The ETF Question: What Actually Matters When Choosing

Your client, Margaret, age 54, asks: “I want some Bitcoin in my portfolio. Which product should I buy?” This seems like a simple question. But the answer determines her custody arrangement, tax treatment, account compatibility, cost structure, and operational complexity. The vehicle decision is as important as the allocation decision.

For years, Bitcoin ETF options were limited. Today they are proliferating: spot Bitcoin ETFs, spot Ethereum ETFs, Ethereum staking ETFs, Solana staking ETFs, and futures-based products that still exist in legacy accounts. Understanding what distinguishes one from another helps you match the right vehicle to each client.

This article focuses on what matters on Monday morning: how to evaluate specific Bitcoin and Ethereum ETF products and decide which is appropriate for a given client. We examine the factors that differentiate products, how to assess custody arrangements, what tracking error means in practice, and how to handle the tax treatment question with clients.

Five Factors That Actually Differentiate Spot Bitcoin ETFs

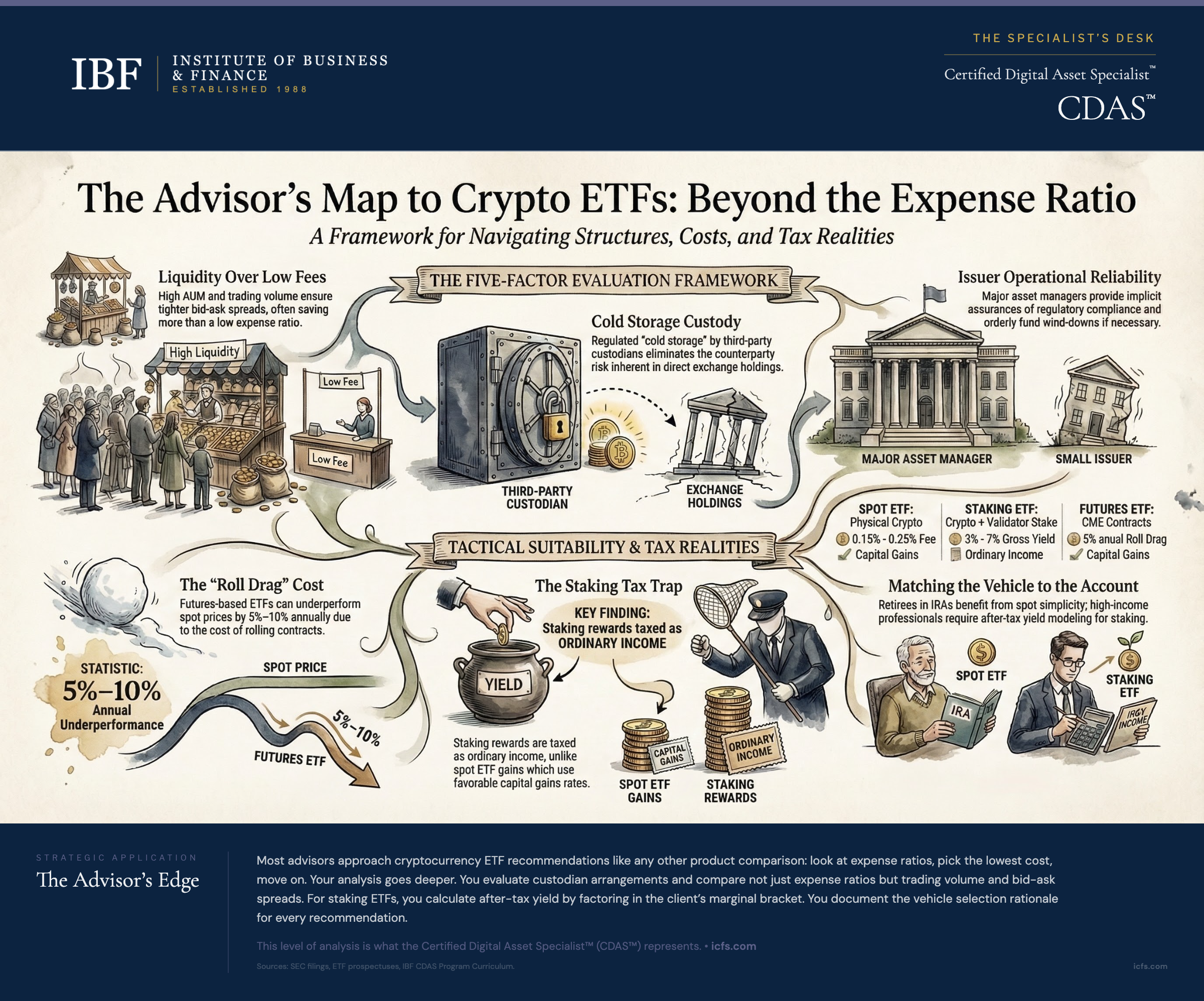

When comparing spot Bitcoin ETFs for a client, most advisors focus on expense ratio alone. This is incomplete. Five factors matter, and each tells you something different about how the product will perform for your specific client.

Expense ratio. This is the annual fee charged as a percentage of assets. Most major spot Bitcoin ETFs charge between 0.15% and 0.25% annually. On a $100,000 position, this translates to $150 to $250 per year. Lower is better, but a slightly higher expense ratio from a more established issuer may be justified by operational reliability. Compare this to futures-based Bitcoin ETFs, which charge 0.85% to 0.95% annually due to the ongoing cost of rolling futures contracts. The expense advantage of spot ETFs is immediate and compounding.

Assets under management. Larger funds typically attract more trading volume, which creates tighter bid-ask spreads. Tighter spreads mean lower transaction costs when clients buy or sell. The largest Bitcoin ETFs, with $100 billion+ in total market assets, trade with a typical spread of 0.02% to 0.05%. A smaller Bitcoin ETF might trade at 0.10% to 0.20% spreads. For a client entering a $50,000 position, the difference between a tight spread and a wide one is measurable. Additionally, AUM indicates market acceptance and issuer commitment to maintaining the product long-term.

Liquidity and trading volume. Average daily trading volume is the best proxy for liquidity. Higher volume signals that other investors are actively trading the product, which means your client can enter and exit efficiently. Check the average daily volume on your platform before recommending. If your client is buying $500,000, you want daily volume in the hundreds of millions to ensure they can move in and out without moving the market.

Custodian arrangement. Most spot Bitcoin ETFs use Coinbase Custody Trust Company, a New York-regulated custodian that holds Bitcoin in cold storage (offline) with insurance coverage. One major Bitcoin ETF issuer operates under a New York state trust charter and received conditional OCC approval in December 2025 for conversion to a national trust bank charter; the conversion is pending completion of pre-opening requirements. For advisory purposes, both models meet regulatory requirements. The practical difference: third-party custody creates an additional counterparty relationship, while self-custody concentrates more functions with the ETF issuer. Ask your clients if they care about this distinction. Most do not; their concern is whether their Bitcoin is safe. Qualified custodians, whether third-party or self-custody through a national bank, provide that assurance.

Issuer track record. The reputation and operational capabilities of the ETF sponsor matter for long-term confidence. Bitcoin ETFs from major asset managers like BlackRock, Fidelity, or Invesco carry implicit assurances about operational continuity and regulatory compliance. If you recommend a Bitcoin ETF from a major issuer and that issuer decides to wind down the fund years later, the orderly process protects your client. Smaller issuers may lack the infrastructure to manage products long-term.

Spot vs. Futures: Why This Distinction Still Matters

Some of your clients may already hold a futures-based Bitcoin ETF like BITO, purchased before spot Bitcoin ETFs existed. Understanding the difference helps you explain whether they should transition.

A spot Bitcoin ETF holds actual Bitcoin. When you buy shares, you own a fractional interest in a trust that holds the cryptocurrency itself. An authorized participant can create new shares by delivering Bitcoin to the trust, or redeem shares by receiving Bitcoin. This structure keeps the ETF price tightly linked to the Bitcoin spot price.

A futures-based Bitcoin ETF holds Bitcoin futures contracts, typically traded on the CME. Because futures contracts expire, the fund must periodically roll its positions: selling expiring contracts and buying longer-dated contracts. This rolling process creates a cost in markets where futures trade at a premium to spot (a condition called contango). When futures prices exceed spot prices, the ETF sells low (expiring contracts) and buys high (new contracts), creating drag on returns.

The quantifiable impact: futures-based ETFs often underperform the spot price by 5% to 10%+ annually during typical contango conditions, and potentially more in volatile environments. A client who bought BITO at $20 may see it decline to $18 due to roll drag, even if Bitcoin price held flat. A client who bought a spot Bitcoin ETF at $20 stays at $20 (minus the small expense ratio).

This is not theoretical. If a client bought $50,000 of BITO five years ago, the roll drag may have cost them $15,000 to $25,000 in foregone returns. The transition to a spot ETF today saves them from future drag, which often justifies any transaction costs or capital gains from switching.

Ethereum ETFs: The Yield Consideration

Spot Ethereum ETFs have attracted less institutional capital than Bitcoin ETFs, despite similar structures. The difference stems from how investors perceive the two assets: Bitcoin as digital gold (pure store of value), Ethereum as a technology platform (with utility and yield potential).

This perception matters because Ethereum’s proof-of-stake consensus mechanism allows holders to earn staking rewards. Initial Ethereum ETFs launched without staking capabilities due to SEC uncertainty about whether staking rewards within an ETF structure might constitute securities issuance. Regulatory clarity has evolved, and newer Ethereum ETFs now stake their holdings and distribute rewards to shareholders.

For clients, this creates a choice: non-staking Ethereum ETFs that hold Ether without generating yield, or staking-enabled Ethereum ETFs that earn approximately 3% to 4% annually in staking rewards. The staking ETFs are newer and smaller, but they address a fundamental advantage of direct Ethereum ownership: the ability to participate in network validation and earn rewards.

If you are considering recommending an Ethereum ETF to a client, ask whether yield matters. If the client wants maximum simplicity and just wants Ethereum price exposure, a non-staking ETF is fine. If the client specifically values the staking yield opportunity and is comfortable with the additional complexity and tax implications (staking rewards are taxable as ordinary income), a staking Ethereum ETF merits consideration.

Compare the net yield. If a staking ETF charges 0.30% in expense ratio and generates 3.5% in staking yield, the net yield is 3.2%. This is meaningful for an income-focused client. Tax the staking income as ordinary income in the client’s marginal bracket, and the after-tax yield becomes smaller. For a client in the 24% federal bracket, 3.2% becomes 2.4% after tax. Still respectable for a volatile asset.

Staking ETFs: When Yield Comes With Complexity

The newest category of digital asset ETFs are staking ETFs. Rather than simply holding a proof-of-stake cryptocurrency, these funds actively participate in network validation and distribute staking rewards to shareholders.

Solana staking ETFs exemplify this category. Solana is a proof-of-stake blockchain that pays validators approximately 7% annually for securing the network. Solana staking ETFs began launching in summer 2025, with the majority of products coming to market in late 2025. The appeal is clear: clients can earn yield from digital assets through a simple ETF without understanding validators, delegation, or unstaking mechanics.

However, staking ETFs come with five considerations that spot-only ETFs do not:

Yield is not guaranteed. Staking rewards depend on network parameters that can change. If Solana’s inflation rate drops (which network governance controls), staking yields will decline. Historical yield does not predict future yield.

Slashing risk exists on some networks. On certain blockchains, validators who misbehave have their staked tokens partially confiscated (slashed). Solana’s slashing mechanism is not automatic; it requires a network halt and restart to trigger. In practice, no Solana staking ETF holder has experienced a slashing event, but the possibility exists. This non-automatic design is why Solana staking ETFs are simpler than Ethereum staking ETFs. But other networks do slash. Know which network’s mechanics you are recommending.

Tax treatment creates complexity. Staking rewards are taxable as ordinary income. For ETF staking products organized as grantor trusts (per IRS Revenue Procedure 2025-31), rewards must be distributed at least quarterly, and investors recognize income on those distributions. If a Solana staking ETF distributes $700 in annual rewards on a $10,000 position, your client owes tax on $700 this year, regardless of whether they sold shares. This differs from spot ETFs where tax events occur only upon sale. For clients in high tax brackets, this annual tax drag matters.

Expense ratios may be higher. Staking ETFs charge higher fees than spot-only products due to operational complexity (validator selection, delegation, reward distribution). A Solana staking ETF might charge 0.25% to 0.35% (with higher-cost outliers at 0.50%) while a non-staking crypto ETF charges 0.20%. Solana staking ETFs generate gross yields of approximately 5.5% to 7% depending on the product. Is the extra yield worth the 0.05% to 0.35% expense premium? Calculate the net yield for each client’s tax situation before recommending.

Liquidity buffers create a constraint. Staked tokens have unbonding periods before they can be liquidated. On Solana, the unbonding period is approximately two days. ETF issuers manage this by maintaining buffers of unstaked Solana and staggering stake activation. This works fine in normal markets, but during unusual volatility, liquidity constraints could cause issues.

Custody: Why It Matters More Than Clients Realize

The FTX collapse demonstrated why custody matters. Customers with assets on that exchange saw their holdings frozen during bankruptcy proceedings. Some recovered partial amounts; many did not. This is counterparty risk that spot ETFs eliminate.

When you buy a spot Bitcoin ETF, your Bitcoin is held by a qualified custodian, not by the ETF issuer and not by you. The custodian is regulated by state banking authorities or the OCC. Assets must be segregated from the custodian’s own funds and held in cold storage (offline) with insurance coverage. If the custodian fails, there are legal protections requiring asset return to owners.

This structure creates a meaningful risk reduction compared to holding Bitcoin on an exchange. An exchange failure leaves you in bankruptcy court waiting for recovery. A custodian failure involves insurance and regulatory protections that move much faster.

For clients who want cryptocurrency exposure but worry about custody risk, this is the case for spot ETFs: buy simplicity and qualified custody through a trusted vehicle rather than take on the operational burden of direct ownership or exchange counterparty risk.

A Practical Framework: Matching Vehicles to Client Situations

When a client asks “which Bitcoin ETF should I buy?”, here is how to think about the decision systematically.

For a retiree in an IRA: A spot Bitcoin ETF from a major issuer (large AUM, tight spreads, established issuer) is the clear choice. The client buys it like any other stock, holds it through their IRA, and never manages custody. Tax complications are deferred until retirement distributions. Complexity is minimal.

For a high-income professional in a taxable account: Still a spot Bitcoin ETF, but evaluate whether a staking Ethereum ETF might also merit consideration. The professional likely has longer time horizons and can afford to pay taxes on staking yield. Model the after-tax yield to determine if it justifies the additional complexity. For Bitcoin specifically, stick with spot. No staking available.

For a client who wants multiple cryptocurrencies: Spot Bitcoin and Ethereum ETFs are available, but if the client wants exposure to Solana, Cardano, or other assets, options are limited. At that point, a direct crypto exchange account (Coinbase, Kraken) might be justified if the client has operational sophistication to manage custody and tax complexity.

For a conservative client who owns a legacy futures Bitcoin ETF: Evaluate whether the roll drag cost justifies transitioning to a spot ETF. If the client bought at high cost basis, the capital gains from switching might consume the future savings. Calculate the break-even point: how long until the elimination of roll drag offsets the transition taxes? For most clients with multi-year horizons, the answer is yes, transition makes sense.

The Tax Consideration Most Advisors Forget

Spot Bitcoin and Ethereum ETFs are treated as capital assets, not securities. This means gains are taxable at capital gains rates (long-term if held over one year, short-term otherwise). For long-term investors, this is favorable: capital gains rates are lower than ordinary income rates.

Staking ETFs introduce ordinary income. Staking rewards are taxed as ordinary income, not capital gains. A client in the 24% federal bracket pays 24% on staking rewards immediately, plus state tax. This is worth disclosing explicitly.

For clients holding spot ETFs in tax-loss harvesting strategies, there is good news: no wash sale rule applies to cryptocurrency as of early 2026, though this may change via legislation. A client can sell a position at a loss, harvest the loss for tax purposes, and immediately repurchase the same ETF without wash-sale complications. This is not true for stocks, which creates a planning opportunity.

Client Conversation: How to Handle the Vehicle Question

When Margaret asks, “Which Bitcoin ETF should I buy?”, here is how the conversation might flow:

“Margaret, you’re asking the right question. There are several spot Bitcoin ETFs available, and they’re similar in structure but differ in a few ways that matter. Let me walk you through the comparison.

All of the major Bitcoin ETFs hold actual Bitcoin in qualified custody, so your asset is protected. The main differences are expense ratio, which is the annual fee, and trading volume, which affects how efficiently we can buy and sell.

The top three Bitcoin ETFs have expense ratios between 0.18% and 0.25%, and all three trade with very tight spreads, meaning low transaction costs. My recommendation is the one with the highest assets under management and tightest spreads, which we’ll be able to buy at the best price.

Once we own it, you will see it trade on your brokerage statement just like a stock. You’ll receive a Form 1099-B reporting capital gains or losses, and beginning with 2025 transactions, also Form 1099-DA from digital asset brokers. If you hold for over a year, gains are taxed at long-term capital gains rates, which is favorable.

The main thing to understand is that this ETF holds real Bitcoin. You’re not buying a derivative or a promise to track Bitcoin. You own fractional shares of a trust that holds the actual asset. That’s why it’s so much simpler than direct ownership.”

This frames the vehicle as a straightforward investment vehicle while explaining the custody advantage over direct ownership.

Key Takeaways

- Spot Bitcoin and Ethereum ETFs are the default vehicle for most clients due to qualified custody, low costs, and operational simplicity.

- Five factors differentiate spot cryptocurrency ETFs: expense ratio, assets under management, liquidity, custodian arrangement, and issuer track record. All five matter, not just the fee.

- Spot Ethereum ETFs now include staking-enabled versions that distribute validator rewards to shareholders, offering yield potential with tax complexity.

- Staking ETFs generate ordinary income (not capital gains), have higher expense ratios, and require understanding of staking mechanics and yield variability.

- Qualified custodian arrangements in spot ETFs eliminate the counterparty risk inherent in direct exchange holdings, providing meaningful risk reduction compared to the FTX-style collapse scenarios.

- Tax treatment is favorable: capital gains rates for spot ETFs, ordinary income rates for staking rewards, and no wash-sale rules for cryptocurrency as of early 2026.

The Advisor’s Edge

Most advisors approach cryptocurrency ETF recommendations like any other product comparison: look at expense ratios, pick the lowest cost, move on. This misses the real conversation.

Your analysis goes deeper. You evaluate the specific custodian arrangement and explain why that matters. You compare not just expense ratios but also trading volume and bid-ask spreads to assess the real transaction cost your client will pay. You understand the tax treatment: capital gains for spot products, ordinary income for staking rewards.

For staking ETFs, you calculate the after-tax yield by factoring in your client’s marginal tax bracket and assessing whether the net yield justifies the 0.30% expense premium over spot products. You explain the staking mechanics clearly enough that the client understands why Solana staking is simpler than Ethereum staking (no slashing risk on Solana) or why a client’s direct staking yield will differ from an ETF’s yield due to validator fees.

You document the vehicle selection rationale. If you recommend a Bitcoin ETF over direct ownership for a moderately sophisticated client, your file clearly states: client requested direct ownership, but advised ETF structure due to custody simplification, tax reporting benefits, and operational complexity concerns. Or if you recommend against a staking ETF despite the client’s interest in yield, you document: net after-tax yield of 2.1% (given client’s 24% federal + 5% state tax bracket) does not justify 0.40% expense premium over spot alternative; client prefers simplicity.

This level of analysis is what the Certified Digital Asset Specialist™ (CDAS™) credential represents. Digital asset recommendations are not about picking an asset class. They are about understanding how to implement that asset class for your specific client’s situation, matching the right vehicle to the right profile, and optimizing for their total after-tax, after-cost outcome.

As digital asset ETF options expand and staking becomes more common, your ability to compare vehicles systematically and explain the distinctions in plain language positions you as a guide, not a product selector.

For guidance on how much digital asset exposure is appropriate for specific client profiles, see How Much Crypto Should Your Client Own? A Portfolio Allocation Framework.

Sources and Notes: CDAS Module 1, Chapter 6 (Digital Asset Investment Vehicles) and CDAS Module 2, Chapter 14 (Suitability and Portfolio Integration), Certified Digital Asset Specialist™ course curriculum, IBF. ETF expense ratios, AUM, and trading data from issuer prospectuses and fund fact sheets. IRS Revenue Procedure 2025-31 (grantor trust staking ETF tax treatment). OCC conditional charter approval (December 2025). Staking yield estimates based on network parameters at time of publication. This article is refreshed annually.