The Question Changed in 2025

For three years, an advisor asked about bitcoin in a 401(k) had regulatory cover to say no. In March 2022, the Department of Labor told plan fiduciaries to exercise “extreme care” before adding cryptocurrency to a 401(k) menu, language unusual enough that most recordkeepers and plan sponsors treated it as a closed door.

That cover is gone. On May 28, 2025, the DOL rescinded the 2022 guidance and returned to an explicitly neutral posture, neither endorsing nor disapproving crypto on plan menus. Then on August 7, 2025, Executive Order 14330 (Democratizing Access to Alternative Assets for 401(k) Investors) directed the DOL and SEC to propose rule changes within 180 days opening plan menus to alternative assets, with crypto exposure arriving through professionally managed investment vehicles rather than direct coin purchases. Major recordkeepers had already been building: Fidelity has offered a Digital Assets Account inside some 401(k) plans since 2022, and more plan menus are following. The practical effect for advisors is that “can my retirement account hold crypto” is no longer hypothetical, and the client asking has usually already read something optimistic about it. The advisor’s job is knowing the three routes in, what each one costs, and where each one breaks.

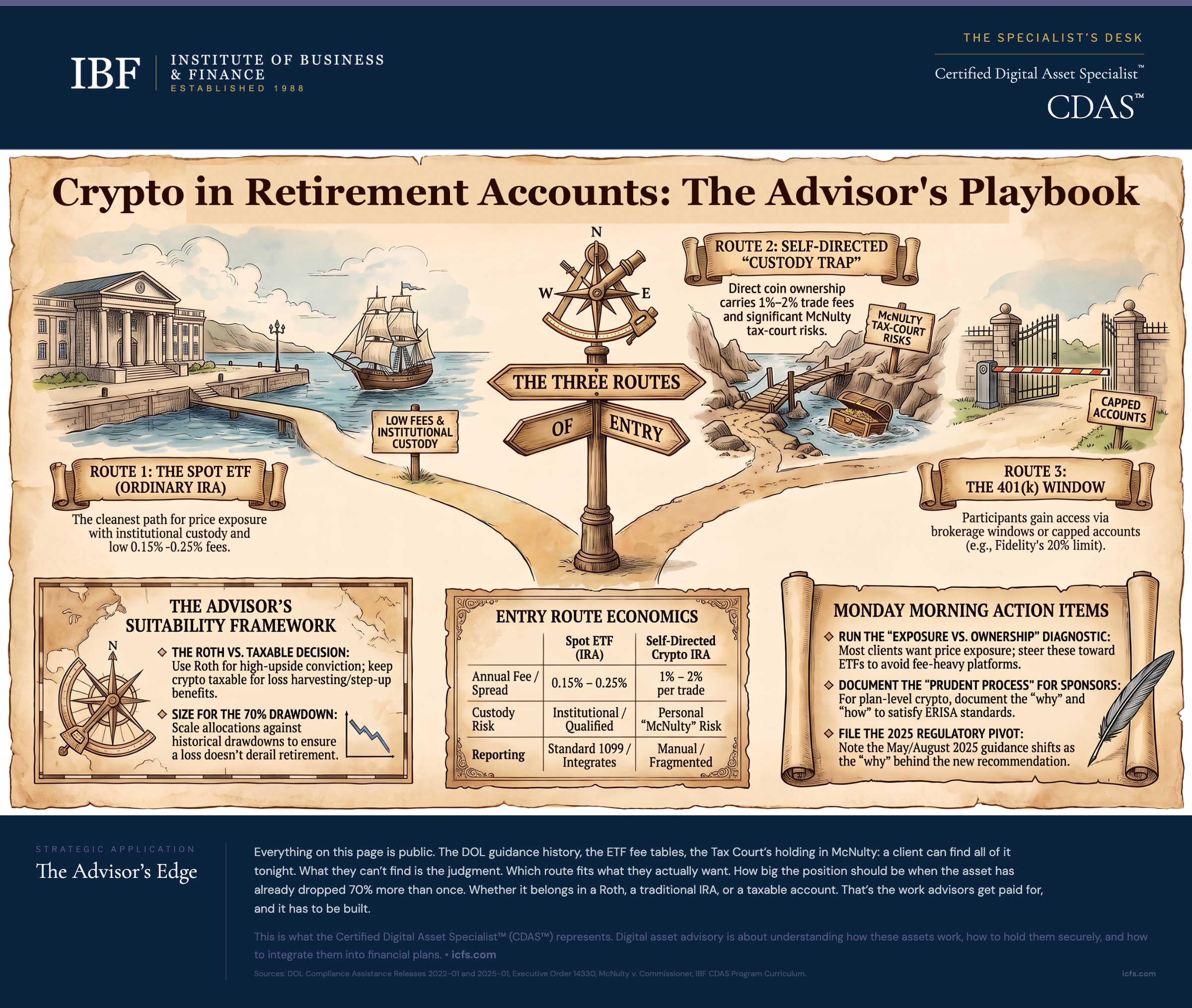

Route One: A Spot ETF Inside an Ordinary IRA

The simplest route needs no special account at all. Since spot bitcoin ETFs launched in January 2024, followed by spot ether ETFs later that year, crypto exposure has been available as an ordinary ticker in an ordinary brokerage IRA. The client’s existing custodian holds an ETF; the ETF’s custodian holds the coins.

This route wins on almost every dimension an advisor cares about. Expense ratios on spot bitcoin ETFs run from roughly 0.15% to 0.25% per year, with the two largest funds both at 0.25%, against the 1% to 2% per-trade fees common on dedicated crypto IRA platforms. Custody risk sits with a qualified institutional custodian rather than with the client. The position shows up in performance reporting and rebalancing software like anything else. And there is no plausible prohibited-transaction exposure, because the client never touches a private key.

What the ETF route gives up: direct ownership of the asset, access to anything beyond the major coins with an approved ETF, and the ability to move coins out or use them. For a retirement allocation, none of those usually matter. A client who wants to actually use crypto is describing a taxable-account activity, not a retirement position.

Route Two: The Self-Directed Crypto IRA

Dedicated platforms offer self-directed IRAs that hold coins directly. The pitch is real ownership and a wider asset menu. The costs deserve a harder look than most marketing invites.

Fee structures vary, but the common pattern is a spread or transaction fee of 1% to 2% per trade, with the leading platforms clustered at 1%, and some charge monthly account or custody fees on top. A client who dollar-cost-averages into a position pays that toll on every buy. Over years, the drag can dwarf the ETF expense ratio the client thought they were too sophisticated for.

The sharper risk is custody discipline, and there is case law on it. In McNulty v. Commissioner (2021), the Tax Court looked at a self-directed IRA structured with a checkbook-control LLC whose owner took personal possession of American Eagle coins the IRA had purchased. The court held that taking personal custody of IRA assets was a distribution, taxable in full. The logic maps directly onto crypto: an IRA owner who moves the account’s coins to a wallet they personally control has arguably taken possession, and the entire account can be deemed distributed, with income tax and, under 59½, the 10% additional tax due on all of it. No court has yet applied McNulty to a crypto wallet specifically (the case involved physical coins), but the extension is the consensus reading among tax and ERISA practitioners. A client holding a six-figure crypto IRA on a hardware wallet in their desk drawer is not running a clever structure. They are holding an audit outcome that has already been litigated once.

The self-directed route can still make sense for a narrow client: someone who wants assets no ETF covers, understands the fee load, and will leave custody with the platform’s qualified custodian without exception. That is a smaller population than the platforms’ ad spend suggests.

Route Three: Crypto on the 401(k) Menu

Inside employer plans, crypto arrives either as a designated investment window (Fidelity’s Digital Assets Account model, which caps the crypto allocation at 20% of the participant’s balance, with employers able to set a lower limit) or through a self-directed brokerage window where the participant buys a spot ETF.

For the participant, the analysis mirrors the IRA discussion. For the advisor working with plan sponsors, there is an extra layer: the 2025 guidance shift changed the regulator’s tone, not the fiduciary standard. ERISA’s prudence duty applies to menu selection exactly as it did in 2022. A sponsor who adds a crypto option still needs a documented prudent process: why this asset class, why this vehicle, what cap, what participant education. “The DOL backed off” is a fact about enforcement posture, not a defense in participant litigation. Advisors who serve plans should treat the new openness as permission to run the analysis, not permission to skip it.

The Account Decision: Roth, Traditional, or Taxable

Once a client decides they want crypto exposure at all, account location is a real decision, and the standard asset-location logic applies with extra force because the expected-return assumptions are so wide.

The Roth case. If the client’s thesis is right and the asset appreciates dramatically, a Roth converts that entire outcome to tax-free. High-volatility, high-ceiling assets are exactly what Roth capacity is theoretically best spent on. The counterargument deserves equal airtime: if the asset craters, the client has burned scarce Roth space on a loss they can never harvest.

The traditional-IRA case. Deferral still helps, but every dollar of crypto gain eventually comes out as ordinary income. A client whose taxable-account crypto would have received long-term capital gains treatment has, inside a traditional IRA, traded a preferential rate for deferral. For a buy-and-hold position, that trade can be a loser.

What every retirement account gives up. Inside any IRA or 401(k), there is no tax-loss harvesting, and crypto’s volatility makes it one of the most harvestable assets in a taxable account. There is also no step-up in basis at death; a taxable-account crypto position held until death passes to heirs with the gain erased, while the same position inside a traditional IRA passes as fully taxable income to the beneficiary. For clients with estate-planning weight on the decision, taxable ownership of the crypto sleeve is sometimes the better answer.

Limitation: Where the Whole Idea Breaks Down

The retirement-account framing fails a specific kind of client: the one whose crypto conviction is really a liquidity preference in disguise. Retirement accounts are the wrong home for assets a client may want to sell fast on sentiment, move to a wallet, or spend. Early-withdrawal friction that protects a retirement saver becomes a trap for a trader.

Sizing is the other failure point. An asset that has drawn down more than 70% from peak multiple times in its history behaves differently inside a portfolio someone must draw income from. A 2% position that doubles helps a retirement plan; a 15% position that draws down 70% two years before retirement changes the client’s life. The access question got easier in 2025. The sizing math did not move at all.

And the regulatory ground remains unsettled in both directions. Guidance that loosened by executive action can tighten the same way. An advisor building a client’s plan around today’s posture should note the assumption in the file.

The Client Conversation

The call usually opens with a version of “my buddy has bitcoin in his IRA, can we do that?” The productive answer sequences three questions.

First, exposure or ownership? If the client wants price exposure in a retirement account, the spot ETF route delivers it at institutional custody standards and index-fund-level fees, inside the account they already have. Most conversations end here, happily.

Second, if they want direct ownership, why? Listen for the answer. “I don’t trust ETFs” leads to a custody conversation and usually back to the ETF. “I want assets the ETFs don’t cover” is legitimate and leads to the self-directed platforms, with the fee schedule and the McNulty custody rules on the table before anything is signed.

Third, how big and in which account? Anchor the size to what the plan can absorb in a 70% drawdown, then place it: Roth for maximum-upside conviction the client can afford to lose, taxable when harvesting and step-up matter, traditional IRA rarely for this asset. Write down the reasoning. If crypto ends up in the plan, the file should show it got there through the same process as everything else.

Key Takeaways

- When a client asks about crypto in a retirement account, present the spot-ETF-in-an-IRA route first. It solves for exposure, custody, and cost simultaneously.

- Before any client opens a self-directed crypto IRA, put the full fee schedule (trade spreads, monthly fees, custody charges) next to a spot ETF’s expense ratio in one table.

- Tell every self-directed IRA client the McNulty rule in one sentence: move the IRA’s coins to a wallet you control and the IRS can treat the whole account as distributed.

- Size crypto positions against a 70%+ drawdown scenario at the client’s retirement date, not against the asset’s best decade.

- Prefer Roth capacity for small, high-conviction crypto sleeves; keep crypto out of traditional IRAs when long-term capital gains treatment or step-up at death would be worth more than deferral.

- For plan-sponsor clients considering a crypto menu option, document a prudent selection process. The 2025 guidance change shifted tone, not the ERISA standard.

The Advisor’s Edge

Nothing in this article is secret. The DOL’s guidance history, the ETF expense ratios, the Tax Court’s reasoning in McNulty, and every crypto IRA platform’s fee page are public and a search away, for advisors and for their clients.

What separates the advisor from the search result is the ability to run the full decision: matching the access route to what the client actually wants, placing the position in the right account for their tax picture, sizing it against a drawdown the asset has already demonstrated, and documenting the process so the recommendation holds up years later. That is a body of connected judgment, and it is what clients are paying for when they ask the bitcoin question.

The Certified Digital Asset Specialist™ (CDAS™) designation is where financial professionals build that judgment, covering digital asset markets, custody, taxation, and portfolio integration at the depth client work requires.

For the vehicle-level analysis behind route one, see Crypto ETFs: An Advisor’s Guide.

Sources and Notes: Analysis based on Department of Labor Compliance Assistance Release 2022-01 and its 2025 rescission, Executive Order 14330, Democratizing Access to Alternative Assets for 401(k) Investors (August 7, 2025), McNulty v. Commissioner, 157 T.C. No. 10 (2021), and published spot ETF and crypto IRA platform fee schedules. Regulatory posture described as of Q2 2026.