The property classification creates capital gains treatment and eliminates like-kind deferral.

- Crypto-to-crypto swaps are taxable. The most common client misunderstanding is that they have not triggered taxes because they never sold to dollars. Any exchange of one cryptocurrency for another is a taxable event.

- Staking and mining income is ordinary income. Revenue Ruling 2023-14 confirms that staking rewards are taxable when received at fair market value. The same principle applies to mining. Clients owe tax on these tokens whether or not they sell.

- Cost basis method selection matters. FIFO, LIFO, HIFO, and Specific Identification produce different tax outcomes. Choose and document the method before the sale, not after.

- Wallet-by-wallet tracking is mandatory. Each wallet or account is a separate container for basis purposes. Universal pooling is no longer permitted.

- Form 1099-DA brings IRS visibility. Brokers now report transaction data directly to the IRS. Underreporting that went undetected for years will now trigger CP2000 notices.

The Advisor’s Edge

Digital asset taxation looks straightforward on the surface: the IRS treats crypto as property, so swaps are sales. But most advisors who encounter clients with digital assets focus only on whether the client owes taxes on their current year activity.

Your conversation goes deeper. You ask about wallet locations and understand wallet-by-wallet tracking. You identify which transactions create ordinary income (staking, mining, airdrops) versus capital gains. You understand why the timing of dominion and control matters for staking rewards and airdrops. You can explain cost basis methods and why documentation matters before the sale, not after.

You acknowledge the limits. DeFi tax treatment is unclear. Specific identification has timing rules. Wash sales do not apply yet, but may in future legislation. You never claim certainty where guidance is genuinely pending.

You provide a service most advisors miss: you organize your client’s transaction records before tax season arrives, then hand them to the CPA with clear documentation. You explain the tax implications in plain language so the client is not surprised when the return is filed. You coordinate between the client, the broker, and the tax professional rather than leaving your client to figure out the connections.

This coordination is what the Certified Digital Asset Specialist™ (CDAS™) credential represents. Digital asset taxation is not about crypto enthusiasm or technical blockchain knowledge. It is about understanding the tax rules well enough to identify compliance risks, organize records, and bridge the gap between your client’s trading activity and their CPA’s return preparation. You help your clients avoid penalties, reduce their tax liability, and prepare for a more visible IRS environment. That is the advisor’s edge.

For a practical guide to evaluating the ETF vehicles your clients will use for digital asset exposure, see Bitcoin and Crypto ETFs: A Practical Guide for Financial Advisors.

Sources and Notes: CDAS Module 2, Chapter 12 (Digital Asset Taxation: Fundamentals) and Chapter 13 (Digital Asset Tax Reporting and Compliance), Certified Digital Asset Specialist™ course curriculum, IBF. IRS Notice 2014-21 (property classification), Revenue Ruling 2023-14 (staking rewards), Revenue Procedure 2024-28 (safe harbor for wallet-by-wallet allocation), Form 1099-DA reporting requirements. This article is refreshed annually.